NEPSE

Investor Backlash After SEBON’s Call for Suggestions: Deep Structural Reform Demands Emerge

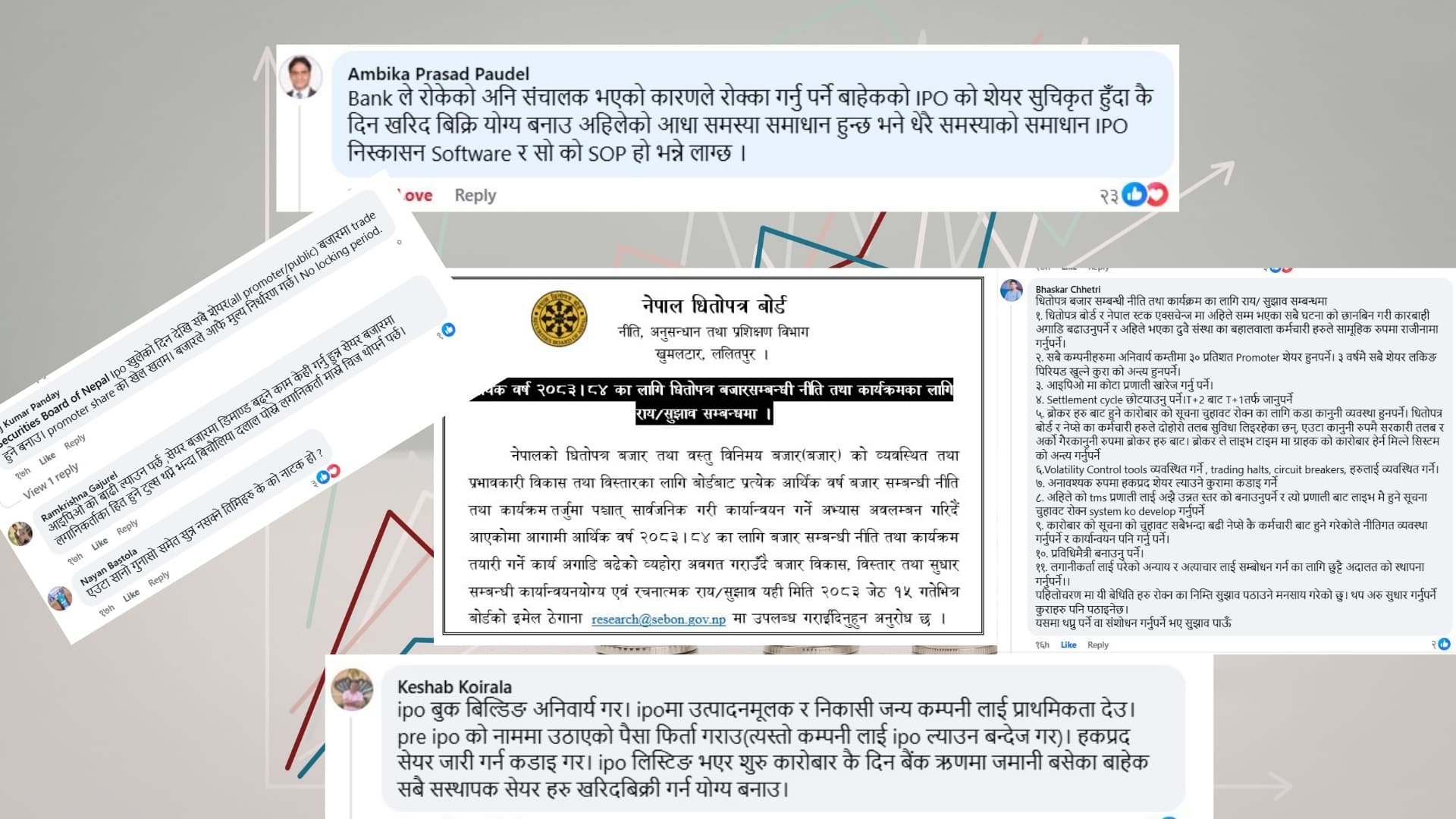

Investor Backlash After SEBON’s Call for Suggestions: Deep Structural Reform Demands Emerge Nepal’s Securities Board (SEBON) invited public suggestions for the upcoming fiscal year’s capital market policies, but the response from investors has gone far beyond routine feedback. Comments on the board’s official social media platform reveal not only dissatisfaction with the current system but also a clear and detailed roadmap for reform. The intensity and consistency of these responses suggest that investor frustration has reached a critical point, with demands centered on transparency, efficiency, and structural fairness.

