एभरेष्ट बैंकको खुद नाफा २१.११% ले वृद्धि, पुस २०८१ को दोस्रो त्रैमासमा शानदार प्रदर्शनEverest Bank Achieves 21.11% Profit Growth in Second Quarter of FY 2081: A Detailed Analysis

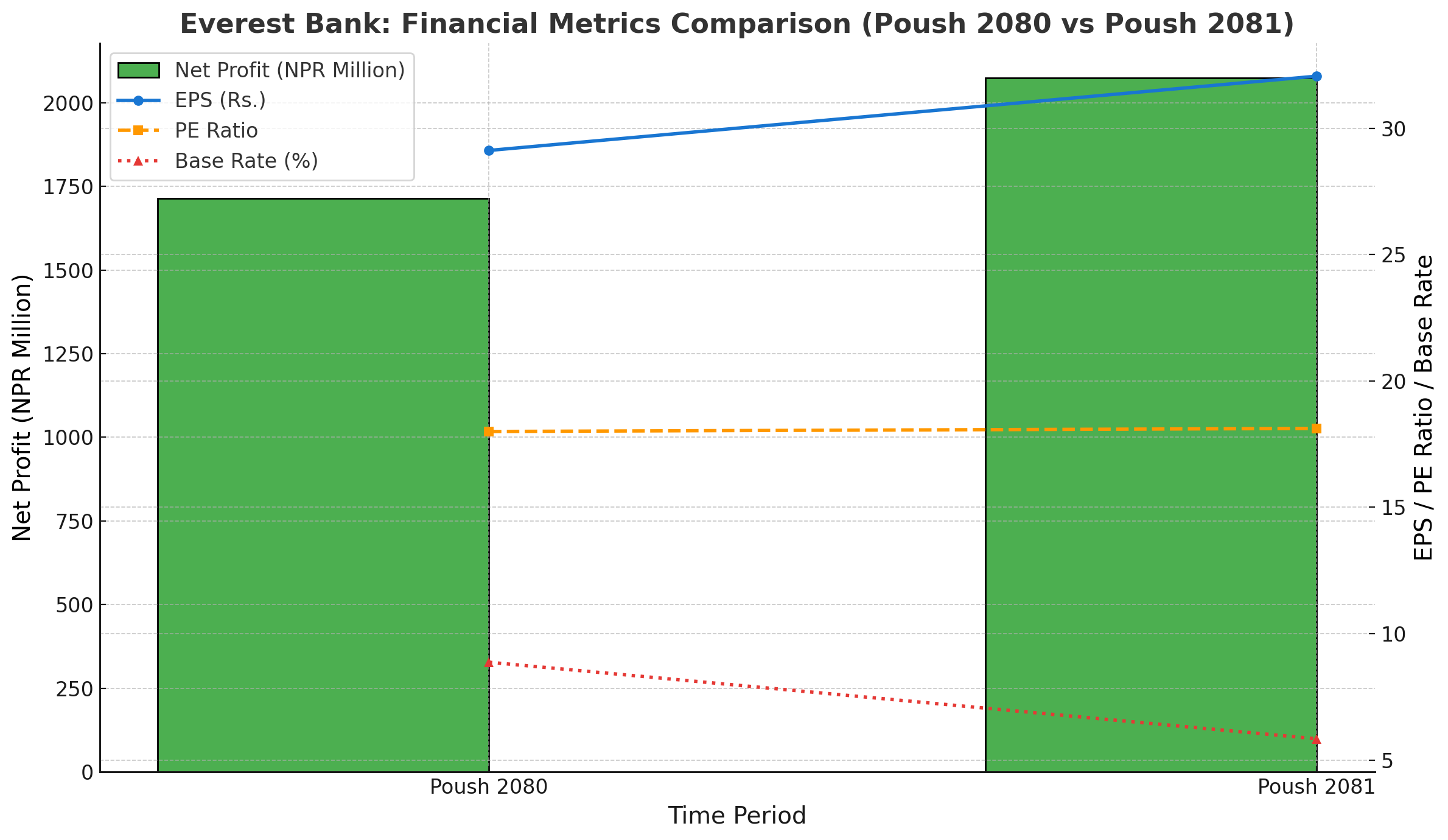

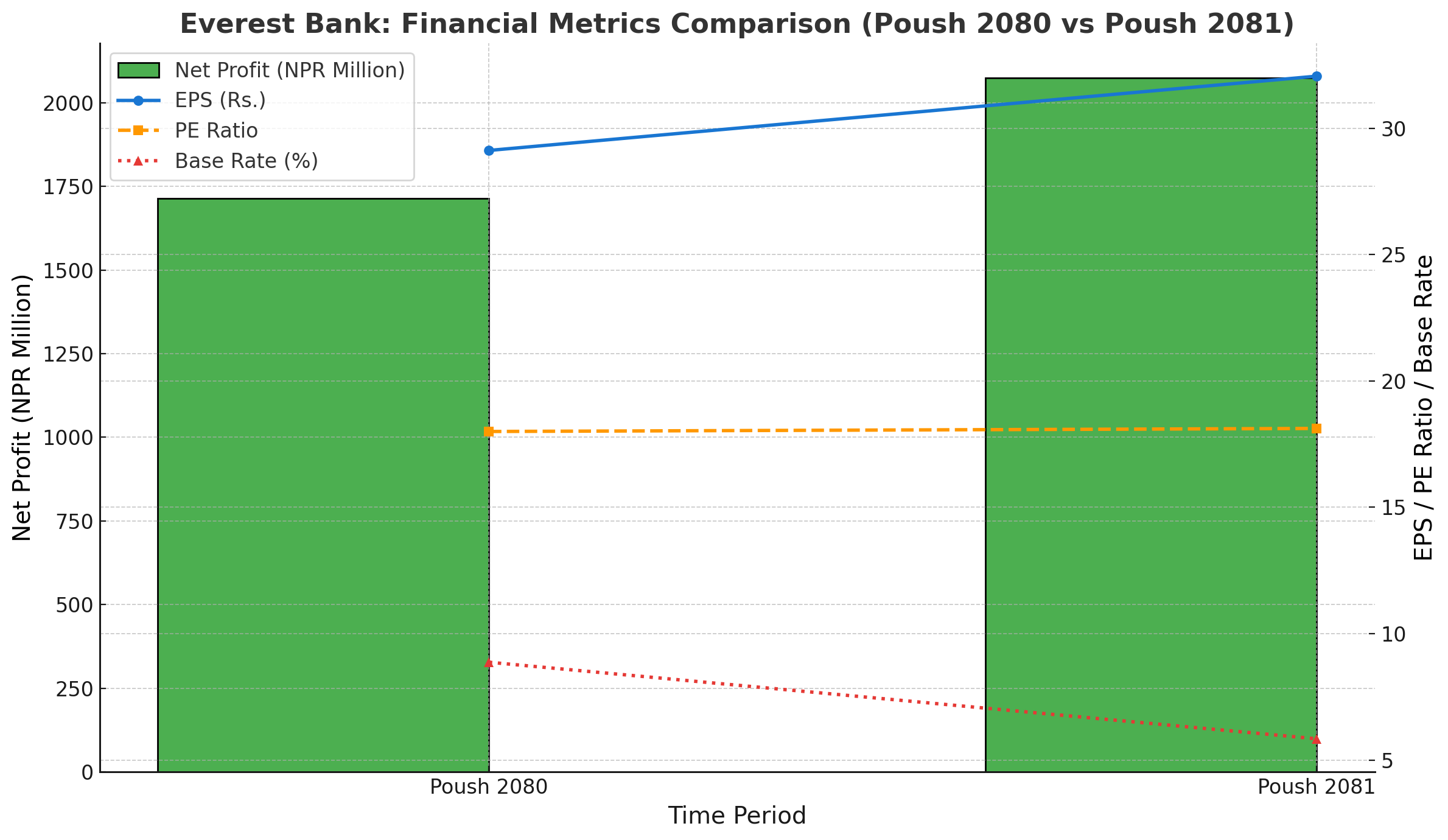

एभरेष्ट बैंक लिमिटेड (EBL) ले आर्थिक वर्ष २०८१ को दोस्रो त्रैमाससम्मको अपरिष्कृत वित्तीय विवरण सार्वजनिक गरेको छ। विवरण अनुसार, बैंकले २ अर्ब ७ करोड ४७ लाख रुपैयाँ खुद नाफा आर्जन गरेको छ, जुन अघिल्लो वर्षको सोही अवधिको तुलनामा २१.११% ले वृद्धि हो। गत वर्षको सोही अवधिमा बैंकको खुद नाफा १ अर्ब ७१ करोड ३१ लाख रुपैयाँ थियो। यो वृद्धि बैंकले ब्याज आम्दानी बढाउनु र खर्च व्यवस्थापन सुधार्नुका साथै इम्पेरमेन्ट चार्ज घटाउन सफल भएकाले सम्भव भएको हो।

