हिमालयन बैंकको दोस्रो त्रैमास: नाफा वृद्धि सीमित, ब्याज आम्दानी घट्दोHimalayan Bank Reports Financial Performance for Second Quarter, FY 2081: Marginal Growth in Net Profit Despite Challenging Conditions

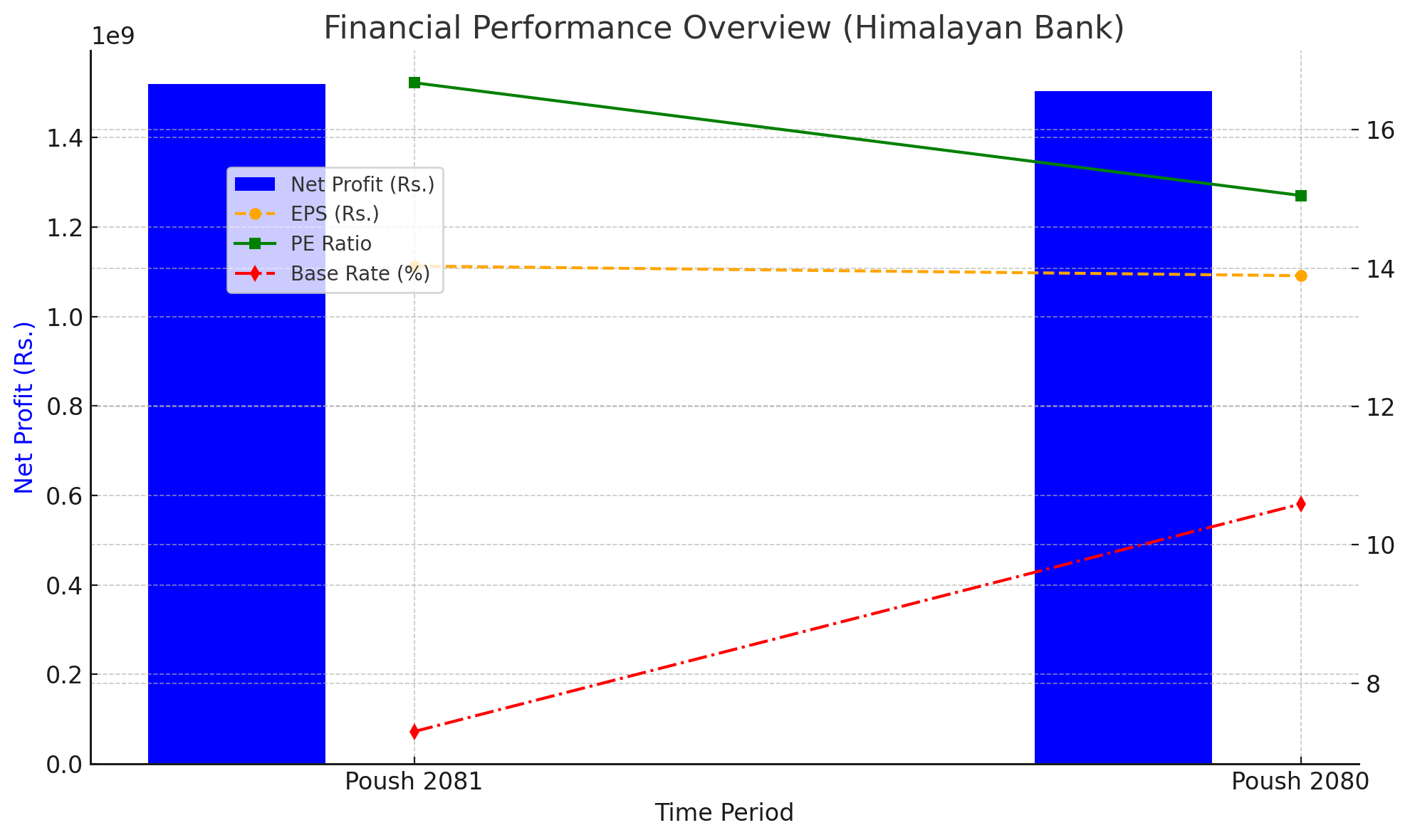

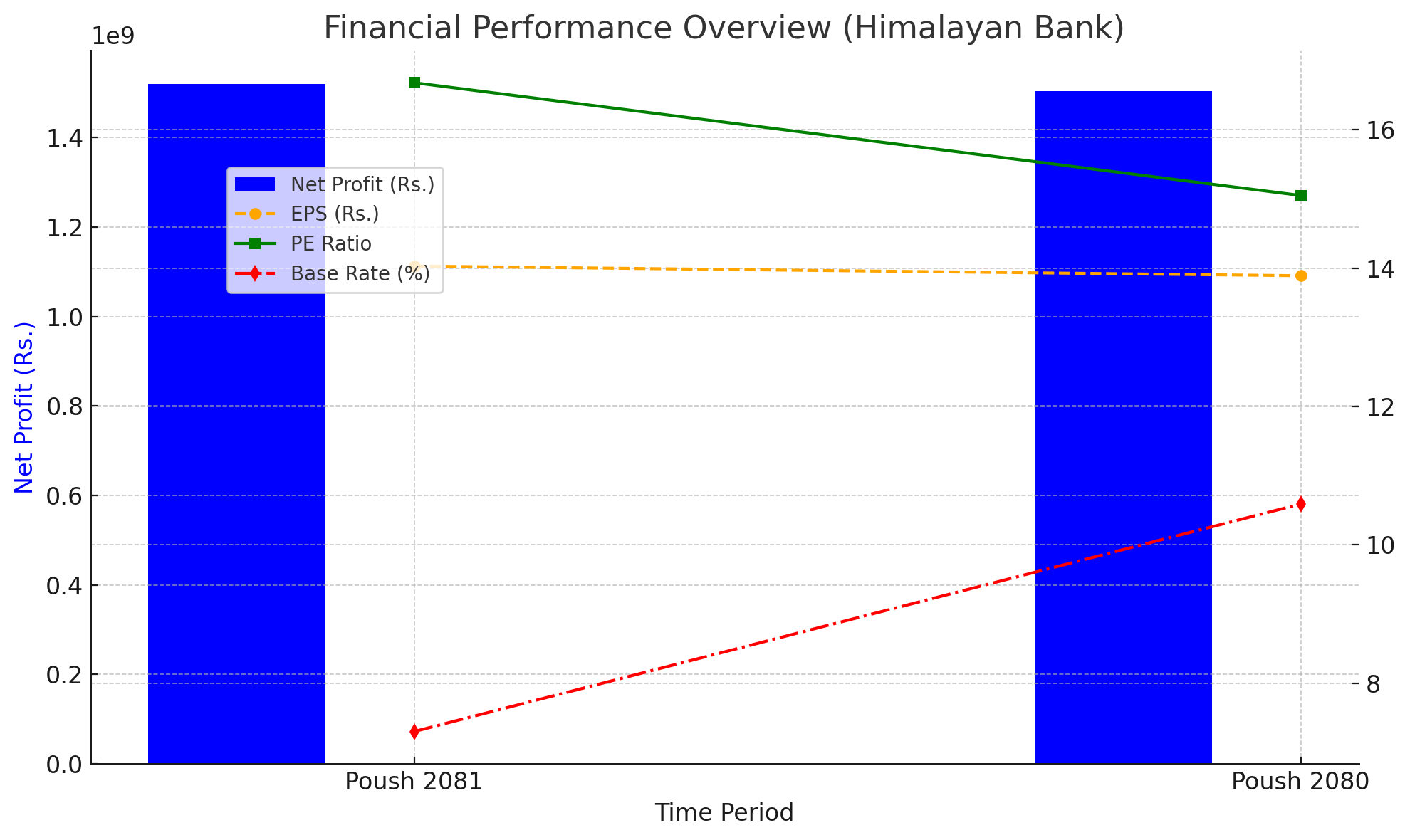

हिमालयन बैंक लिमिटेड (HBL) ले आर्थिक वर्ष २०८१ को दोस्रो त्रैमाससम्मको अपरिष्कृत वित्तीय विवरण सार्वजनिक गरेको छ। विवरण अनुसार, बैंकको खुद नाफा गत वर्षको सोही अवधिको तुलनामा थोरै सुधार देखिएको छ। बैंकले चालु त्रैमासमा १ अर्ब ५१ करोड ८७ लाख रुपैयाँ खुद नाफा आर्जन गरेको छ, जुन गत वर्षको १ अर्ब ५० करोड ३९ लाख रुपैयाँ भन्दा ०.९८ प्रतिशतले बढी हो।

नाफामा सामान्य वृद्धि

बैंकले चालु त्रैमासमा १ अर्ब ५१ करोड ८७ लाख रुपैयाँ खुद नाफा आर्जन गरेको छ। यो वृद्धि ब्याज आम्दानी र कमिशन आम्दानीमा भएको गिरावटका बाबजुद हासिल भएको हो।

