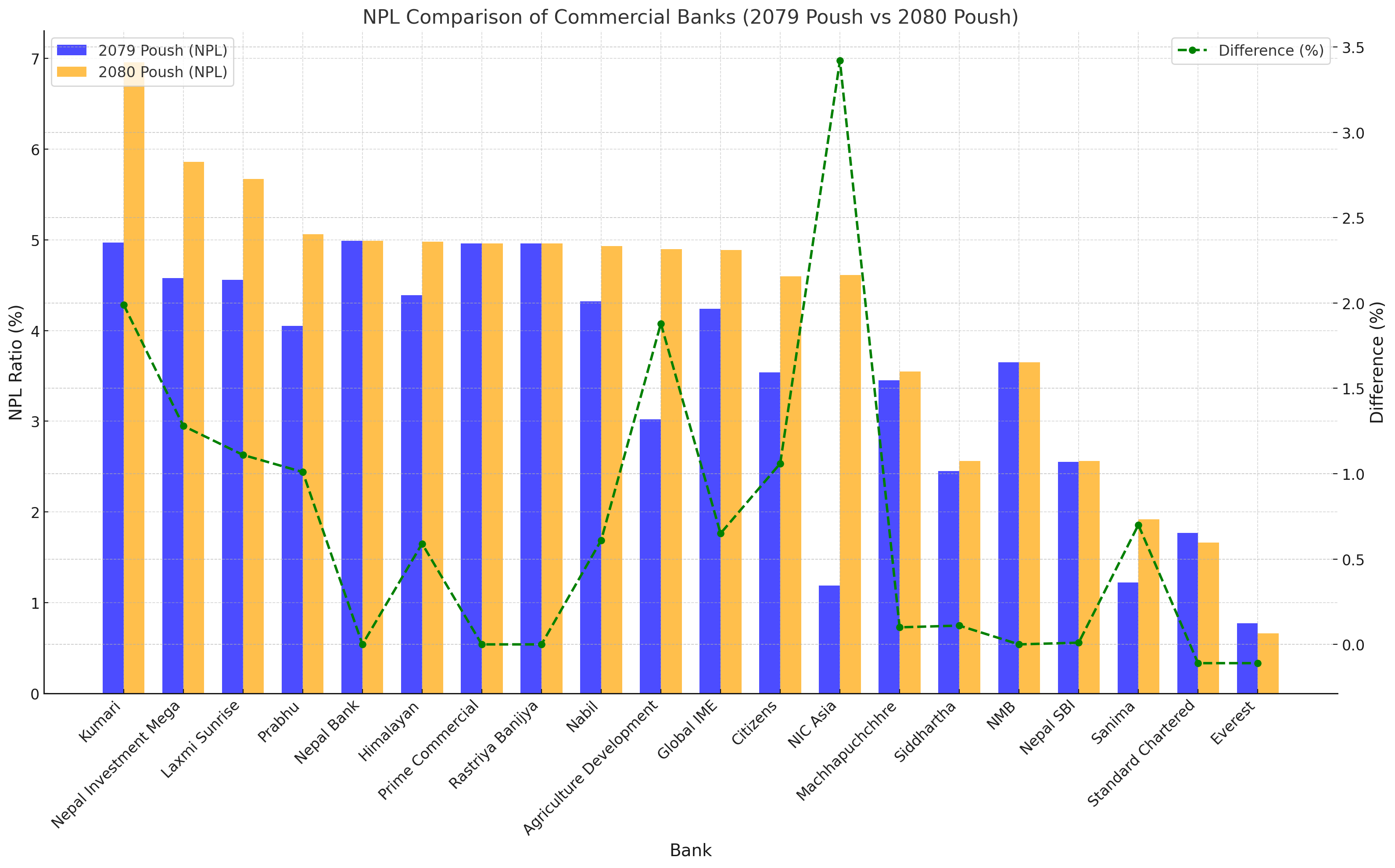

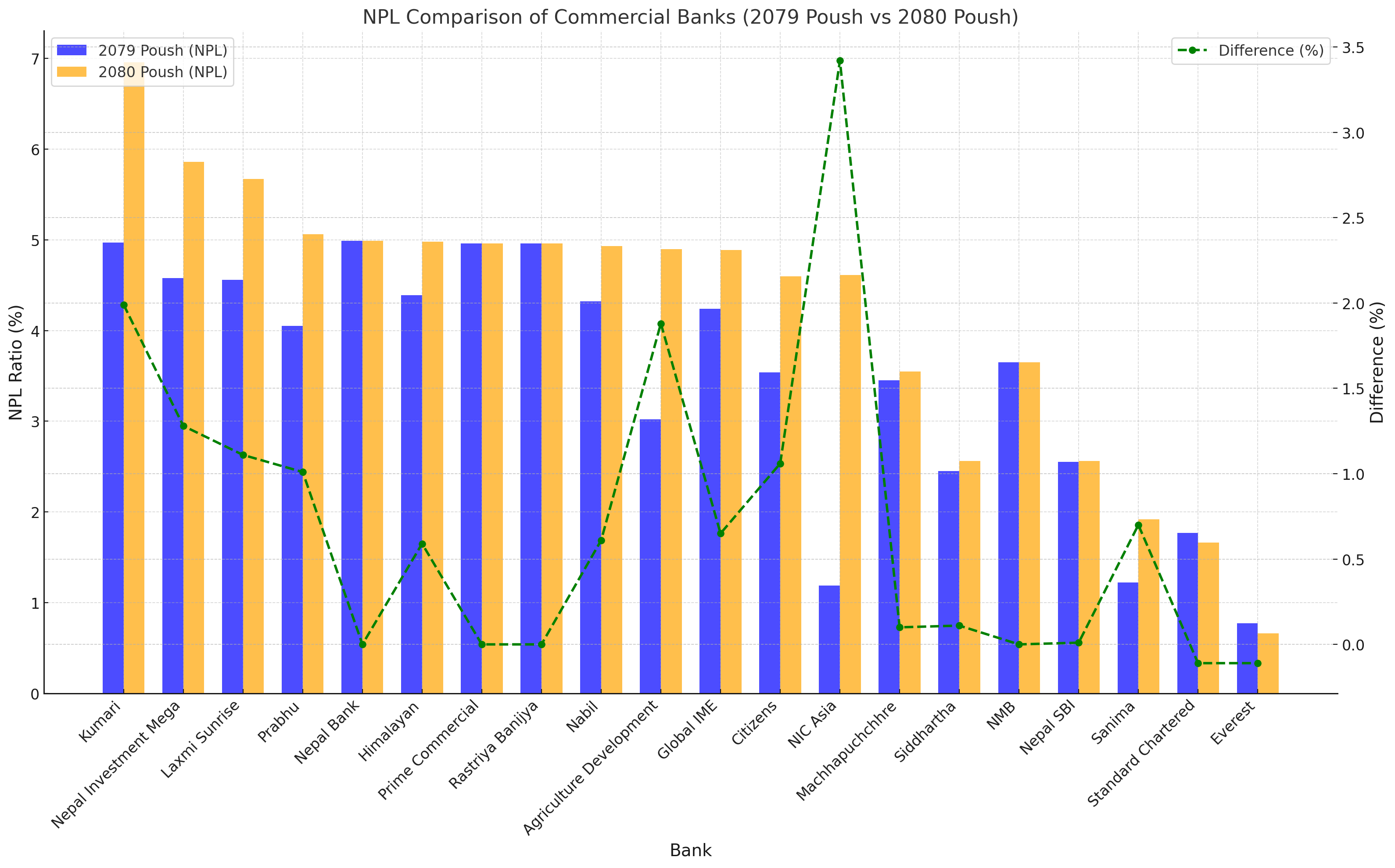

वाणिज्य बैंकहरूले आर्थिक वर्ष २०८० को पुस मसान्तसम्मको खराब कर्जा (एनपीएल) अनुपात सार्वजनिक गरेका छन्। तथ्यांकले देखाउँछ कि औसत खराब कर्जा अनुपात ३.४० प्रतिशतबाट बढेर ४.४९ प्रतिशत पुगेको छ, जुन १.०९ प्रतिशत बिन्दुले वृद्धि हो। यो वृद्धिले बैंकिङ क्षेत्रमा कर्जा असुलीसम्बन्धी समस्या थप गहिरिएको संकेत गर्दछ।

यस अवधिमा अधिकांश बैंकहरूको एनपीएल बढेको देखिए पनि एभरेष्ट बैंक र स्ट्यान्डर्ड चार्टर्ड बैंकले भने आफ्नो एनपीएल घटाउन सफल भएका छन्। यसले बैंकिङ क्षेत्रमा जोखिम व्यवस्थापनलाई अझ सुदृढ बनाउनुको आवश्यकता देखाउँछ।