खुद नाफामा उल्लेख्य वृद्धि

बैंकले चालु त्रैमासमा ३६ करोड १६ लाख रुपैयाँले खुद नाफा बढाएको छ। यो वृद्धि बैंकको सञ्चालन कुशलता र ग्राहकहरूको बढ्दो विश्वासलाई पुष्टि गर्छ।

खुद ब्याज आम्दानी (Net Interest Income)

बैंकको खुद ब्याज आम्दानी १९.११% ले वृद्धि भई ३ अर्ब ६२ करोड रुपैयाँबाट ४ अर्ब ३१ करोड रुपैयाँ पुगेको छ। यो बैंकको प्रभावकारी ऋण व्यवस्थापन र व्याज दर फैलावटको कुशल उपयोगको संकेत हो।

शुल्क र कमिशन आम्दानी (Fee and Commission Income)

खुद शुल्क र कमिशन आम्दानी १४.४६% ले वृद्धि भई ६६ करोड ८४ लाख रुपैयाँबाट ७६ करोड ५० लाख रुपैयाँ पुगेको छ। यसले सेवा शुल्क, कार्ड जारी गर्ने शुल्क र अन्य बैंकिङ सेवा मार्फत आम्दानी बढेको देखाउँछ।

सञ्चालन आम्दानी (Operating Income)

कुल सञ्चालन आम्दानी १७.६९% ले वृद्धि भई ४ अर्ब ५० करोड रुपैयाँबाट ५ अर्ब २९ करोड रुपैयाँ पुगेको छ, जसले बैंकको आर्थिक बलियो आधारलाई पुष्टि गर्छ।

इम्पेरमेन्ट चार्जमा कमी

इम्पेरमेन्ट चार्ज ४३ करोड २३ लाख रुपैयाँबाट घटेर ३४ करोड ९५ लाख रुपैयाँमा झरेको छ। यसले बैंकको सम्पत्ति गुणस्तरमा सुधार र जोखिम व्यवस्थापन प्रभावकारी भएको संकेत गर्दछ।

सञ्चालन मुनाफा (Operating Profit)

बैंकको सञ्चालन मुनाफा २६.९७% ले वृद्धि भई ३ अर्ब १० करोड रुपैयाँ पुगेको छ, जुन अघिल्लो वर्षको २ अर्ब ४४ करोड रुपैयाँ थियो।

प्रति शेयर आम्दानी (EPS)

बैंकको EPS २.९४ रुपैयाँले बढेर ३२.०६ रुपैयाँ पुगेको छ, जसले लगानीकर्ताहरूका लागि राम्रो प्रतिफलको संकेत गर्दछ।

प्रति शेयर नेटवर्थ (Net Worth Per Share)

२२५.७९ रुपैयाँ पुगेको छ, जसले बैंकको सुदृढ वित्तीय अवस्थालाई झल्काउँछ।

PE अनुपात (PE Ratio)

१८.१२ गुणा रहेको छ, जुन स्थिर छ।

आधार दर (Base Rate)

आधार दर ८.८७% बाट घटेर ५.८४% मा झरेको छ। यो घटावटले बैंकको ऋण प्रतिस्पर्धा बढाउनेछ।

निक्षेप र कर्जा (Deposits and Loans)

निक्षेप

ग्राहक निक्षेप ७.८०% ले वृद्धि भई २ खर्ब ५० अर्ब रुपैयाँ पुगेको छ।

कर्जा लगानी

कर्जा लगानी १६.९६% ले वृद्धि भई २ खर्ब ८ अर्ब रुपैयाँ पुगेको छ।

कर्जा-निक्षेप अनुपात (LDR)

८५.३९% पुगेको छ, जसले बैंकले निक्षेपलाई प्रभावकारी रूपमा लगानी गर्न सफल भएको देखाउँछ।

आधार दरमा गिरावट

आधार दर घट्नुले ऋणग्राहीहरूका लागि आकर्षक भए पनि बैंकको व्याज आम्दानीमा असर पर्न सक्ने जोखिम छ।

सम्पत्ति गुणस्तरको व्यवस्थापन

सम्पत्ति गुणस्तर कायम राख्न बैंकलाई जोखिम व्यवस्थापनमा सतर्क रहन आवश्यक छ।

एभरेष्ट बैंकले चालु आर्थिक वर्षको दोस्रो त्रैमासमा वित्तीय सूचकहरूमा उल्लेखनीय वृद्धि हासिल गरेको छ। शुल्क र व्याज आम्दानीको वृद्धि, इम्पेरमेन्ट चार्जको कमी, र निक्षेप तथा कर्जाको राम्रो व्यवस्थापनले बैंकलाई प्रतिस्पर्धात्मक बनाएको छ।

