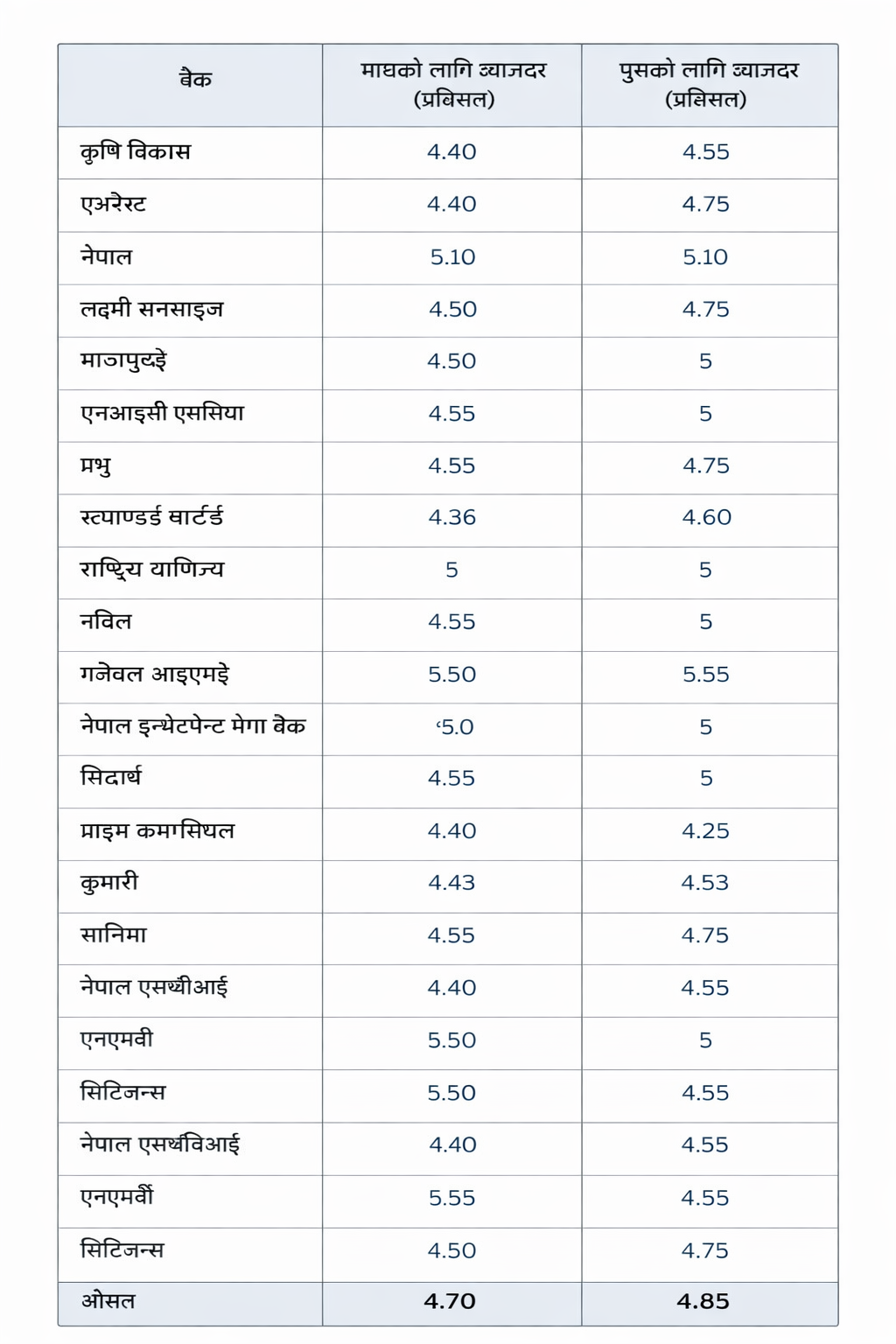

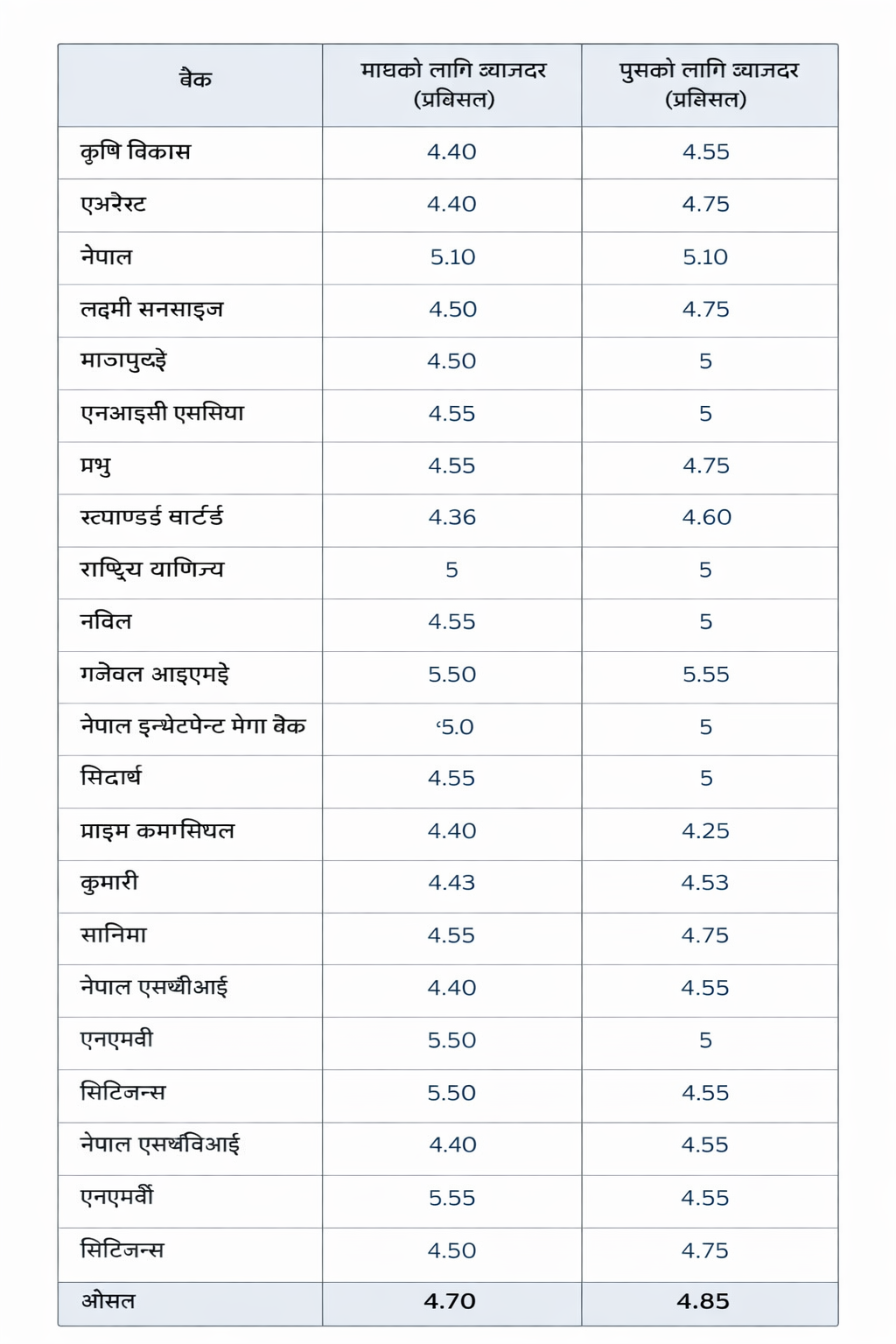

काठमाडौं । माघ महिनाका लागि वाणिज्य बैंकहरूले सार्वजनिक गरेको नयाँ ब्याजदर तालिकाले बैंकिङ प्रणालीमा तरलता अत्यधिक रहेको स्पष्ट संकेत गरेको छ। सञ्चालनमा रहेका २० वाणिज्य बैंकमध्ये १२ बैंकले पुसको तुलनामा माघमा निक्षेपको ब्याजदर घटाएका छन् भने ७ बैंकले व्यक्तिगत मुद्दती निक्षेपमा दिने अधिकतम ब्याजदर यथावत् राखेका छन्। यसबीच प्राइम कमर्सियल बैंकले भने अपवादका रूपमा ब्याजदर बढाएको छ।

पुस महिनामा व्यक्तिगत मुद्दती निक्षेपको अधिकतम ब्याजदर ५.५५ प्रतिशतसम्म पुगेको थियो। तर माघमा यस्तो अधिकतम दर घटेर ५.५ प्रतिशतमा सीमित भएको छ। त्यस्तै, पुसमा औसत ब्याजदर ४.८५ प्रतिशत रहेकोमा माघमा घटेर ४.७ प्रतिशतमा झरेको छ। यसले बैंकिङ प्रणालीमा कर्जा माग कमजोर रहेको र निक्षेप परिचालनमा बैंकहरूलाई चुनौती बढ्दै गएको देखाउँछ।

कुन बैंकले कति ब्याज?

