नेपालका प्रमुख वाणिज्य बैंकहरूले जेष्ठ महिनाको अन्त्यसम्ममा लिएको ऋणको विवरणले बैंकहरू अझैपनि कर्जा तथा वित्त व्यवस्थापनका लागि बाह्य स्रोतहरूमा निर्भर रहेको देखाएको छ। यस अवधिमा लिएको ऋण विभिन्न स्रोतबाट जस्तै अन्तरबैंक कर्जा, विदेशी वित्तीय संस्था, अन्य वित्तीय संस्था तथा बन्ड र सेक्युरिटीमार्फत गरिएको पाइन्छ।

मुख्य बुँदाहरू:

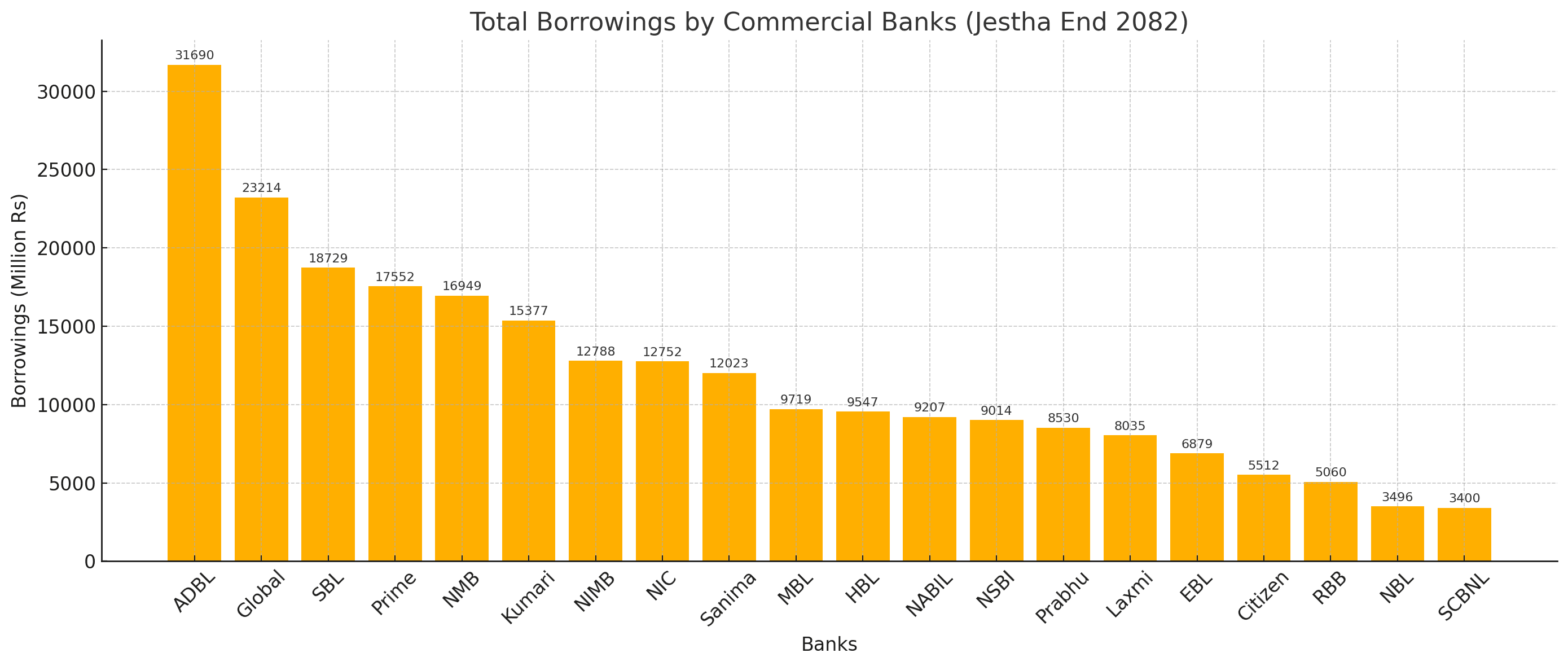

जेष्ठ २०८२ को अन्त्यसम्ममा सबैभन्दा बढी ऋण लिने बैंक कृषि विकास बैंक (ADBL) हो, जसले कूल रु. ३१.६९ अर्ब बराबरको ऋण लिएको छ। यसपछिका बैंकहरूमा ग्लोबल आइएमई बैंकले रु. २३.२१ अर्ब, र प्राइम कमर्शियल बैंकले रु. १७.५५ अर्ब बराबरको ऋण लिएका छन्। अन्य बैंकहरू जस्तै एनएमबी (रु. १६.९५ अर्ब), सानिमा (रु. १२.०२ अर्ब), र प्रभु बैंक (रु. ८.५२ अर्ब) पनि उच्च ऋणकर्ताको सूचीमा छन्।

बन्ड र सेक्युरिटीको प्रमुखता:

अधिकांश बैंकहरूले बन्ड तथा सेक्युरिटी जारी गरेर ऋण लिएका छन्। कुमारी बैंक (रु. १४ अर्ब), एनआईसी एशिया (रु. १२.७५ अर्ब), र नबिल बैंक (रु. ९.२१ अर्ब) यसमा अगाडि छन्। कृषि विकास बैंक (ADBL) ले मात्र रु. २०.४८ अर्ब बराबरको बन्ड जारी गरेको देखिन्छ।

विभिन्न स्रोतबाट ऋण:

राष्ट्र बैंक (NRB) बाट कर्जा: न्यून देखिन्छ, केवल सिभिल बैंक (SBL) ले रु. ३९१.९२ मिलियन र सिटिजेन बैंकले रु. ४१.४४ मिलियन लिएका छन्।

अन्तरबैंक कर्जा (Interbank Borrowing): स्ट्यान्डर्ड चार्टर्ड (Rs. 1 अर्ब), एचबीएल (Rs. 1.5 अर्ब), एमबीएल (Rs. 2.4 अर्ब), र प्राइम बैंक (Rs. 5.5 अर्ब) सक्रिय छन्।

विदेशी वित्तीय संस्था: एनएमबी (Rs. 5.03 अर्ब), ADBL (Rs. 12.17 अर्ब), र सिभिल बैंक (Rs. 5.77 अर्ब) अगाडि छन्।

अन्य वित्तीय संस्था: ADBL ले रु. १०.३९ अर्ब र एनएसबीआईले रु. ३.१६ अर्ब बराबर ऋण लिएका छन्।

यस विवरणले देखाउँछ कि नेपाली बैंकहरूले अझैपनि ऋण विस्तार र तरलता व्यवस्थापनका लागि कर्जा लिने रणनीतिमा केन्द्रित छन्। बन्डमार्फत दीर्घकालीन पूँजी संकलन भइरहेको छ, जुन सकारात्मक मानिन्छ। तथापि, विदेशी कर्जा स्रोतमा अत्यधिक निर्भर बैंकहरूले अन्तर्राष्ट्रिय ब्याजदरको जोखिम व्यवस्थापनमा सतर्कता अपनाउनु पर्ने आवश्यकता देखिन्छ।

जेष्ठ २०८२ को अन्त्यसम्मको यो वित्तीय स्थिति नेपाली बैंकिङ्ग प्रणालीले बजारमा लगानी विस्तारका लागि आन्तरिक र बाह्य स्रोतहरू प्रयोग गरिरहेको स्पष्ट संकेत हो।