बैंक | २०७९ पुस (एनपीएल) | २०८० पुस (एनपीएल) | फरक (∆) |

|---|---|---|---|

कुमारी | ४.९७% | ६.९६% | +१.९९% |

नेपाल इन्भेष्टमेन्ट मेगा | ४.५८% | ५.८६% | +१.२८% |

लक्ष्मी सनराइज | ४.५६% | ५.६७% | +१.११% |

प्रभु | ४.०५% | ५.०६% | +१.०१% |

नेपाल बैंक | ४.९९% | ४.९९% | ०.००% |

हिमालयन | ४.३९% | ४.९८% | +०.५९% |

प्राइम कमर्सियल | ४.९६% | ४.९६% | ०.००% |

राष्ट्रिय वाणिज्य | ४.९६% | ४.९६% | ०.००% |

नबिल | ४.३२% | ४.९३% | +०.६१% |

कृषि विकास बैंक | ३.०२% | ४.९०% | +१.८८% |

ग्लोबल आइएमई | ४.२४% | ४.८९% | +०.६५% |

सिटिजन्स | ३.५४% | ४.६०% | +१.०६% |

एनआईसी एशिया | १.१९% | ४.६१% | +३.४२% |

माछापुच्छ्रे | ३.४५% | ३.५५% | +०.१०% |

सिद्धार्थ | २.४५% | २.५६% | +०.११% |

एनएमबि | ३.६५% | ३.६५% | ०.००% |

नेपाल एसबीआई | २.५५% | २.५६% | +०.०१% |

सानिमा | १.२२% | १.९२% | +०.७०% |

स्ट्यान्डर्ड चार्टर्ड | १.७७% | १.६६% | -०.११% |

एभरेष्ट | ०.७७% | ०.६६% | -०.११% |

औसत (Average) | ३.४०% | ४.४९% | +१.०९% |

१. सबैभन्दा धेरै एनपीएल भएका बैंकहरू

कुमारी बैंकले ६.९६% खराब कर्जाको अनुपातसहित सबैभन्दा बढी एनपीएल कायम गरेको छ।

अन्य बैंकहरू जसको एनपीएल ५% भन्दा माथि पुगेको छ:

नेपाल इन्भेष्टमेन्ट मेगा बैंक: ५.८६%

लक्ष्मी सनराइज बैंक: ५.६७%

प्रभु बैंक: ५.०६%

२. सबैभन्दा धेरै एनपीएल वृद्धि गर्ने बैंकहरू

एनआईसी एशिया बैंकको एनपीएल ३.४२ प्रतिशत बिन्दुले बढेर ४.६१% पुगेको छ।

कृषि विकास बैंकको एनपीएल १.८८ प्रतिशत बिन्दुले बढेर ४.९०% पुगेको छ।

३. एनपीएल घटाउन सफल बैंकहरू

एभरेष्ट बैंक र स्ट्यान्डर्ड चार्टर्ड बैंकले आफ्नो एनपीएल घटाउन सकेका छन्।

एभरेष्ट बैंक: ०.७७% बाट ०.६६% (-०.११%)।

स्ट्यान्डर्ड चार्टर्ड: १.७७% बाट १.६६% (-०.११%)।

४. औसत खराब कर्जा अनुपात

वाणिज्य बैंकहरूको औसत एनपीएल ३.४०% बाट ४.४९% पुगेको छ, जसले बैंकिङ क्षेत्रमा बढ्दो जोखिमलाई संकेत गर्दछ।

खराब कर्जा वृद्धि हुनुका कारणहरू

१. कर्जा असुलीको समस्या

ग्राहकहरूको व्यवसायिक गतिविधिमा मन्दीका कारण कर्जा किस्ता समयमा तिर्न नसकेको।

२. आर्थिक सुस्तता

आर्थिक मन्दीका कारण ऋणीले आफ्नो कर्जा भुक्तानीमा कठिनाइ भोगिरहेका छन्।

३. ब्याजदर वृद्धि

ब्याजदरको वृद्धिले कर्जाको लागत बढाएर किस्ता तिर्ने क्षमता घटाएको छ।

राष्ट्र बैंकको भूमिका र निर्देशन

नेपाल राष्ट्र बैंकले ५% भन्दा माथि एनपीएल भएका बैंकहरूलाई:

लाभांश वितरण गर्न नदिने।

नयाँ व्यवसाय विस्तार गर्न रोक लगाउने।

बैंकहरूलाई खराब कर्जा असुलीमा प्राथमिकता दिन निर्देशन दिएको छ।

१. कर्जा असुली प्रक्रियालाई सुदृढ गर्नुहोस्

बैंकहरूले कर्जा असुलीका लागि विशेष टोली गठन गरेर प्रभावकारी कदम चाल्न आवश्यक छ।

२. जोखिम व्यवस्थापन सुधार गर्नुहोस्

कर्जा प्रवाह गर्दा ग्राहकको वित्तीय अवस्था र जोखिम मूल्याङ्कनलाई प्राथमिकता दिनुपर्छ।

३. पोर्टफोलियोको विविधिकरण गर्नुहोस्

उच्च जोखिम भएका क्षेत्रमा निर्भरता घटाई विभिन्न क्षेत्रमा कर्जा प्रवाह गर्ने।

यो तथ्यांकले वाणिज्य बैंकहरूले आफ्नो कर्जा असुली प्रक्रियामा सुधार गरी आर्थिक स्थायित्वतर्फ अघि बढ्न आवश्यक रहेको देखाउँछ। आगामी दिनमा बैंकहरूले जोखिम न्यूनीकरण गर्दै कर्जा व्यवस्थापनलाई सुदृढ बनाउनुपर्ने आवश्यकता छ। यस्तो कदमले बैंकिङ क्षेत्रमा दीर्घकालीन स्थायित्व सुनिश्चित गर्नेछ।