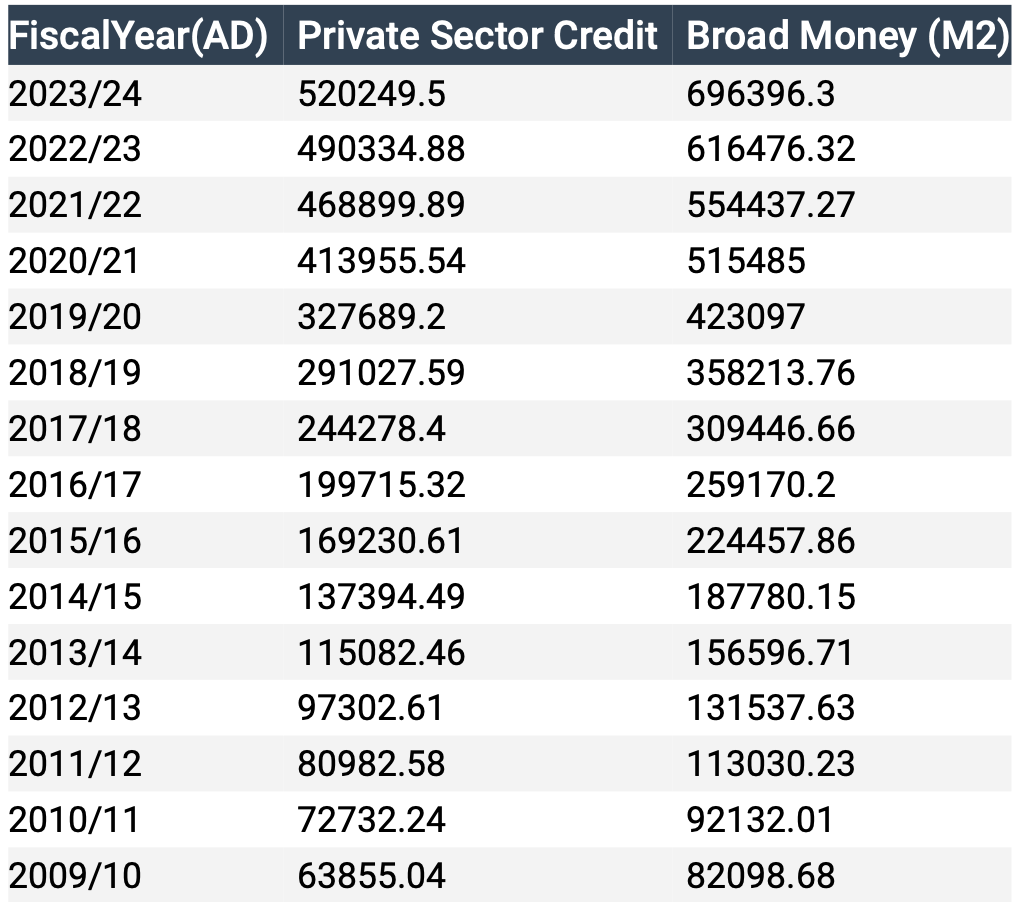

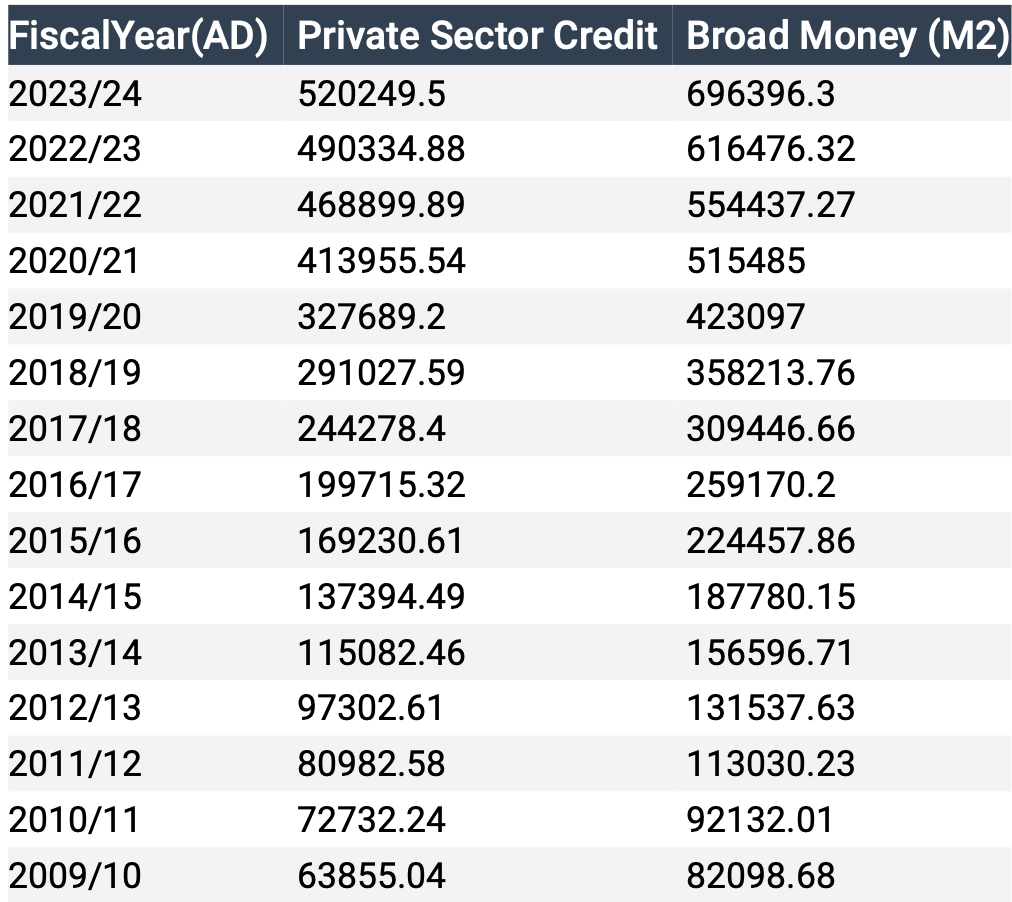

काठमाडौं, नेपाल – नेपालमा निजी क्षेत्रको कर्जा वृद्धिदर आर्थिक वर्ष २०२३/२४ मा ५.७५% मा सीमित भएको छ। हालसालै सार्वजनिक तथ्याङ्क अनुसार, निजी क्षेत्रको कर्जा ५.२ ट्रिलियन रुपैयाँ (५,२०,२४९.५ करोड) पुगेको छ। तर, यो वृद्धि अघिल्लो वर्ष २०२२/२३ को ४.३७% को तुलनामा केही सुधार भए पनि अघिल्लो वर्षहरूको तुलनामा निकै कम छ।

तीन वर्षअघिको २०२०/२१ मा निजी क्षेत्रको कर्जा वृद्धिदर २०.८४% थियो, जुन हालको वृद्धिदरको तुलनामा निकै उच्च थियो। तर, पछिल्ला केही वर्षयता कर्जा प्रवाहमा गिरावट आउनु बैंक तथा वित्तीय संस्थाहरूको सावधानीपूर्ण कर्जा नीतिहरू र आर्थिक मन्दीका संकेतहरू देखिन्छन्।

कर्जा वृद्धिदरको घट्दो प्रवृत्ति

विगत केही वर्षयता नेपालमा निजी क्षेत्रको कर्जा वृद्धिदर क्रमशः घट्दै गएको देखिन्कर्जा प्रवाह सुस्त हुनुका मुख्य कारणहरू

१. बढ्दो ब्याजदर: नेपाल राष्ट्र बैंक (NRB) ले मुद्रास्फीति नियन्त्रण गर्न कडाइ गरेको छ, जसले बैंकहरूको ऋणको लागत बढाएको छ।

