वाणिज्य बैंकहरूको खराब कर्जा (एनपीएल) अनुपात: बढ्दो चुनौती र भविष्यको दिशाCommercial Banks' Non-Performing Loan (NPL) Ratio: Rising Challenges and Future Directions

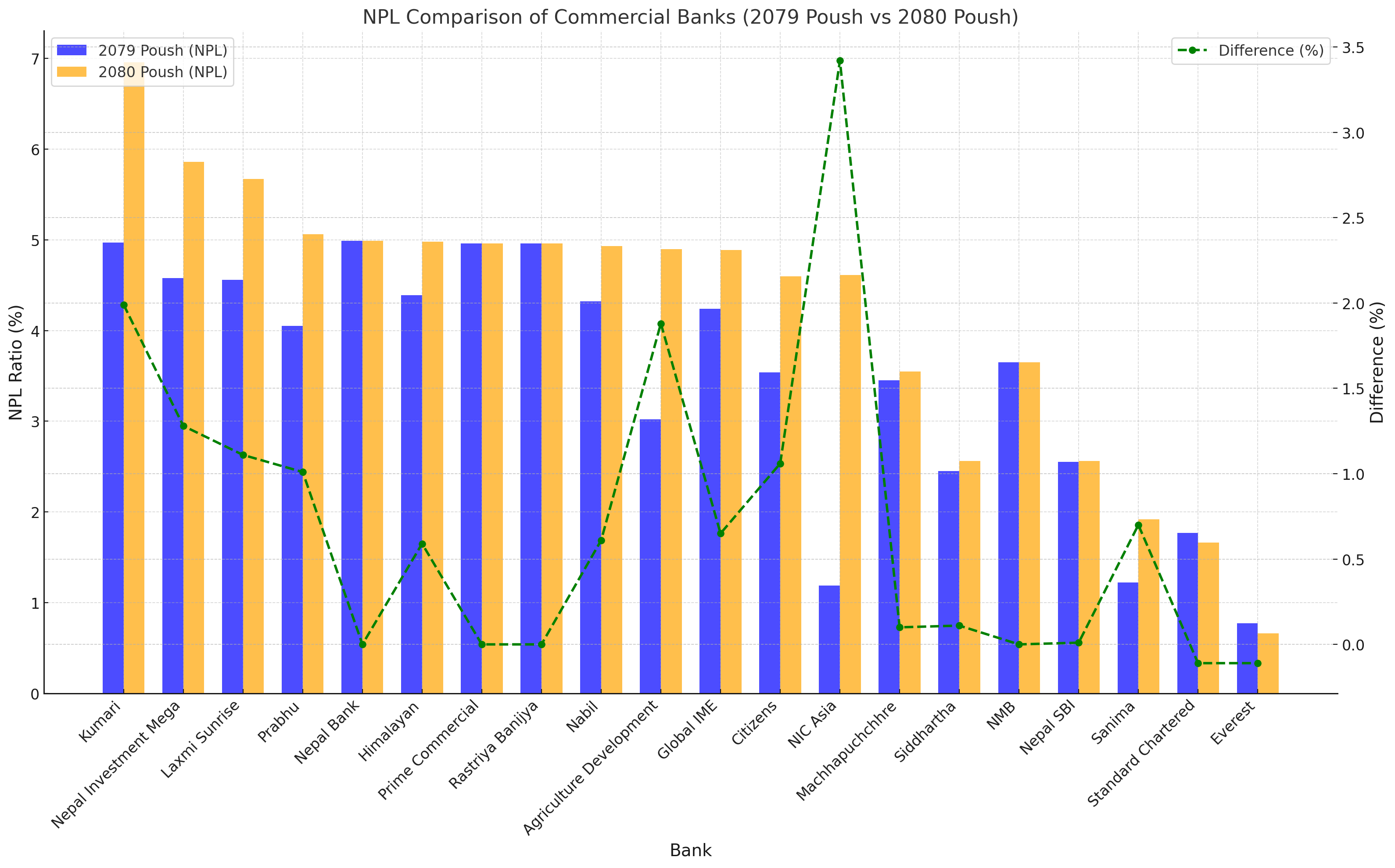

वाणिज्य बैंकहरूले आर्थिक वर्ष २०८० को पुस मसान्तसम्मको खराब कर्जा (एनपीएल) अनुपात सार्वजनिक गरेका छन्। तथ्यांकले देखाउँछ कि औसत खराब कर्जा अनुपात ३.४० प्रतिशतबाट बढेर ४.४९ प्रतिशत पुगेको छ, जुन १.०९ प्रतिशत बिन्दुले वृद्धि हो। यो वृद्धिले बैंकिङ क्षेत्रमा कर्जा असुलीसम्बन्धी समस्या थप गहिरिएको संकेत गर्दछ।