ब्याज र कमिशन आम्दानीमा गिरावट

बैंकको खुद ब्याज आम्दानी गत वर्षको तुलनामा १०.०४ प्रतिशतले घटेर ५ अर्ब २३ करोड रुपैयाँमा झरेको छ।

त्यस्तै, खुद फि तथा कमिशन आम्दानी पनि १३.१२ प्रतिशतले घटेर ४५ करोड ६९ लाख रुपैयाँमा सीमित भएको छ।

कुल सञ्चालन आम्दानीमा गिरावट

बैंकको कुल सञ्चालन आम्दानी गत वर्षको ६ अर्ब ६० करोड रुपैयाँबाट घटेर ६ अर्ब ७ करोड रुपैयाँमा झरेको छ, जसले मुख्य आम्दानीका स्रोतहरूमा आएको दबाबलाई संकेत गर्छ।

इम्पेरमेन्ट चार्जमा भारी कमी

बैंकले इम्पेरमेन्ट चार्जलाई १ अर्ब ९४ करोड रुपैयाँबाट घटाएर १८ करोड ४६ लाख रुपैयाँमा झारेको छ। यसले सञ्चालन मुनाफालाई ४१.२२ प्रतिशतले बढाएर ३ अर्ब १२ करोड रुपैयाँ पुर्याएको छ।

प्रति शेयर आम्दानी (EPS) र शेयरधनीको नेटवर्थ

बैंकको EPS १४ पैसा बढेर १४ रुपैयाँ ३ पैसामा पुगेको छ।

त्यस्तै, प्रति शेयर नेटवर्थ १७६ रुपैयाँ ११ पैसा रहेको छ, जसले बैंकको सुदृढ पूँजी संरचनालाई देखाउँछ।

निक्षेप र कर्जामा सामान्य वृद्धि

बैंकले पुस मसान्तसम्म २ खर्ब ९८ अर्ब रुपैयाँ निक्षेप संकलन गरेको छ, जुन गत वर्षको तुलनामा १.५० प्रतिशतले बढी हो।

त्यस्तै, कर्जामा ०.२० प्रतिशतको वृद्धि हुँदै २ खर्ब ३० अर्ब रुपैयाँ पुगेको छ।

ब्याज दरको अन्तर घट्यो

बैंकको ब्याज दरको अन्तर (Interest Rate Spread) ४.६२ प्रतिशतबाट घटेर ३.९८ प्रतिशतमा झरेको छ। त्यस्तै, आधार दर (Base Rate) पनि १०.५९ प्रतिशतबाट घटेर ७.३० प्रतिशतमा पुगेको छ।

वितरणयोग्य मुनाफा ऋणात्मक

बैंकको वितरणयोग्य मुनाफा भने अझै पनि ऋणात्मक अवस्थामा छ। पुस मसान्तसम्म यो मुनाफा ३ अर्ब ९५ करोड ९ लाख रुपैयाँ ऋणात्मक छ, जसले शेयरधनीलाई लाभांश वितरणमा चुनौती उत्पन्न गरिरहेको छ।

हिमालयन बैंकको वित्तीय प्रदर्शनले मिश्रित संकेत देखाउँछ। एकातिर, इम्पेरमेन्ट चार्जमा भएको भारी कटौती र पूँजीको बलियो स्थिति बैंकको नाफा वृद्धिमा मुख्य कारक बनेका छन्। अर्कोतिर, ब्याज र फि आम्दानीमा आएको गिरावटले परम्परागत बैंकिङ व्यवसायमा चुनौती देखाएको छ।

ब्याज दरको अन्तर र आधार दरमा आएको कमीले बैंकिङ क्षेत्रमा बढ्दो प्रतिस्पर्धा र जोखिम व्यवस्थापनलाई संकेत गर्छ। साथै, ऋणात्मक वितरणयोग्य मुनाफाले बैंकलाई निकट भविष्यमा लाभांश वितरणमा कठिनाइ निम्त्याउने सम्भावना देखिन्छ।

हिमालयन बैंकले चुनौतीपूर्ण वातावरणमा पनि सन्तुलित वित्तीय प्रदर्शन कायम राखेको छ। तर, यसले आय स्रोतको विविधीकरण र सञ्चालन लागतमा थप सुधार आवश्यक रहेको देखाउँछ। डिजिटल परिवर्तन र ग्राहकसँगको सम्पर्क सुधार गर्ने योजनाले दीर्घकालीन वृद्धिलाई बल पुर्याउन सक्छ।

बैंकको यस प्रदर्शनले स्थिरता देखाए पनि, प्रतिस्पर्धात्मक बजारमा निरन्तरता कायम राख्न अझ रणनीतिक कदमहरू आवश्यक देखिन्छ।

Himalayan Bank Limited (HBL) has unveiled its unaudited financial report for the second quarter of FY 2081 (ending Poush 2081), showing a slight improvement in profitability despite significant declines in key income streams. The bank reported a net profit of NPR 1.52 billion, a marginal 0.98% increase compared to NPR 1.50 billion in the same period of FY 2080.