लगानीकर्ताहरूका लागि उच्च प्रतिफल, ग्राहकहरूका लागि आकर्षक दर, र समग्र रूपमा बलियो वित्तीय स्थिति बैंकको आगामी सफलताका लागि सकारात्मक संकेत हुन्। बैंकले चालु रणनीतिलाई निरन्तरता दिएमा आगामी त्रैमासहरूमा पनि थप उत्कृष्टता हासिल गर्न सक्छ।

Everest Bank Limited (EBL), one of Nepal’s prominent financial institutions, has published its unaudited financial results for the second quarter of FY 2081, showing a robust performance across key metrics. The bank’s net profit surged by 21.11% to NPR 2.07 billion, compared to NPR 1.71 billion in the same period last year (Poush 2080). This strong performance highlights Everest Bank’s effective management strategies and its ability to adapt to changing market conditions.

Net Profit Growth

The bank’s net profit rose by NPR 361.6 million in a year, driven by growth in core revenue streams and reduced costs. This marks a significant achievement for the bank, reflecting strong operational efficiency and growing customer trust.

Net Interest Income (NII):

NII, the primary revenue source for the bank, increased by 19.11%, from NPR 3.62 billion in Poush 2080 to NPR 4.31 billion in Poush 2081. This indicates better management of lending and borrowing rates and an expanded loan portfolio.

Fee and Commission Income:

The bank’s fee-based revenue also grew, with net fee and commission income rising by 14.46% to NPR 765 million, up from NPR 668 million in the previous year. This demonstrates Everest Bank’s growing ability to diversify its income sources through services like remittance, card issuance, and trade finance.

Operating Income:

The total operating income surged by 17.69% to NPR 5.29 billion, up from NPR 4.50 billion in Poush 2080, further solidifying the bank’s financial strength.

Reduction in Impairment Charges:

One of the significant contributors to the profit growth was the reduction in impairment charges, which dropped by NPR 82.7 million, from NPR 432.3 million in Poush 2080 to NPR 349.6 million in Poush 2081. This reflects improved asset quality and better risk management practices.

Operating Profit:

The operating profit rose significantly by 26.97% to NPR 3.10 billion, compared to NPR 2.45 billion last year. This underscores the bank’s ability to control expenses while growing revenues.

Key Ratios and Indicators

Earnings Per Share (EPS):

The bank’s EPS improved by 2.94, reaching NPR 32.06. This increase reflects higher returns for shareholders.

Net Worth Per Share:

Everest Bank’s net worth per share stood at NPR 225.79, indicating a solid financial base and higher equity strength.

PE Ratio:

The PE Ratio remained stable at 18.12, showing consistent valuation levels relative to earnings growth.

Base Rate and Interest Rate Spread:

The base rate decreased significantly from 8.87% in Poush 2080 to 5.84% in Poush 2081. This drop in base rate makes Everest Bank’s loans more competitive, which is likely to attract more borrowers.

The interest rate spread slightly decreased from 4.00% to 3.99%, indicating tighter margins on interest-based income.

Deposits and Loans

Customer Deposits:

The bank’s deposits grew by 7.80%, reaching NPR 250.43 billion, a testament to Everest Bank’s reputation and customer confidence.

Loan Portfolio:

Loans and advances increased significantly by 16.96%, totaling NPR 208.43 billion. This reflects the bank’s focus on expanding credit facilities while maintaining asset quality.

Loan-to-Deposit Ratio (LDR):

The LDR increased to 85.39%, indicating efficient utilization of customer deposits in revenue-generating loans.

Challenges Ahead

Declining Base Rate:

While the lower base rate attracts borrowers, it poses a challenge for maintaining net interest margins if lending volumes do not increase proportionally.

Asset Quality:

Although impairment charges have decreased, the bank must remain vigilant to ensure non-performing loans (NPLs) do not rise amid potential economic uncertainties.

Everest Bank’s second-quarter performance indicates strong operational resilience and strategic focus on revenue growth. The increase in core income streams like interest and fees, coupled with reduced impairment charges, highlights efficient management practices. However, the bank needs to navigate challenges such as tightening margins and competitive pressures in the lending market.

The growth in deposits and loans reflects the bank’s increasing market penetration, while improved shareholder returns, as evidenced by higher EPS, solidifies its position as one of Nepal’s leading banks. Moving forward, Everest Bank must balance growth and risk management to sustain its upward trajectory.