निजी क्षेत्रमा कर्जा प्रवाहमा वृद्धि: चालु आर्थिक वर्षको पहिलो महिनामा १४ अर्ब ११ करोड थप कर्जा प्रवाहIncrease in Credit Flow to the Private Sector: An Additional NPR 14.11 Billion in Credit Disbursed in the First Month of the Current Fiscal Year

चालु आर्थिक वर्षको पहिलो महिनामा बैंक तथा वित्तीय संस्थाहरूबाट निजी क्षेत्रमा प्रवाहित कर्जा १४ अर्ब ११ करोड रुपैयाँ (०.३ प्रतिशत) ले वृद्धि भएको छ। यो वृद्धि अघिल्लो वर्षको सोही अवधिमा ४ अर्ब ३५ करोड रुपैयाँ (०.१ प्रतिशत) ले घटेको अवस्थासँग तुलना गर्दा सकारात्मक संकेत हो।

वार्षिक वृद्धि:

२०८१ साउन मसान्तमा बैंक तथा वित्तीय संस्थाहरूबाट निजी क्षेत्रतर्फ प्रवाहित कर्जा ६.२ प्रतिशतले वृद्धि भएको छ।

क्षेत्रगत कर्जा प्रवाह:

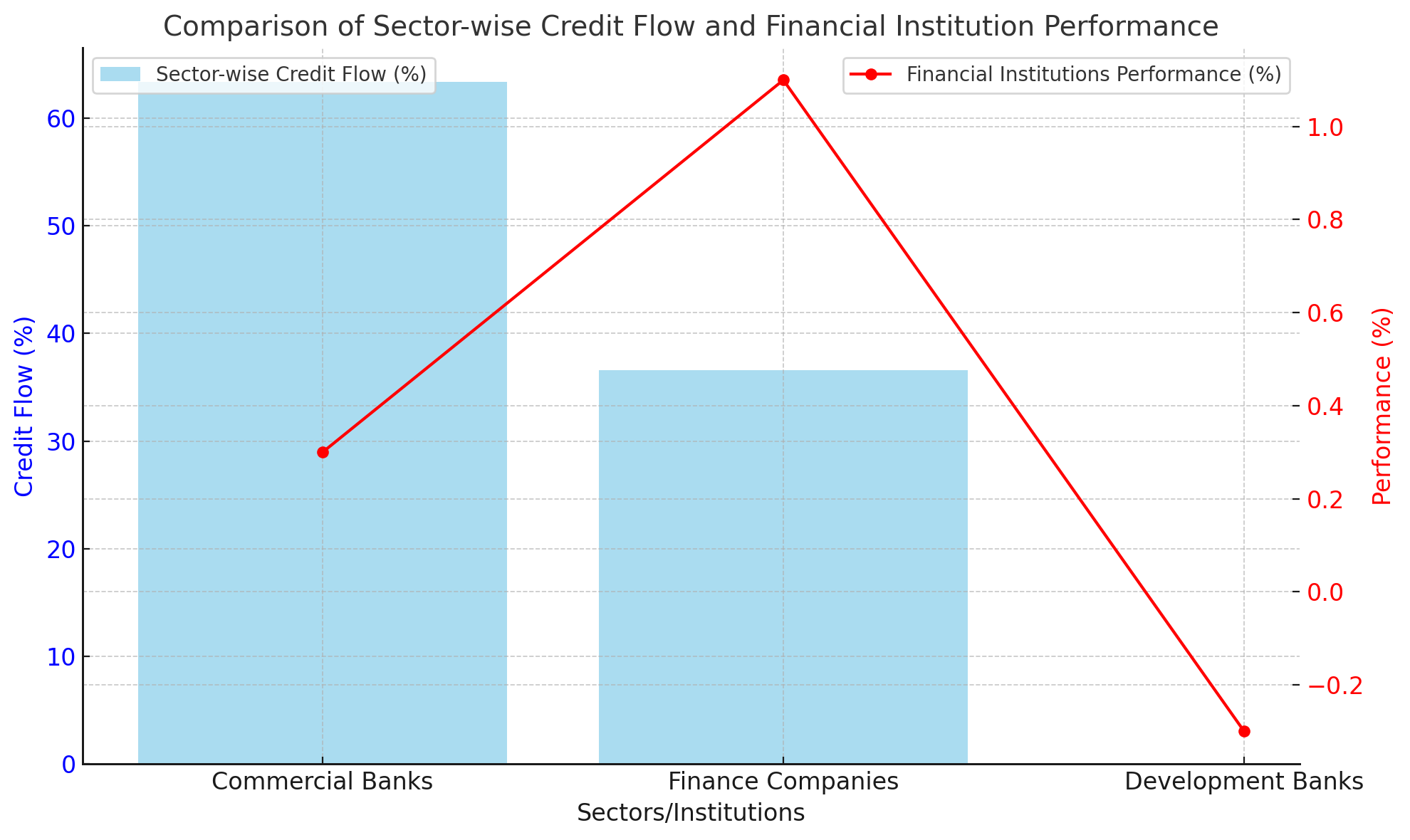

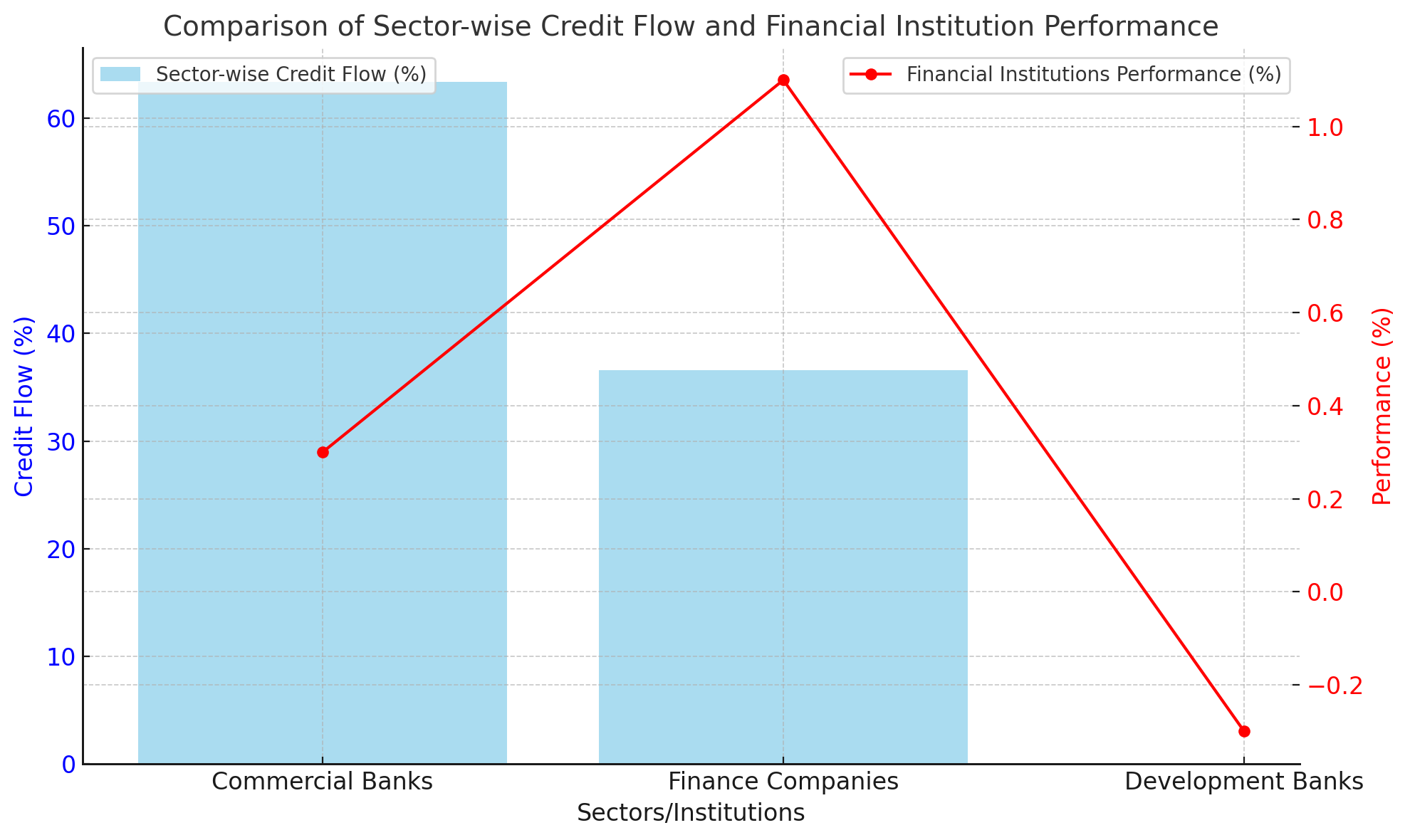

गैर–वित्तीय संस्थागत क्षेत्र: ६३.४ प्रतिशत कर्जा प्रवाह, अघिल्लो वर्षको तुलनामा केहि घटेको (अघिल्लो वर्ष ६४.० प्रतिशत)।

