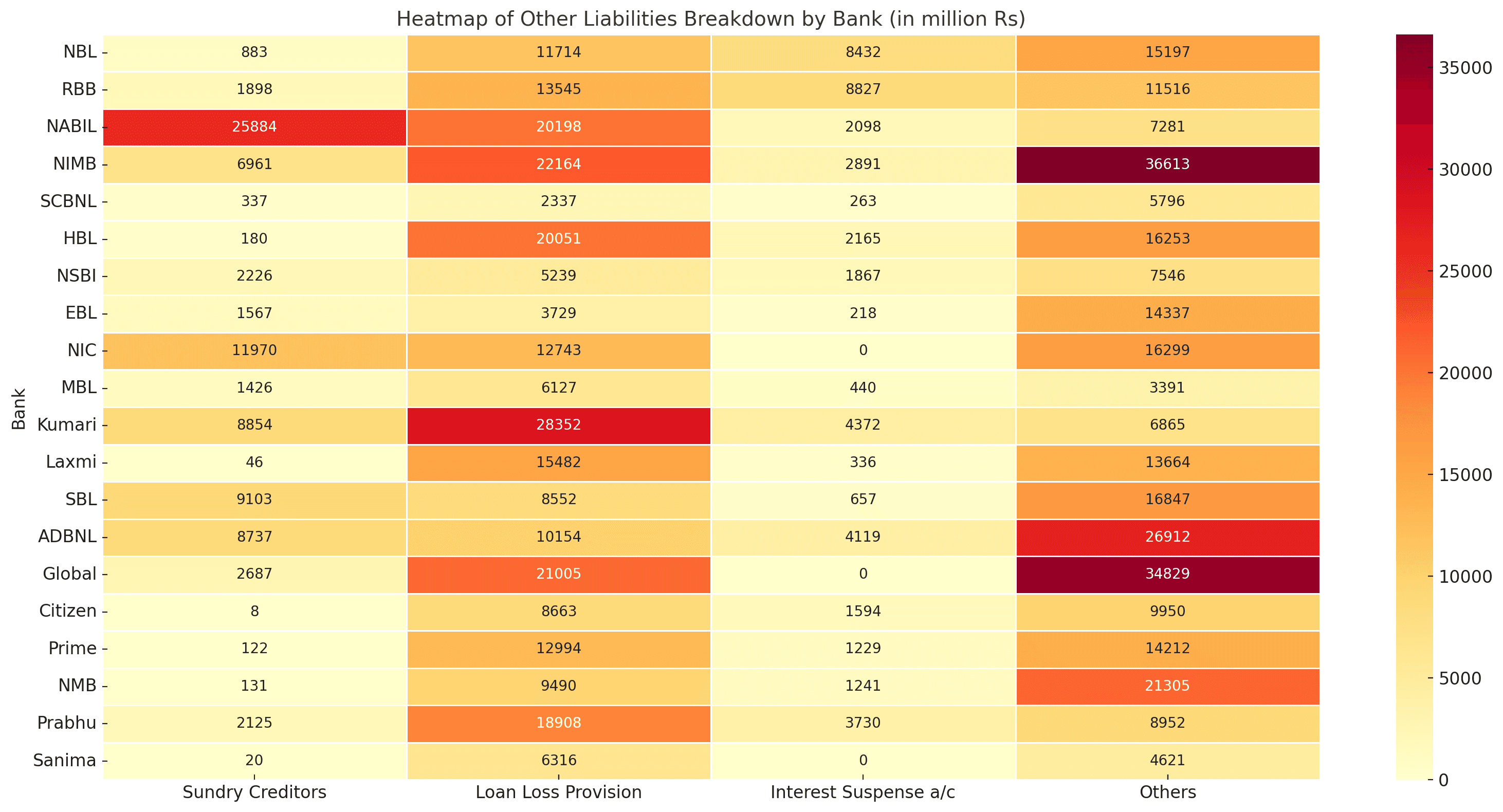

नेपालका वाणिज्य बैंकहरूले आर्थिक वर्ष २०८२ को जेठ मसान्तसम्ममा रिपोर्ट गरेका ‘अन्य दायित्व’ (Other Liabilities) मा उल्लेखनीय वृद्धि देखिएको छ। यी दायित्वहरूमा सन्ड्री क्रेडिटर्स, कर्जा नोक्सानी प्रावधान (Loan Loss Provision), ब्याज निलम्बन खाता (Interest Suspense a/c), तथा अन्य विभिन्न दायित्व समावेश छन्, जसले बैंकको आन्तरिक जोखिम र आर्थिक व्यवस्थापनको अवस्था झल्काउँछ।

सवैभन्दा बढी अन्य दायित्व भएको बैंक एनआईएमबी (NIMB) हो, जसको जम्मा रकम ६८.६३ अर्ब रुपैयाँ रहेको छ। यसमा ३६.६१ अर्ब अन्य दायित्वमा र २२.१६ अर्ब कर्जा नोक्सानी प्रावधानमा छुट्याइएको छ। ग्लोबल आइएमई बैंक दोस्रो स्थानमा छ, जसको ५८.५२ अर्ब रुपैयाँ अन्य दायित्व छ भने त्यसमा २१.०५ अर्ब कर्जा प्रावधान र ३४.८२ अर्ब अन्य दायित्व छन्।

नबिल बैंकको अन्य दायित्व ५५.४६ अर्ब रुपैयाँ पुगेको छ, जसमा सन्ड्री क्रेडिटर्स अन्तर्गत मात्रै २५.८८ अर्ब रहेको छ — जुन यो शीर्षकमा सबैभन्दा बढी हो।

स्ट्यान्डर्ड चार्टर्ड बैंक (SCBNL) र सनिमा बैंक जस्ता संस्थाहरूले कम दायित्व रिपोर्ट गरेका छन् — क्रमशः ८.७३ अर्ब र १०.९५ अर्ब। यसले या त उनीहरूको संरचना सरल रहेको वा बढी सतर्क वित्तीय नीति अपनाएको देखाउँछ।