Dipesh Ghimire

3 min read

Nepal’s Securities Board (SEBON) invited public suggestions for the upcoming fiscal year’s capital market policies, but the response from investors has gone far beyond routine feedback. Comments on the board’s official social media platform reveal not only dissatisfaction with the current system but also a clear and detailed roadmap for reform. The intensity and consistency of these responses suggest that investor frustration has reached a critical point, with demands centered on transparency, efficiency, and structural fairness.

Investor Ambika Prasad Paudel highlighted fundamental flaws in the IPO system. He argued that, except for legally restricted shares, all IPO shares should be tradable from the very first day of listing. According to him, this single reform could resolve a large portion of market distortions. Paudel also pointed to weaknesses in IPO issuance software and the absence of clear standard operating procedures, suggesting that operational inefficiencies are deeply embedded in the system.

Focusing on day-to-day trading challenges, Arjun Dahal raised concerns that reflect the lived experience of retail investors. He emphasized delays in receiving payments after selling shares and called for the immediate elimination of illegal credit-based trading. Dahal also proposed insurance protection for funds held in broker accounts, along with improved investor education at the account opening stage. His broader suggestions—such as enabling intraday trading, automating the EDIS system, ensuring proper dividend tracking, and introducing digital voting for shareholders—indicate a push toward a more modern and investor-friendly trading environment.

Taking a more radical stance, Raj Kumar Panday challenged the very structure of share ownership in Nepal’s capital market. He proposed that all shares, including promoter holdings, should be freely tradable from the IPO stage, effectively eliminating lock-in periods. His argument reflects a belief that market-driven price discovery should replace regulatory restrictions, although such a shift would significantly alter the current balance between stability and liquidity.

Among the most comprehensive responses came from Bhaskar Chhetri, who called for sweeping institutional reforms. He demanded investigations into past irregularities within SEBON and the Nepal Stock Exchange (NEPSE), along with accountability measures for those involved. Chhetri also advocated for shortening the settlement cycle from T+2 to T+1, abolishing the IPO quota system, and strengthening legal frameworks to prevent information leakage and insider trading. His comments suggest that the credibility of regulatory institutions themselves is under scrutiny.

Chhetri further raised concerns about systemic weaknesses in technology and governance. He argued that the current Trading Management System (TMS) requires significant upgrades to prevent misuse and improve security. He also called for better management of volatility control tools, stricter regulation of rights share issuance, and even the establishment of a specialized court to address investor grievances. These proposals point to a deeper demand for institutional restructuring rather than incremental change.

From a different perspective, Keshab Koirala focused on improving the quality of companies entering the market. He advocated for mandatory book-building mechanisms and prioritizing productive and export-oriented firms in IPO approvals. Koirala also criticized the misuse of pre-IPO funding practices and called for stricter controls to ensure that only financially credible companies are allowed to raise public capital.

Investor Ramkrishna Gajurel brought attention to perceived inequities in market participation. He argued that IPO gains are often captured by intermediaries and limited groups rather than genuine investors, suggesting that the system disproportionately benefits insiders. This perception of unfairness, he implied, discourages broader participation and weakens trust in the market.

Similarly, Nayan Bastola pointed to structural bias within the regulatory framework, claiming that influential players are often protected while smaller investors bear the risks. Such sentiments highlight a growing perception gap between regulators and retail participants, which could have long-term implications for market confidence.

On the regulatory front, Hari Prasad Pandit emphasized the need to curb price manipulation in premium IPOs and eliminate illegal trading practices. He also called for full automation of systems like EDIS and improvements in cost calculation mechanisms. His insistence on strict action against insider trading reflects a broader demand for stronger enforcement rather than just policy reform.

Taken together, these responses reveal a clear pattern: investors are not merely seeking minor adjustments but are calling for a fundamental overhaul of Nepal’s capital market structure. Issues related to IPO allocation, broker practices, technological infrastructure, and regulatory accountability are deeply interconnected, and addressing them will require a coordinated and long-term approach.

SEBON’s initiative to gather suggestions has, perhaps unintentionally, exposed the depth of systemic challenges facing the market. While the diversity of opinions reflects different priorities, the underlying message is consistent—investors want a transparent, efficient, and fair system that protects their interests. How effectively these concerns are translated into policy will determine not only the success of upcoming reforms but also the future credibility of Nepal’s capital market.

Advertisement

Written by

Dipesh Ghimire