नेपाल इन्भेष्टमेन्ट मेगा बैंकको वित्तीय विवरण: मुनाफामा उल्लेख्य सुधारNepal Investment Mega Bank's Financial Performance: Significant Profit Growth

नेपाल इन्भेष्टमेन्ट मेगा बैंक लिमिटेडले चालु आर्थिक वर्ष २०८१/८२ को दोस्रो त्रैमाससम्मको अपरिष्कृत वित्तीय विवरण सार्वजनिक गरेको छ। विवरण अनुसार, बैंकको नाफा गत वर्षको तुलनामा उल्लेखनीय रूपमा सुधार भएको देखिन्छ।

खुद नाफामा ५७ प्रतिशत वृद्धि

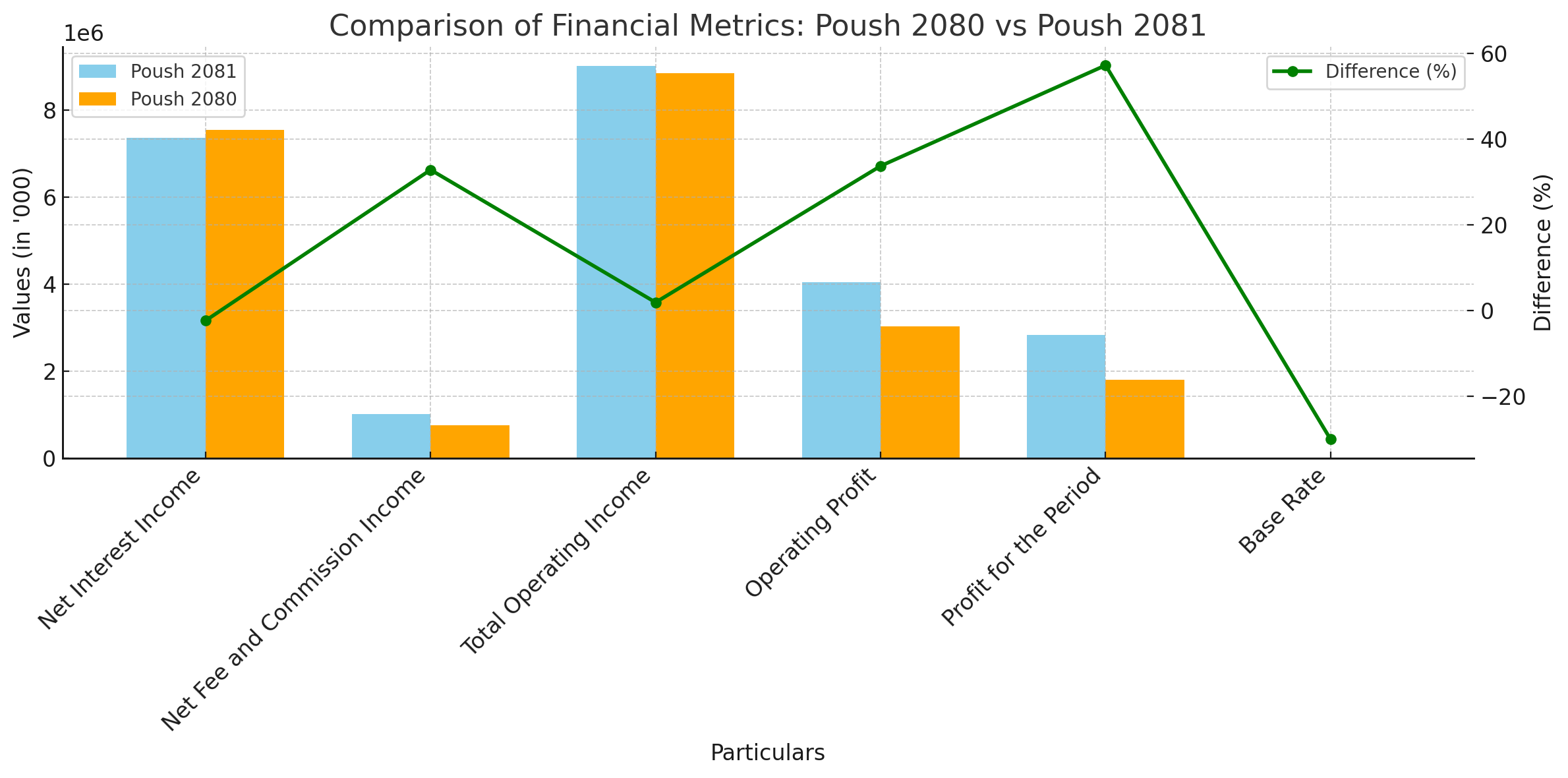

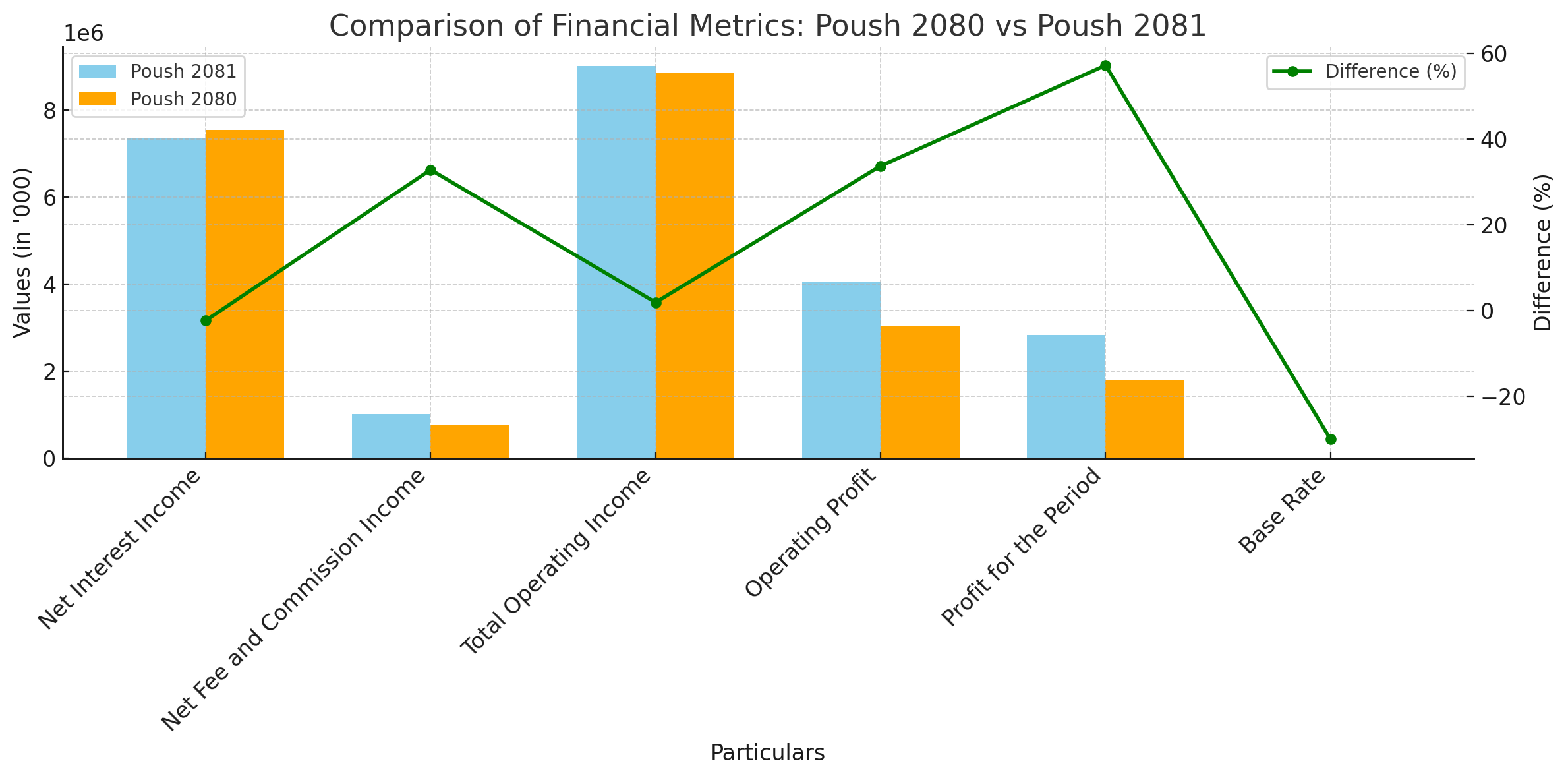

बैंकले चालु आर्थिक वर्षको पुस मसान्तसम्म २ अर्ब ८३ करोड २३ लाख रुपैयाँ खुद नाफा कमाएको छ, जुन गत वर्षको सोही अवधिमा कमाएको १ अर्ब ८० करोड १९ लाख रुपैयाँभन्दा ५७.१८ प्रतिशतले बढी हो। यस वृद्धि मुख्यत: इम्पेरमेन्ट चार्जमा कमी आएको कारणले भएको हो। गत वर्षको तुलनामा इम्पेरमेन्ट चार्ज २ अर्ब ८६ करोड ७८ लाख रुपैयाँबाट घटेर १ अर्ब ७७ करोड २५ लाख रुपैयाँमा झरेको छ।

आम्दानीका मुख्य सूचकहरू

बैंकको खुद ब्याज आम्दानी ७३ करोड ६५ लाखमा सीमित हुँदा २.३७ प्रतिशतले घटेको छ। तर, खुद फि तथा कमिशन आम्दानी ३२.८ प्रतिशतले बढेर १० करोड ५ लाख पुगेको छ। साथै, बैंकको कुल सञ्चालन आम्दानी पनि १.८७ प्रतिशतले वृद्धि भएको छ।

