Top

Inflation and Investment: Why Keeping Money Idle Is the Costliest Financial Decision

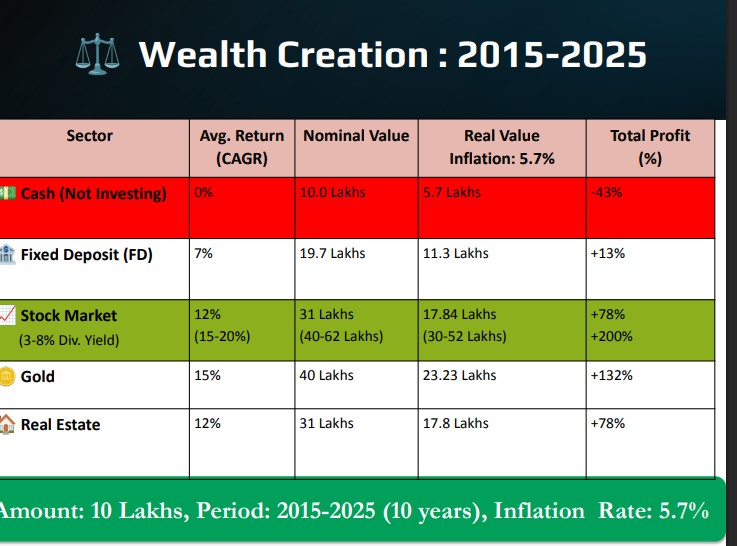

Inflation and Investment: Why Keeping Money Idle Is the Costliest Financial Decision A decade-long comparison of different investment options reveals a striking reality about wealth creation: money that remains idle gradually loses its value due to inflation. Financial data covering the period 2015 to 2025 suggests that individuals who chose not to invest their savings experienced a significant decline in purchasing power. For example, a cash amount of Rs. 10 lakh held without investment over ten years effectively falls to around Rs. 5.7 lakh in real value, implying a loss of about 43 percent when adjusted for inflation.

Dipesh Ghimire

3 min read

A decade-long comparison of different investment options reveals a striking reality about wealth creation: money that remains idle gradually loses its value due to inflation. Financial data covering the period 2015 to 2025 suggests that individuals who chose not to invest their savings experienced a significant decline in purchasing power. For example, a cash amount of Rs. 10 lakh held without investment over ten years effectively falls to around Rs. 5.7 lakh in real value, implying a loss of about 43 percent when adjusted for inflation.

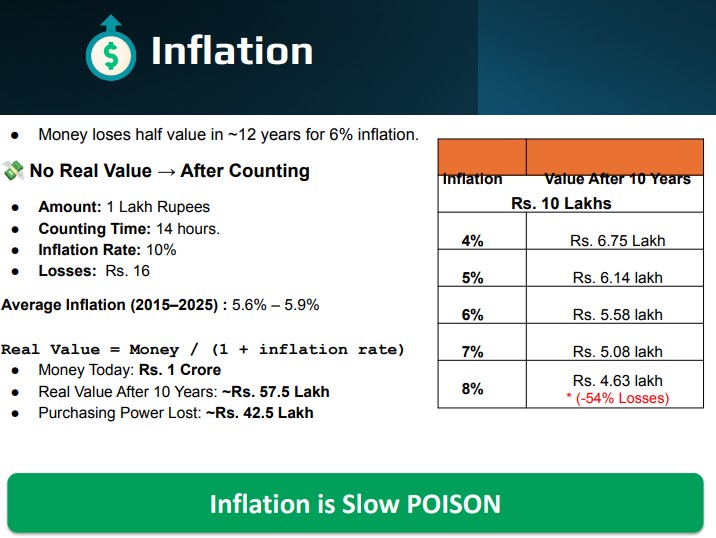

This decline highlights the silent but powerful effect of inflation, which averaged roughly 5.6 to 5.9 percent during the decade. Economists often describe inflation as a “hidden tax” on savings because it steadily erodes the purchasing capacity of money. Even when the nominal value of cash remains unchanged, its ability to buy goods and services decreases over time. At an inflation rate of around six percent, the real value of money can effectively be cut in half within about twelve years, making long-term wealth preservation impossible without investment.