व्यक्तिगत तथा घरपरिवार क्षेत्र: ३६.६ प्रतिशत कर्जा प्रवाह, अघिल्लो वर्षको तुलनामा वृद्धि (अघिल्लो वर्ष ३६.० प्रतिशत)।

वित्तीय संस्थाहरूको प्रदर्शन:

वाणिज्य बैंकहरू: कर्जा प्रवाहमा ०.३ प्रतिशतले वृद्धि।

वित्त कम्पनीहरू: कर्जा प्रवाहमा १.१ प्रतिशतले वृद्धि।

विकास बैंकहरू: कर्जा प्रवाहमा ०.३ प्रतिशतले घटेको।

धितो सुरक्षण:

चालु सम्पत्ति (कृषि तथा गैर-कृषिजन्य वस्तु): १३.३ प्रतिशत कर्जा सुरक्षण, अघिल्लो वर्ष १२.१ प्रतिशत।

घर जग्गा धितो सुरक्षण: ६६.३ प्रतिशत कर्जा सुरक्षण, अघिल्लो वर्ष ६७.१ प्रतिशत।

कर्जा प्रवाहका क्षेत्रगत बिस्तार:

कर्जा प्रवाहमा वृद्धि भएका क्षेत्रहरू: कृषि (०.५%), औद्योगिक उत्पादन (०.१%), यातायात, सञ्चार तथा सार्वजनिक सेवा (१.६%), सेवा उद्योग (०.६%), उपभोग्य क्षेत्र (०.१%)।

कर्जा प्रवाहमा घटेका क्षेत्रहरू: निर्माण (०.४%), थोक तथा खुद्रा व्यापार (०.२%)।

कर्जा प्रकारहरूमा वृद्धि/घटावट:

बढेका कर्जा: आवधिक कर्जा (०.३%), मार्जिन प्रकृतिको कर्जा (१.५%), ट्रष्ट रिसिट (आयात) कर्जा (९.४%), हायर पर्चेज कर्जा (०.०३%), रियल स्टेट कर्जा (०.१%)।

घटेका कर्जा: अधिविकर्ष कर्जा (३%), नगद प्रवाह कर्जा (०.२%)।

समग्रमा, चालु आर्थिक वर्षको पहिलो महिनामा बैंक तथा वित्तीय संस्थाहरूको कर्जा प्रवाहमा केहि सुधार देखिएको छ, जसले नेपाली अर्थतन्त्रमा केही स्थिरता र सकारात्मकता ल्याएको छ। तथापि, क्षेत्रगत आधारमा कर्जा प्रवाहमा विविधता रहेकोले अझै सुधारको आवश्यकता छ।

In the first month of the current fiscal year, credit disbursed by banks and financial institutions to the private sector increased by NPR 14.11 billion, representing a 0.3% growth. This growth is a positive indicator, especially when compared to the same period last year, which saw a decline of NPR 4.35 billion (0.1%).

Annual Growth:

As of the end of Shrawan 2081, credit disbursed to the private sector by banks and financial institutions increased by 6.2%.

Sector-wise Credit Flow:

Non-financial Institutional Sector: 63.4% of the total credit was disbursed to this sector, slightly down from 64.0% last year.

Individual and Household Sector: 36.6% of the total credit was disbursed to this sector, up from 36.0% last year.

Performance of Financial Institutions:

Commercial Banks: Credit flow increased by 0.3%.

Finance Companies: Credit flow increased by 1.1%.

Development Banks: Credit flow decreased by 0.3%.

Collateral Security:

Current Assets (Agricultural and Non-Agricultural Goods): Collateral security accounted for 13.3% of the total credit, up from 12.1% last year.

Real Estate Collateral Security: Collateral security accounted for 66.3% of the total credit, down from 67.1% last year.

Sectoral Expansion of Credit Flow:

Sectors with Increased Credit Flow: Agriculture (0.5%), Industrial Production (0.1%), Transport, Communication, and Public Service (1.6%), Service Industry (0.6%), Consumer Sector (0.1%).

Sectors with Decreased Credit Flow: Construction (0.4%), Wholesale and Retail Trade (0.2%).

Increase/Decrease in Types of Loans:

Increased Loans: Term Loans (0.3%), Margin Loans (1.5%), Trust Receipt (Import) Loans (9.4%), Hire Purchase Loans (0.03%), Real Estate Loans (0.1%).

Decreased Loans: Overdraft Loans (3%), Cash Flow Loans (0.2%).

Overall, the first month of the current fiscal year has shown some improvement in credit disbursement by banks and financial institutions, contributing to some stability and positivity in the Nepalese economy. However, sectoral diversity in credit flow suggests that there is still room for improvement.