Net Profit Marginally Up

The bank achieved a net profit of NPR 1.518 billion in Poush 2081, up from NPR 1.503 billion in Poush 2080, representing a modest growth of 0.98%. This improvement occurred despite notable declines in the bank's core income sources.

Decline in Interest and Fee-Based Income

Net Interest Income (NII), the primary revenue source for the bank, decreased by 10.04% year-on-year, from NPR 5.82 billion to NPR 5.23 billion. The decline reflects the pressures of a challenging interest rate environment and reduced lending margins.

Similarly, Net Fee and Commission Income dropped by 13.12%, from NPR 526 million to NPR 457 million. This signals reduced transaction volumes or lower fee generation capabilities.

Total Operating Income Weakens

Total Operating Income decreased by 8.03%, falling from NPR 6.61 billion in Poush 2080 to NPR 6.07 billion in Poush 2081. This decline underlines the impact of weaker interest and fee income on overall operational performance.

Sharp Reduction in Impairment Charges

A key factor driving the profit growth was a substantial reduction in impairment charges. The bank reduced these charges from NPR 1.95 billion in Poush 2080 to a mere NPR 184.6 million in the current period. This reflects improved asset quality and reduced provisioning requirements, which helped offset the decline in core revenue.

Operating Profit Surges

Despite lower operating income, the reduced impairment charges enabled the bank's operating profit to increase significantly by 41.22%, from NPR 2.21 billion to NPR 3.12 billion. This highlights the bank's success in managing operational costs and asset quality effectively.

Earnings Per Share (EPS) and Shareholders’ Equity

EPS saw a marginal increase of 14 paisa, rising to NPR 14.03 from NPR 13.89 in the same period last year.

The bank's net worth per share stood at NPR 176.11, an increase from NPR 162.17, underscoring a solid capital base.

Deposits and Loans Growth

Deposits from customers reached NPR 298.3 billion, growing by 1.50% from NPR 293.9 billion in the same period last year. Loans and advances to customers also grew slightly by 0.20%, reaching NPR 230.7 billion.

The modest growth in both deposits and lending reflects a cautious banking approach amidst economic uncertainties.

Declining Margins

The bank's interest rate spread narrowed to 3.98%, compared to 4.62% in Poush 2080. This reduction in spread, coupled with a significant drop in the base rate from 10.59% to 7.30%, highlights pressure on the bank’s lending profitability.

Distributable Profit Remains Negative

Despite profitability at the operational level, the bank’s distributable profit remains negative at NPR 3.95 billion. This indicates that the bank may face challenges in providing dividends or other distributions to shareholders in the near term.

The financial performance of Himalayan Bank highlights a mixed picture. On one hand, the reduction in impairment charges and strong capital reserves have enabled the bank to maintain a slight profit growth. On the other hand, declining core revenue streams, such as net interest income and fee-based income, underline the challenges posed by the current economic environment and reduced lending margins.

The narrowing interest rate spread and sharp drop in the base rate suggest heightened competition in the lending market and a more conservative lending approach. This could be due to lower credit demand, increased regulatory oversight, or cautious risk management policies. Furthermore, the negative distributable profit signals that the bank has accumulated significant unrealized losses or provisions, limiting its ability to return value to shareholders in the short term.

Himalayan Bank's performance in the second quarter showcases its resilience in navigating economic headwinds. However, the declining revenue from core banking operations underscores the need to diversify income streams and enhance efficiency. To sustain long-term growth, the bank may need to:

Expand its non-interest income sources through innovative fee-based products and services.

Strengthen its cost optimization strategies to counter declining revenue.

Focus on digital transformation to improve customer engagement and operational efficiency.

While the bank has successfully improved asset quality, as evidenced by the reduction in impairment charges, maintaining profitability amidst a challenging macroeconomic environment will require a balanced approach to growth and risk management.

This report highlights Himalayan Bank’s commitment to stability, but also the hurdles it faces in an increasingly competitive and regulated banking landscape.