The comparison of major asset classes over the same period presents a different picture. Fixed deposits, traditionally considered one of the safest investment options, delivered an average return of about 7 percent annually. Under this scenario, an initial investment of Rs. 10 lakh could grow to roughly Rs. 19.7 lakh in nominal terms after ten years. However, once inflation is accounted for, the real value rises only to about Rs. 11.3 lakh, reflecting a modest gain of approximately 13 percent in real purchasing power.

By contrast, investments in the stock market show significantly stronger wealth creation potential. With an average annual return estimated at around 12 percent, a Rs. 10 lakh investment could grow to approximately Rs. 31 lakh over a decade. When adjusted for inflation, the real value remains around Rs. 17.8 lakh, representing a substantial increase in purchasing power. In cases where market performance reaches higher levels, returns could potentially be even stronger, demonstrating the long-term power of equity investments.

Another asset that has historically delivered strong returns is gold, which in this comparison generated an estimated annual return of around 15 percent. Over ten years, this could turn an initial Rs. 10 lakh into roughly Rs. 40 lakh in nominal value. After adjusting for inflation, the real value stands at approximately Rs. 23 lakh, making gold one of the most effective traditional assets for preserving and increasing wealth during periods of economic uncertainty.

Similarly, real estate has shown consistent long-term growth. With an estimated return of around 12 percent annually, property investments have the potential to grow at a pace comparable to equities over extended periods. A Rs. 10 lakh investment in real estate could also rise to about Rs. 31 lakh in nominal value, translating into a real purchasing value close to Rs. 17.8 lakh after inflation adjustments.

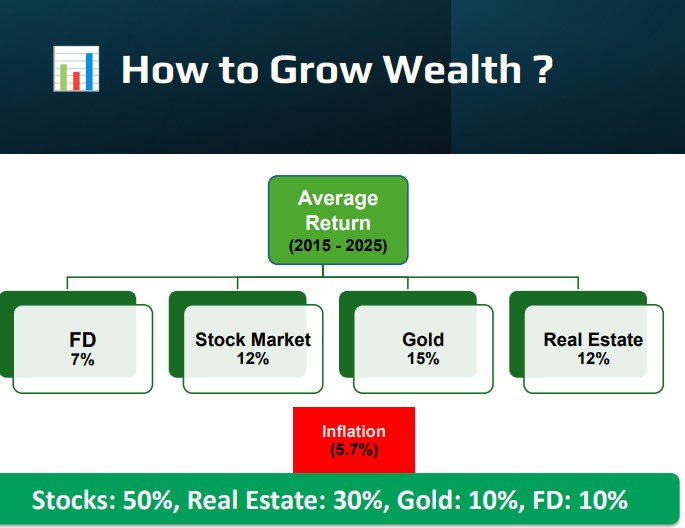

Financial planners emphasize that the key to wealth creation lies not only in choosing the right asset but also in diversification and strategic allocation. A balanced investment strategy might include a portfolio distribution such as 50 percent in stocks, 30 percent in real estate, 10 percent in gold, and 10 percent in fixed deposits. Such a structure allows investors to benefit from growth opportunities while maintaining stability during market fluctuations.

Beyond financial instruments, the framework presented in the analysis highlights an often-overlooked aspect of investing: the psychological and strategic dimension of decision-making. According to this perspective, the investment process can be understood through three stages — “Why, How, and What.” The “Why” represents mindset and emotional discipline, accounting for roughly 80 percent of investment success, while the “How” involves planning and strategy, and the “What” relates to execution, such as selecting specific assets or trade opportunities.

Experts argue that investors frequently focus too heavily on technical tools, charts, and short-term market signals while neglecting the fundamental purpose behind their financial decisions. A clear investment objective, disciplined strategy, and long-term perspective are often more important than short-term market timing.

Ultimately, the data reinforces a powerful lesson for individual investors: inflation steadily erodes idle savings, while productive assets create wealth over time.

Whether through equities, real estate, gold, or diversified portfolios, the act of investing remains the most effective defense against the gradual loss of purchasing power. In the long run, the difference between saving and investing can determine whether money simply survives inflation—or grows to generate real prosperity.

Advertisement

Written by

Dipesh Ghimire