सञ्चालन मुनाफामा सुधार

समीक्षा अवधिमा बैंकको सञ्चालन मुनाफा ३३.६९ प्रतिशतले बढेर ४ अर्ब ४ करोड रुपैयाँ पुगेको छ। यो मुख्यत: ब्याज आम्दानीको न्यून गिरावट र अन्य सञ्चालन खर्चहरूको कुशल व्यवस्थापनको परिणाम हो।

वित्तीय सूचकहरूमा प्रगति

बैंकको प्रतिशेयर आम्दानी (EPS) १०.५६ बाट १६.६० रुपैयाँ पुगेको छ, जसले बैंकको लाभप्रदता संकेत गर्दछ। त्यस्तै, बैंकको प्रतिशेयर नेटवर्थ १८५ रुपैयाँ पुगेको छ। बैंकको मूल्य आम्दानी अनुपात (PE Ratio) १२.७१ गुणा रहेको छ, जसले लगानीकर्ताहरूले बैंकको शेयर मूल्यको तुलनामा कमाएको आम्दानीको दर संकेत गर्दछ।

निक्षेप र कर्जा व्यवस्थापन

बैंकले पुस मसान्तसम्म ४ खर्ब ४० अर्ब रुपैयाँ निक्षेप संकलन गरेको छ, जुन ९.२९ प्रतिशतले वृद्धि भएको हो। त्यस्तै, बैंकले ३ खर्ब २८ अर्ब रुपैयाँ कर्जा लगानी गरेको छ, जुन ७.६३ प्रतिशतले बढेको छ।

आधार दर र ऋण–निक्षेप अनुपात

बैंकको आधार दर ६.५८ प्रतिशत रहेको छ, जुन गत वर्षको ९.४१ प्रतिशतको तुलनामा कम हो। यसले बैंकले कर्जाको लागत घटाएको संकेत गर्दछ। तर, बैंकको क्रेडिट–डिपोजिट अनुपात ७८.८७ प्रतिशत रहेको छ, जुन सन्तुलित स्तरमा छ।

बैंकले आफ्नो सञ्चालनमा कुशल व्यवस्थापन गर्दै लाभप्रदतालाई सुधार गरेको छ। खुद नाफा र EPS मा भएको वृद्धि लगानीकर्ताहरूका लागि सकारात्मक संकेत हो। तर, ब्याज आम्दानीमा आएको गिरावटलाई दीर्घकालीन रूपमा सम्बोधन गर्न बैंकले नयाँ रणनीति अपनाउनुपर्ने देखिन्छ।

इम्पेरमेन्ट चार्ज घटाउँदै सञ्चालन खर्चमा नियन्त्रण राख्नु बैंकको मुख्य उपलब्धि हो। अब बैंकले कर्जाका नयाँ क्षेत्रहरूमा लगानी बढाउँदै ब्याज आम्दानी सुधार गर्नुपर्ने आवश्यक छ।

Nepal Investment Mega Bank Limited has published its unaudited financial report for the second quarter of the fiscal year 2081/82. The report highlights remarkable improvements in profitability compared to the same period last year.

Net Profit Increases by 57%

As of Poush 2081, the bank has recorded a net profit of NPR 2.83 billion, marking a 57.18% increase compared to NPR 1.80 billion in the same period last year. This growth is primarily driven by a reduction in impairment charges, which decreased from NPR 2.87 billion to NPR 1.77 billion.

Key Income Indicators

The bank's net interest income has slightly declined by 2.37% to NPR 7.36 billion. However, net fee and commission income surged by 32.80%, reaching NPR 1.01 billion. Additionally, total operating income grew by 1.87%, reflecting the bank's ability to manage revenue streams effectively.

Improved Operating Profit

The bank's operating profit increased by 33.69% to NPR 4.04 billion during the review period. This improvement is attributed to effective cost management and a reduction in impairment charges, despite the slight decline in interest income.

Progress in Financial Metrics

The bank's Earnings Per Share (EPS) rose significantly from NPR 10.56 to NPR 16.60, indicating improved profitability. Similarly, the net worth per share increased to NPR 185.00. The Price-to-Earnings (PE) ratio stands at 12.71 times, reflecting a reasonable valuation for investors.

Deposit and Loan Management

As of Poush 2081, the bank has mobilized deposits amounting to NPR 440.88 billion, a 9.29% increase compared to last year. Loans and advances to customers have grown by 7.63%, reaching NPR 328.79 billion.

Base Rate and Credit-to-Deposit Ratio

The bank's base rate has decreased from 9.41% to 6.58%, indicating lower borrowing costs for customers. Meanwhile, the credit-to-deposit ratio is at 78.87%, which reflects prudent liquidity management.

Nepal Investment Mega Bank has demonstrated strong operational efficiency and profitability growth in the second quarter. The increase in net profit and EPS is a positive signal for investors. However, the decline in net interest income suggests that the bank may need to explore new avenues to sustain revenue growth in the long term.

The reduction in impairment charges and cost control measures have been the bank's significant achievements. Going forward, the bank should focus on increasing its interest income by tapping into new lending sectors and expanding its customer base.