Popular News

Hot

Stock

Top

dipesh

Trading

Interest Rate Adjustment Analysis of Commercial Banks in Nepal for Mangsir 2081

Interest Rate Adjustment Analysis of Commercial Banks in Nepal for Mangsir 2081 Interest rates play a pivotal role in the financial ecosystem, impacting how people save, invest, and borrow. In Nepal, as in other countries, these rates reflect the broader economic climate and the strategic goals of banks. Recently, commercial banks in Nepal announced adjustments to their deposit interest rates for Mangsir 2081. This article explores these adjustments in detail, analyzing their implications for individuals, institutions, and the economy as a whole. The focus of this analysis is to understand why banks have made these changes, what they might signal about the financial outlook in Nepal, and how different stakeholders—depositors, borrowers, policymakers—may need to adapt. In a country where the banking sector significantly impacts the economy, these shifts in interest rates can have widespread effects.

Dipesh Ghimire

6 min read

Interest rates play a pivotal role in the financial ecosystem, impacting how people save, invest, and borrow. In Nepal, as in other countries, these rates reflect the broader economic climate and the strategic goals of banks. Recently, commercial banks in Nepal announced adjustments to their deposit interest rates for Mangsir 2081. This article explores these adjustments in detail, analyzing their implications for individuals, institutions, and the economy as a whole.

The focus of this analysis is to understand why banks have made these changes, what they might signal about the financial outlook in Nepal, and how different stakeholders—depositors, borrowers, policymakers—may need to adapt. In a country where the banking sector significantly impacts the economy, these shifts in interest rates can have widespread effects.