कर्जा नोक्सानी प्रावधान लगभग सबै बैंकहरूमा उच्च देखिएको छ। कुमारी बैंकले २८.३५ अर्ब तथा लक्ष्मी बैंकले १५.४८ अर्ब छुट्याएको छ, जुन सम्भावित ‘नपाउने कर्जा’ का जोखिमलाई सम्बोधन गर्न गरिएको तयारी हो।

ब्याज निलम्बन खाता अधिकांश बैंकहरूमा मध्यम देखिएको छ। एनआईसी, ग्लोबल, र सनिमा बैंकहरूले यो शीर्षकमा रकम उल्लेख नगरेको पाइन्छ, जसले या त उनीहरूको कर्जा असुली अवस्था राम्रो रहेको वा लेखा नीति भिन्न रहेको देखाउँछ।

‘अन्य’ दायित्व अत्यन्त ठूलो र अस्पष्ट क्षेत्र हो। एनआईएमबीमा मात्र ३६.६१ अर्ब, र ग्लोबलमा ३४.८२ अर्ब रुपैयाँ रहेको देखिन्छ। यसले पारदर्शिता अभावलाई देखाउँछ र नियामक निकायबाट थप अनुगमनको आवश्यकता औंल्याउँछ।

निष्कर्षमा, कर्जा नोक्सानीको प्रावधानले बैंकहरूको जोखिम सजगता देखाउँछ भने सन्ड्री क्रेडिटर्स र अन्य दायित्वहरूमा भएको वृद्धिले अल्पकालीन दायित्वको चाप वा आन्तरिक व्यवस्थापनमा कमजोरी संकेत गर्छ। आगामी त्रैमासिक विवरणमा यी दायित्वहरूको विस्तृत विश्लेषण र पारदर्शिता अत्यावश्यक देखिन्छ।