यस अवधिमा अधिकांश बैंकहरूको एनपीएल बढेको देखिए पनि एभरेष्ट बैंक र स्ट्यान्डर्ड चार्टर्ड बैंकले भने आफ्नो एनपीएल घटाउन सफल भएका छन्। यसले बैंकिङ क्षेत्रमा जोखिम व्यवस्थापनलाई अझ सुदृढ बनाउनुको आवश्यकता देखाउँछ।

बैंक | २०७९ पुस (एनपीएल) | २०८० पुस (एनपीएल) | फरक (∆) |

|---|---|---|---|

कुमारी | ४.९७% | ६.९६% | +१.९९% |

नेपाल इन्भेष्टमेन्ट मेगा | ४.५८% | ५.८६% | +१.२८% |

लक्ष्मी सनराइज | ४.५६% | ५.६७% | +१.११% |

प्रभु | ४.०५% | ५.०६% | +१.०१% |

नेपाल बैंक | ४.९९% | ४.९९% | ०.००% |

हिमालयन | ४.३९% | ४.९८% | +०.५९% |

प्राइम कमर्सियल | ४.९६% | ४.९६% | ०.००% |

राष्ट्रिय वाणिज्य | ४.९६% | ४.९६% | ०.००% |

नबिल | ४.३२% | ४.९३% | +०.६१% |

कृषि विकास बैंक | ३.०२% | ४.९०% | +१.८८% |

ग्लोबल आइएमई | ४.२४% | ४.८९% | +०.६५% |

सिटिजन्स | ३.५४% | ४.६०% | +१.०६% |

एनआईसी एशिया | १.१९% | ४.६१% | +३.४२% |

माछापुच्छ्रे | ३.४५% | ३.५५% | +०.१०% |

सिद्धार्थ | २.४५% | २.५६% | +०.११% |

एनएमबि | ३.६५% | ३.६५% | ०.००% |

नेपाल एसबीआई | २.५५% | २.५६% | +०.०१% |

सानिमा | १.२२% | १.९२% | +०.७०% |

स्ट्यान्डर्ड चार्टर्ड | १.७७% | १.६६% | -०.११% |

एभरेष्ट | ०.७७% | ०.६६% | -०.११% |

औसत (Average) | ३.४०% | ४.४९% | +१.०९% |

१. सबैभन्दा धेरै एनपीएल भएका बैंकहरू

कुमारी बैंकले ६.९६% खराब कर्जाको अनुपातसहित सबैभन्दा बढी एनपीएल कायम गरेको छ।

अन्य बैंकहरू जसको एनपीएल ५% भन्दा माथि पुगेको छ:

नेपाल इन्भेष्टमेन्ट मेगा बैंक: ५.८६%

लक्ष्मी सनराइज बैंक: ५.६७%

प्रभु बैंक: ५.०६%

२. सबैभन्दा धेरै एनपीएल वृद्धि गर्ने बैंकहरू

एनआईसी एशिया बैंकको एनपीएल ३.४२ प्रतिशत बिन्दुले बढेर ४.६१% पुगेको छ।

कृषि विकास बैंकको एनपीएल १.८८ प्रतिशत बिन्दुले बढेर ४.९०% पुगेको छ।

३. एनपीएल घटाउन सफल बैंकहरू

एभरेष्ट बैंक र स्ट्यान्डर्ड चार्टर्ड बैंकले आफ्नो एनपीएल घटाउन सकेका छन्।

एभरेष्ट बैंक: ०.७७% बाट ०.६६% (-०.११%)।

स्ट्यान्डर्ड चार्टर्ड: १.७७% बाट १.६६% (-०.११%)।

४. औसत खराब कर्जा अनुपात

वाणिज्य बैंकहरूको औसत एनपीएल ३.४०% बाट ४.४९% पुगेको छ, जसले बैंकिङ क्षेत्रमा बढ्दो जोखिमलाई संकेत गर्दछ।

खराब कर्जा वृद्धि हुनुका कारणहरू

१. कर्जा असुलीको समस्या

ग्राहकहरूको व्यवसायिक गतिविधिमा मन्दीका कारण कर्जा किस्ता समयमा तिर्न नसकेको।

२. आर्थिक सुस्तता

आर्थिक मन्दीका कारण ऋणीले आफ्नो कर्जा भुक्तानीमा कठिनाइ भोगिरहेका छन्।

३. ब्याजदर वृद्धि

ब्याजदरको वृद्धिले कर्जाको लागत बढाएर किस्ता तिर्ने क्षमता घटाएको छ।

राष्ट्र बैंकको भूमिका र निर्देशन

नेपाल राष्ट्र बैंकले ५% भन्दा माथि एनपीएल भएका बैंकहरूलाई:

