stock Loans

NRB Allows Up to 80 Percent Loans Against Shares of Financially Strong Companies

Overall, the decision appears intended to balance market support with financial-sector stability. It gives investors greater borrowing capacity against high-quality shares while retaining safeguards against repeated revaluation, excessive leverage and indiscriminate lending.

Dipesh Ghimire

4 min read

Kathmandu — Nepal Rastra Bank has introduced a more flexible lending arrangement for loans backed by shares, allowing banks and financial institutions to extend credit of up to 80 percent of the assessed value of shares belonging to financially strong listed companies.

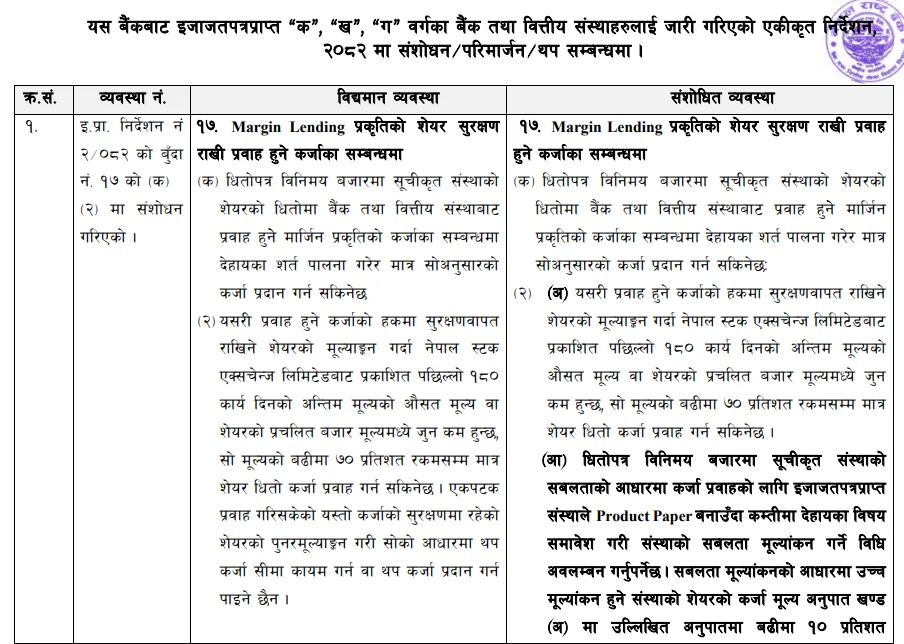

The new provision has been introduced through an amendment to the Unified Directives, 2082, issued to banks and financial institutions. Under the earlier arrangement, lenders could provide share-backed loans of up to 70 percent of the lower value between the prevailing market price and the average trading price of the shares over the last 180 working days.

The central bank has retained the existing 70 percent general limit but has allowed banks and financial institutions to provide an additional 10 percentage points in financing against shares of companies that demonstrate strong financial performance, regulatory discipline and institutional credibility.

This means that the higher 80 percent lending facility will not be available against the shares of every company listed on the Nepal Stock Exchange. Banks will first have to assess the financial strength and overall reliability of each company before deciding whether its shares qualify for the additional loan margin.

For this purpose, banks and financial institutions will be required to develop their own “product paper.” The document will establish the criteria and scoring system used to classify listed companies according to their financial and institutional strength.

The evaluation must take into account several indicators, including the size of the company’s paid-up capital, the period for which it has remained listed on the stock exchange, its history of profitability and dividend distribution, credit rating, compliance with regulatory requirements and regular completion of annual general meetings.

Companies receiving higher scores under these criteria may qualify for the enhanced lending facility. Investors pledging shares of such companies as collateral could receive loans equal to a maximum of 80 percent of the eligible share value.

The requirement to prepare a company-specific assessment is likely to change the earlier practice of treating most listed shares in a broadly similar manner. Under the revised approach, shares of companies with stable earnings, good governance and a consistent dividend record will be considered lower-risk collateral than shares of companies with weak financial performance or poor regulatory compliance.

Banks and financial institutions will also have to publish their product papers on their official websites. This provision is expected to improve transparency by allowing investors to understand which companies qualify for higher loan limits and the standards used by individual lenders in making such decisions.

However, the revised policy also gives banks considerable responsibility. Since each financial institution will prepare its own product paper, the list of companies qualifying for the 80 percent facility may differ from one bank to another. A company considered financially strong by one institution may not necessarily receive the same classification from another.

The provision could therefore lead banks to compete not only through interest rates but also through their selection and evaluation of eligible companies. At the same time, the central bank’s mandatory criteria are expected to prevent institutions from preparing completely arbitrary assessments.

Nepal Rastra Bank has clarified that banks cannot increase the loan amount later merely by revaluing the pledged shares. Once a loan has been sanctioned on the basis of the initial valuation and approved lending ratio, the limit cannot be raised through a subsequent increase in the market price of the shares or a fresh assessment of the company.

This restriction is important because share prices can rise sharply during bullish market conditions. Allowing repeated revaluation could encourage excessive borrowing and expose both investors and banks to greater losses if the market later declines.

The revised provision is expected to benefit investors holding shares of fundamentally strong companies. With a higher lending ratio, such investors may gain access to additional liquidity without immediately selling their holdings.

For example, under the previous 70 percent ceiling, eligible shares valued at Rs 1 million could support a maximum loan of Rs 700,000. Under the new arrangement, the same collateral could support a loan of up to Rs 800,000, provided the company meets the bank’s financial-strength criteria.

The policy may also increase demand for shares of companies with strong balance sheets, regular profits, a stable dividend history and sound corporate governance. Investors could begin to attach greater importance to whether a company’s shares qualify for the higher loan facility.

However, the provision does not eliminate the risks associated with share-backed lending. A higher loan-to-value ratio leaves a smaller cushion between the loan amount and the value of the collateral. If share prices decline significantly, borrowers may face margin calls or be required to provide additional collateral.

Banks will therefore need to apply careful risk assessment even when lending against shares of financially sound companies. Strong company fundamentals may reduce the risk of poor business performance, but they cannot fully protect investors from fluctuations in the secondary market.

The policy represents a shift towards risk-based lending in Nepal’s capital market. Rather than applying the same loan ceiling to all listed shares, the central bank has allowed stronger companies to receive preferential treatment based on measurable financial and governance indicators.

The revised arrangement could support investor confidence and improve liquidity in the share market, particularly if banks implement the policy consistently and transparently. Its actual impact, however, will depend on the quality of the product papers, the strictness of company evaluations and the willingness of banks to provide the additional lending facility.

Overall, the decision appears intended to balance market support with financial-sector stability. It gives investors greater borrowing capacity against high-quality shares while retaining safeguards against repeated revaluation, excessive leverage and indiscriminate lending.

Advertisement

Written by

Dipesh Ghimire