Overview of Interest Rate Trends in Nepali Banking

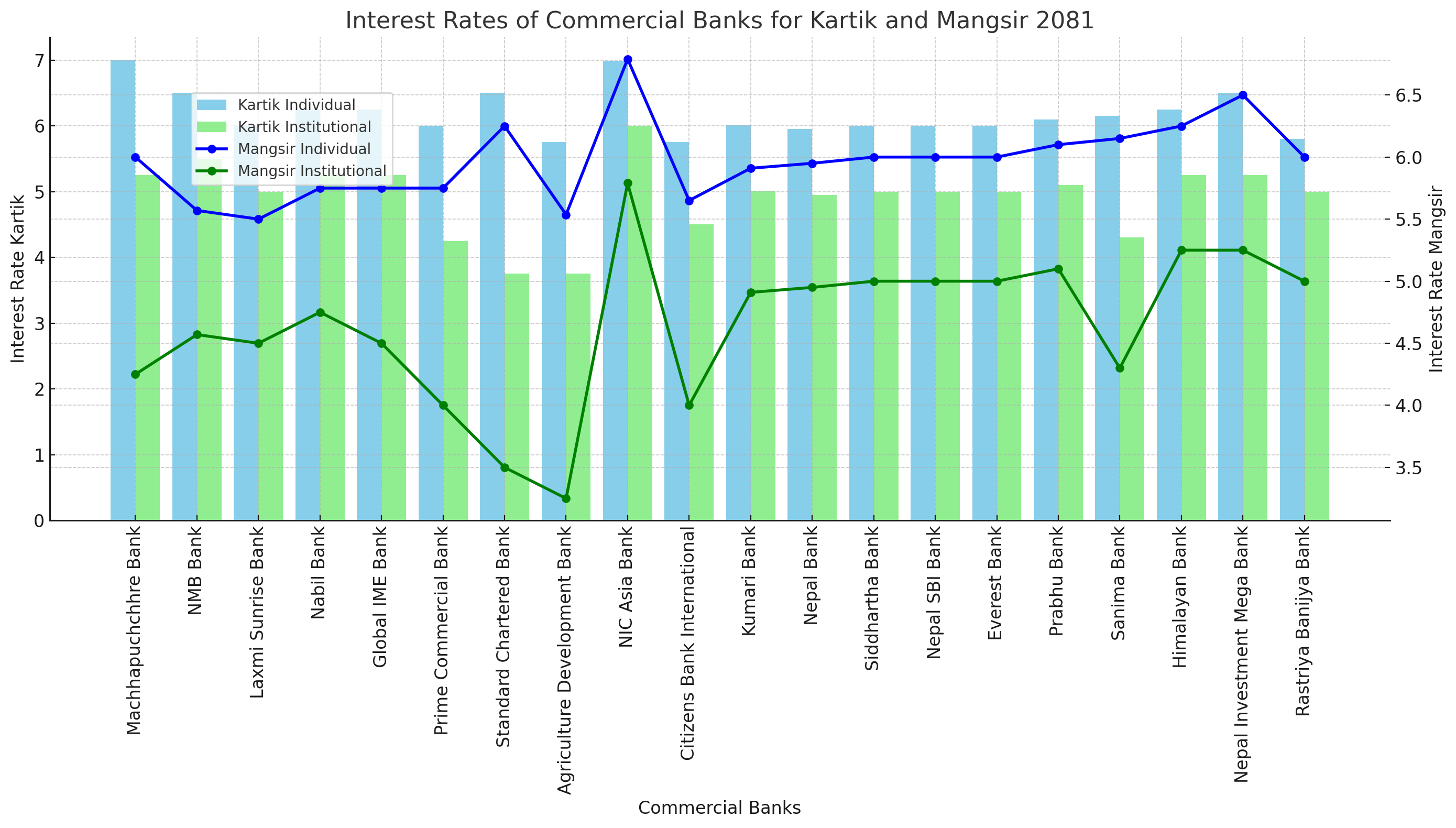

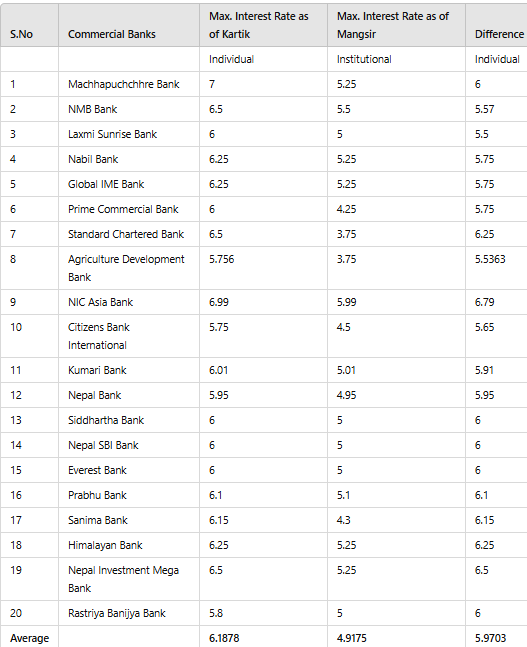

Interest rates in Nepal have experienced various shifts over the years, influenced by economic cycles, inflationary pressures, and global financial trends. In recent years, Nepal Rastra Bank (NRB), the central bank, has been managing rates with the aim of fostering growth while controlling inflation and ensuring financial stability. Compared to countries like India or Bangladesh, Nepal’s interest rates have generally been higher, reflecting both the need to attract depositors and the limited investment opportunities in other sectors.

For Kartik 2081, average interest rates across commercial banks stood at approximately 6.18% for individual deposits and 4.92% for institutional deposits. However, in Mangsir 2081, we observed a slight reduction to around 5.97% for individual deposits and 4.64% for institutional deposits. This subtle but consistent downward adjustment suggests a cautious approach by banks, potentially in response to anticipated economic slowdowns or liquidity management needs.

Detailed Bank-by-Bank Analysis

Each bank’s strategy in setting interest rates reflects its priorities, financial strength, and market positioning. Some banks have aggressively cut rates, while others have kept them stable. Let’s look at a few notable cases:

Machhapuchchhre Bank: Reduced its individual deposit rate by 1%, bringing it down to 6%. This sharp decrease suggests a conservative approach, possibly aimed at managing liquidity more tightly.

NIC Asia Bank: With an individual rate of 6.79% for Mangsir, NIC Asia is among the few banks still offering relatively high returns, albeit lower than the previous month’s rate. This may be part of a strategy to retain a competitive edge and attract a large depositor base.

Nepal Bank and Siddhartha Bank: These banks opted to keep their rates unchanged, signaling stability and confidence in their current position. This approach might appeal to risk-averse depositors seeking consistent returns.

Citizens Bank International: Reduced its institutional deposit rate by 0.5%, aligning with sector-wide trends but at a level that keeps it competitive for institutional clients.

Overall, the diversity in rate adjustments across banks reflects varied strategies, influenced by each bank’s financial goals and market dynamics. Some banks prioritize attracting individual depositors, while others focus on institutional deposits, adjusting rates to achieve a balanced portfolio.

Economic and Market Implications

The interest rate adjustments carry significant implications for both investors and borrowers in Nepal:

Impact on Individual Depositors: Lower rates on savings accounts may push individuals to seek alternative investments, potentially driving more capital into Nepal’s stock market, real estate, or other higher-yield options. This trend could stimulate growth in these sectors but may also heighten risks if investors are unprepared for the volatility associated with these investments.