लाभांश वितरण गर्न नदिने।

नयाँ व्यवसाय विस्तार गर्न रोक लगाउने।

बैंकहरूलाई खराब कर्जा असुलीमा प्राथमिकता दिन निर्देशन दिएको छ।

१. कर्जा असुली प्रक्रियालाई सुदृढ गर्नुहोस्

बैंकहरूले कर्जा असुलीका लागि विशेष टोली गठन गरेर प्रभावकारी कदम चाल्न आवश्यक छ।

२. जोखिम व्यवस्थापन सुधार गर्नुहोस्

कर्जा प्रवाह गर्दा ग्राहकको वित्तीय अवस्था र जोखिम मूल्याङ्कनलाई प्राथमिकता दिनुपर्छ।

३. पोर्टफोलियोको विविधिकरण गर्नुहोस्

उच्च जोखिम भएका क्षेत्रमा निर्भरता घटाई विभिन्न क्षेत्रमा कर्जा प्रवाह गर्ने।

यो तथ्यांकले वाणिज्य बैंकहरूले आफ्नो कर्जा असुली प्रक्रियामा सुधार गरी आर्थिक स्थायित्वतर्फ अघि बढ्न आवश्यक रहेको देखाउँछ। आगामी दिनमा बैंकहरूले जोखिम न्यूनीकरण गर्दै कर्जा व्यवस्थापनलाई सुदृढ बनाउनुपर्ने आवश्यकता छ। यस्तो कदमले बैंकिङ क्षेत्रमा दीर्घकालीन स्थायित्व सुनिश्चित गर्नेछ।