२. तरलता अभाव: बैंक तथा वित्तीय संस्थाहरूमा तरलता (liquidity) को समस्या देखिएको छ, जसले नयाँ कर्जा प्रवाहमा असर परेको छ।

३. व्यवसायिक विश्वासको कमी: सेयर बजारमा अनिश्चितता, जग्गा तथा निर्माण क्षेत्रमा मन्दी, तथा व्यापारमा कमजोर गतिविधि देखिएको छ।

४. लगानीको अभाव: निर्माण, जलविद्युत्, उत्पादन तथा पर्यटन क्षेत्रमा लगानी आकर्षित हुन कठिन भइरहेको छ।

५. बैंकिङ नियमन कडाइ: नेपाल राष्ट्र बैंकले लगानी सुरक्षाका लागि नयाँ नीतिहरू ल्याएको छ, जसले बैंकहरूलाई ऋण प्रवाहमा सतर्क बनाएको छ।

निजी क्षेत्रको कर्जा प्रवाह घट्दा हुने असरहरू

व्यवसायहरूमा लगानी कम हुने: बैंक कर्जामा निर्भर व्यवसायहरूलाई विस्तार गर्न कठिनाइ हुन्छ।

रोजगारी सिर्जनामा गिरावट: जब उद्योग तथा व्यवसायले ऋण पाउँदैनन्, रोजगारीको अवसरहरू सीमित हुन्छन्।

जिडीपी वृद्धिमा असर: आर्थिक वृद्धिका लागि बैंकिङ प्रणालीबाट प्रवाहित कर्जा महत्त्वपूर्ण हुन्छ।

विशेषज्ञहरूका अनुसार, यदि तरलता समस्या कायमै रह्यो भने नेपालमा निजी क्षेत्रको कर्जा प्रवाह आगामी वर्षहरूमा अझै सुस्त रहन सक्छ।

नेपाल राष्ट्र बैंकको रणनीति र सम्भावित उपायहरू

नेपाल राष्ट्र बैंकले मुद्रास्फीति नियन्त्रण र वित्तीय स्थायित्व कायम राख्न विभिन्न उपायहरू अवलम्बन गरिरहेको छ। तर, कर्जा प्रवाह सुधार गर्न निम्न उपायहरू आवश्यक हुन सक्छन्:

ब्याजदर घटाउने: कर्जा लिने खर्च घटाउन ब्याजदर समायोजन गर्नुपर्ने आवश्यकता छ।

तरलता व्यवस्थापन: बैंकहरूलाई कर्जा प्रवाह सहज बनाउन नेपाल राष्ट्र बैंकले विशेष नीतिहरू ल्याउन सक्छ।

कर्जा प्रोत्साहन कार्यक्रम: निर्माण, जलविद्युत्, तथा लघु उद्यमका लागि विशेष कर्जा प्याकेजहरू ल्याउन सकिन्छ।

भविष्यको सम्भावना: के नेपालको कर्जा प्रवाह पुनः वृद्धि हुन सक्छ?

नेपालको आर्थिक भविष्य वैश्विक अर्थतन्त्र, बैंकिङ प्रणालीको नीति तथा सरकारको वित्तीय निर्णयहरूमा निर्भर रहनेछ।

यदि कर्जा प्रवाह सुधार गर्न प्रभावकारी उपायहरू अपनाइएन भने निजी क्षेत्रको विस्तार र आर्थिक वृद्धिमा थप चुनौती आउन सक्छ। तर, सही नीतिहरू लागू भएमा बैंकहरूको तरलता सुधार हुन सक्छ, जसले पुनः आर्थिक गतिविधिलाई गति दिन मद्दत गर्नेछ।

अहिलेसम्म बैंकहरू तथा व्यवसायहरू आर्थिक परिवर्तहरू हेर्दै सावधानीपूर्वक अघि बढिरहेका छन्। नेपाल राष्ट्र बैंक, सरकार, र निजी क्षेत्रको सहकार्य आवश्यक छ, जसले दीर्घकालीन रूपमा कर्जा प्रवाहलाई सन्तुलित बनाउन सक्छ।