माघ महिनामा व्यक्तिगत मुद्दती निक्षेपमा सबैभन्दा धेरै ब्याज दिने बैंकको रूपमा ग्लोबल आइएमई बैंक अग्रस्थानमा देखिएको छ। उक्त बैंकले ५.५ प्रतिशत ब्याजदर सार्वजनिक गरेको छ। त्यसपछि नेपाल बैंक, राष्ट्रिय वाणिज्य बैंक, एनआइसी एसिया, एनएमबी बैंक तथा नेपाल इन्भेष्टमेन्ट मेगा बैंकले अधिकतम ५ प्रतिशत ब्याजदर दिएका छन्।

सबैभन्दा कम ब्याजदर भने स्ट्याण्डर्ड चार्टर्ड बैंकले दिएको छ, जसको अधिकतम ब्याजदर ४.३६ प्रतिशत मात्रै रहेको छ। कृषि विकास बैंक, एभरेष्ट बैंक, लक्ष्मी सनराइज बैंक, माछापुच्छ्रे बैंक, कुमारी बैंक, सानिमा बैंक, सिटिजन्स बैंक लगायतले पनि पुसको तुलनामा ब्याजदर घटाएका छन्।

प्राइम कमर्सियल बैंकले भने व्यक्तिगत मुद्दती निक्षेपको ब्याजदर ४.२५ प्रतिशतबाट बढाएर ४.४ प्रतिशत पुर्याएको छ, जुन माघ महिनाको एक मात्र वृद्धि हो।

रेमिटेन्स खातामा भने आकर्षण

बैंकहरूले रेमिटेन्स खातामा भने व्यक्तिगत मुद्दती खाताभन्दा करिब एक प्रतिशत बढी ब्याज दिइरहेका छन्। वैदेशिक रोजगारीबाट भित्रिने रेमिटेन्सलाई बैंकिङ प्रणालीमा आकर्षित गर्न यस्तो नीति लिइएको बैंकहरूको भनाइ छ।

किन घट्दैछ ब्याजदर?

पछिल्लो समय बैंकहरूसँग कर्जा लगानी योग्य रकम अत्यधिक बढेपछि ब्याजदर निरन्तर घटिरहेको हो। हाल बैंकिङ प्रणालीमा करिब ११ खर्ब रुपैयाँभन्दा बढी कर्जा दिन मिल्ने रकम (तरलता) रहेको छ। कर्जा माग कमजोर हुँदा बैंकहरू आफ्नो अतिरिक्त रकम राष्ट्र बैंकमा राख्न बाध्य भएका छन्।

कर्जा विस्तार नहुँदा बैंकहरूले पछिल्लो समय २.६७ प्रतिशतदेखि ३ प्रतिशतसम्मको ब्याजदरमा राष्ट्र बैंकमा रकम राखिरहेका छन्। राष्ट्र बैंकले पनि एक वर्षे ऋणपत्र जारी गर्दै बैंकहरूबाट अतिरिक्त तरलता सोसिरहेको छ। यसरी राष्ट्र बैंकमा थुप्रिएको रकम हाल आठ खर्ब ७३ अर्ब रुपैयाँ पुगेको छ।

बैंकिङ प्रणालीको अवस्था

हाल बैंक तथा वित्तीय संस्थाहरूसँग कुल ७६ खर्ब ५९ अर्ब रुपैयाँ निक्षेप संकलन भएको छ भने त्यसको तुलनामा कर्जा लगानी ५७ खर्ब २८ अर्ब रुपैयाँ मात्र रहेको छ। निक्षेप र कर्जाबीचको यो ठूलो अन्तरले बैंकिङ प्रणालीमा तरलता प्रशस्त रहेको तर आर्थिक गतिविधि सुस्त रहेको संकेत गर्दछ।

माघ महिनाको ब्याजदरले निक्षेपकर्ताका लागि प्रतिफल घट्दै गएको देखाए पनि बैंकिङ प्रणालीको स्थायित्वका हिसाबले तरलता व्यवस्थापनको अवस्था सहज बनेको छ। कर्जा माग बढ्न नसकेसम्म ब्याजदर तत्कालै माथि जाने सम्भावना न्यून देखिन्छ। आर्थिक गतिविधि विस्तार, निजी क्षेत्रको लगानी वृद्धि र कर्जा प्रवाहमा सुधार आएपछि मात्र ब्याजदरमा पुनः उकालो लाग्ने अपेक्षा गर्न सकिने अवस्था देखिन्छ।