Institutional Investors’ Response: Large institutions often require stable and substantial returns on their deposits. The rate reductions might lead them to reassess their cash management strategies, possibly reallocating capital to foreign investments or diversifying into more aggressive domestic assets.

Loan Accessibility: As deposit rates fall, banks may lower their lending rates as well, making loans more affordable. This could boost demand for credit, particularly in sectors like real estate, construction, and SMEs. Lower borrowing costs can spur economic activity, but if loan standards are relaxed excessively, it could increase the risk of defaults.

Broader Economic Impact: The lower rates may signal a cautious stance from banks as they anticipate changes in liquidity or respond to NRB’s policy shifts. If the trend continues, we may see a broader shift in savings and investment behaviors across Nepal, potentially impacting sectors reliant on deposits for funding.

Regional and Global Influences

Interest rate policies in Nepal do not exist in isolation; they are influenced by regional and global economic conditions. For instance, the U.S. Federal Reserve’s recent interest rate hikes have led to shifts in global capital flows, putting pressure on emerging markets like Nepal to manage liquidity carefully. Comparatively, other South Asian countries have also adjusted their rates to stabilize their economies amidst inflationary pressures and currency fluctuations.

Nepal’s reliance on foreign aid and external debt introduces additional complexities. As interest rates on foreign loans fluctuate, Nepal must balance domestic and international liabilities, often adjusting domestic rates to mitigate potential risks. These dynamics underscore the interconnected nature of Nepal’s financial policies with global economic trends.

Historical Case Studies

Examining past instances of interest rate adjustments can provide insights into the potential outcomes of the current trend. During the global financial crisis of 2008, Nepal, like many other countries, maintained higher interest rates to attract deposits and maintain liquidity. More recently, inflationary periods have led to rate hikes to control consumer prices.

Comparing with similar economies, we find that countries like Sri Lanka and Bhutan have experienced similar cycles of rate adjustments in response to external shocks and internal economic conditions. These historical examples suggest that while rate cuts can stimulate borrowing and spending, they also carry risks if not managed prudently.

Future Outlook and Projections

Looking ahead, it’s likely that Nepali banks will continue to adjust rates cautiously, particularly if inflation remains stable or declines. For the upcoming quarters, the following scenarios are plausible:

Stable or Further Reduced Rates: If inflation stabilizes and NRB’s policies remain accommodative, banks may lower rates further to encourage credit growth.

Potential Rate Hikes: In the event of a liquidity crunch or rising inflation, banks might raise rates to attract deposits and retain capital.

Risks: Any drastic changes in interest rates could disrupt depositor confidence or increase the risk of default on loans issued at lower rates. Policymakers and banks will need to carefully monitor these dynamics to ensure financial stability.

Implications for Policymakers and Financial Regulators

The Nepal Rastra Bank (NRB) plays a critical role in guiding the banking sector. Given the current rate environment, NRB may focus on ensuring a balanced approach that supports economic growth while controlling inflation. Policy recommendations include maintaining transparency in rate-setting, monitoring credit quality, and providing guidance on responsible lending practices to prevent excessive risk-taking.

In addition, NRB could encourage banks to develop financial products that cater to a diverse range of investor needs, promoting long-term financial inclusion and stability.

Investor Education: Navigating the Changing Interest Rate Environment

For individual and institutional investors, navigating this changing environment requires informed strategies:

Individual Investors: With deposit rates falling, individuals might consider diversifying into alternative investment vehicles such as mutual funds, government bonds, or even stocks, provided they understand the risks.

Institutional Investors: Larger institutions may look for higher-yield investments, possibly in the form of corporate bonds, real estate, or other fixed-income securities. Diversifying portfolios to reduce dependency on bank deposits can be a prudent strategy.

Education on these alternatives can help investors make informed decisions, mitigating the impact of lower interest rates on their overall returns.

Conclusion

The recent interest rate adjustments by Nepali banks represent a cautious but necessary response to the current economic environment. By slightly lowering rates, banks aim to balance depositor returns with the need for economic growth and loan accessibility. This trend has significant implications for individual and institutional investors, as well as for the economy as a whole.

As the Nepali economy adapts to these changes, policymakers and banks must work together to promote financial stability, foster growth, and provide opportunities for diversified investments. Looking forward, continued monitoring of economic indicators and regulatory guidance will be crucial to navigating the challenges and opportunities posed by this new interest rate environment.

Advertisement

Written by

Dipesh Ghimire