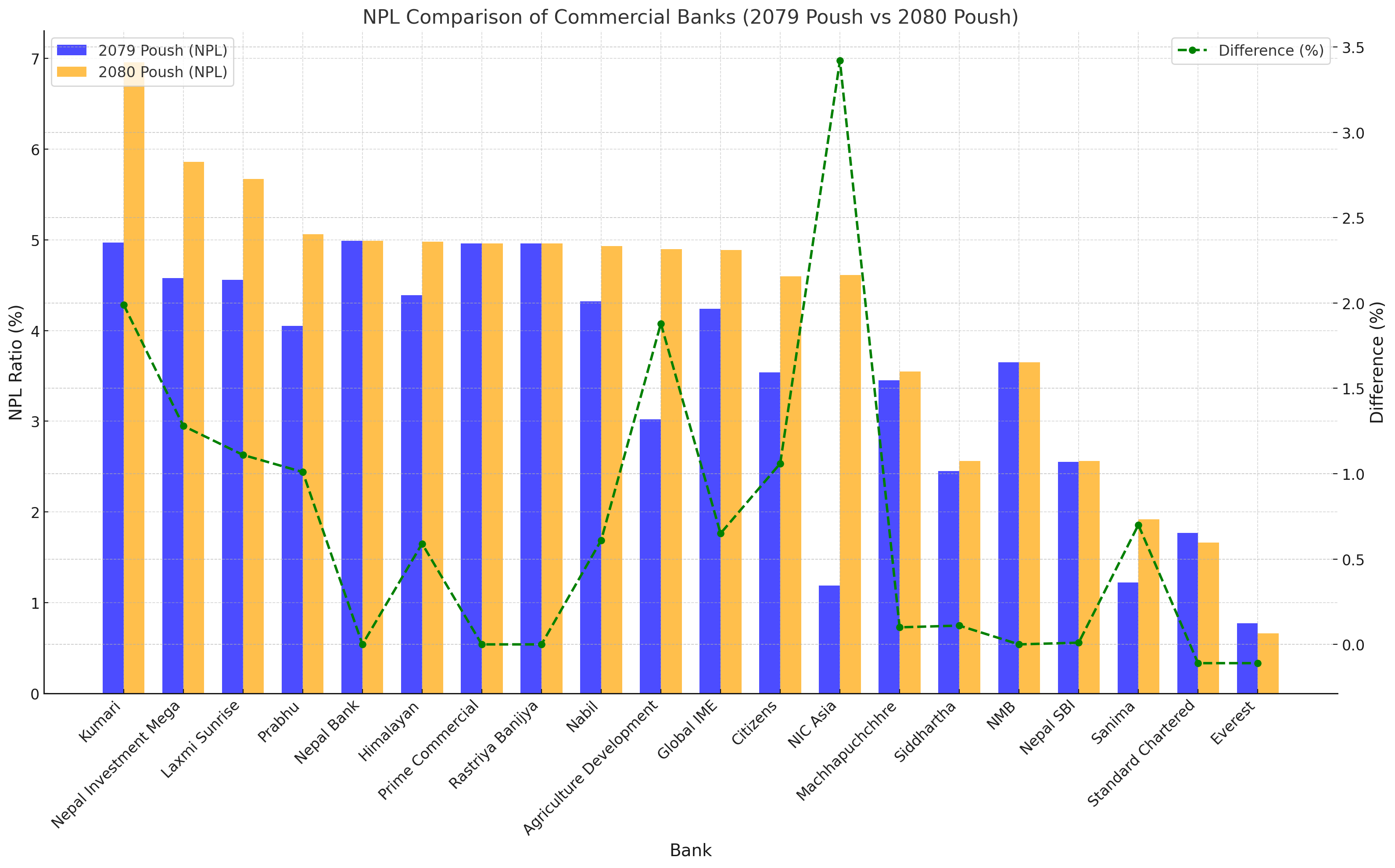

The Non-Performing Loan (NPL) ratios of Nepal's commercial banks for FY 2080 Poush reveal a concerning rise, signaling growing challenges in loan recovery. According to the data, the average NPL ratio increased by 1.09 percentage points, climbing from 3.40% in FY 2079 Poush to 4.49% in FY 2080 Poush. This surge indicates a need for immediate attention to credit risk management across the banking sector.

While most banks recorded an increase in NPL ratios, only two banks—Everest Bank and Standard Chartered Bank—managed to reduce their NPL levels. The trend highlights the urgent need for strategic interventions to address loan recovery issues.

Bank | 2079 Poush (NPL) | 2080 Poush (NPL) | Difference (∆) |

|---|---|---|---|

Kumari | 4.97% | 6.96% | +1.99% |

Nepal Investment Mega | 4.58% | 5.86% | +1.28% |

Laxmi Sunrise | 4.56% | 5.67% | +1.11% |

Prabhu | 4.05% | 5.06% | +1.01% |

Nepal Bank | 4.99% | 4.99% | 0.00% |

Himalayan | 4.39% | 4.98% | +0.59% |

Prime Commercial | 4.96% | 4.96% | 0.00% |

Rastriya Banijya | 4.96% | 4.96% | 0.00% |

Nabil | 4.32% | 4.93% | +0.61% |

Agriculture Development | 3.02% | 4.90% | +1.88% |

Global IME | 4.24% | 4.89% | +0.65% |

Citizens | 3.54% | 4.60% | +1.06% |

NIC Asia | 1.19% | 4.61% | +3.42% |

Machhapuchchhre | 3.45% | 3.55% | +0.10% |

Siddhartha | 2.45% | 2.56% | +0.11% |

NMB | 3.65% | 3.65% | 0.00% |

Nepal SBI | 2.55% | 2.56% | +0.01% |

Sanima | 1.22% | 1.92% | +0.70% |

Standard Chartered | 1.77% | 1.66% | -0.11% |

Everest | 0.77% | 0.66% | -0.11% |

Average (All Banks) | 3.40% | 4.49% | +1.09% |

1. Banks with the Highest NPL Ratios

Kumari Bank reported the highest NPL ratio at 6.96%, an increase of 1.99 percentage points from the previous year.

Other banks exceeding the critical 5% threshold include:

Nepal Investment Mega Bank: 5.86%

Laxmi Sunrise Bank: 5.67%

Prabhu Bank: 5.06%

These banks now face limitations imposed by Nepal Rastra Bank (NRB), which prohibits banks with NPLs above 5% from distributing dividends or expanding their business.

2. Banks with the Most Significant NPL Increase

NIC Asia Bank experienced the largest rise in NPL ratio, increasing by 3.42 percentage points to 4.61%. This sharp rise reflects challenges in loan recovery and higher credit risks.

Agriculture Development Bank recorded the second-largest increase of 1.88 percentage points, reaching 4.90%.

3. Banks Reducing NPL Ratios

Everest Bank and Standard Chartered Bank were the only banks to reduce their NPL ratios:

Everest Bank: Reduced from 0.77% to 0.66% (-0.11%).

Standard Chartered: Reduced from 1.77% to 1.66% (-0.11%).

These improvements reflect better credit risk management and focused loan recovery efforts.

4. Industry Average

The average NPL ratio increased from 3.40% in FY 2079 Poush to 4.49% in FY 2080 Poush, indicating a worsening trend across the sector.

Factors Behind the Increase in NPL Ratios

Loan Recovery Challenges

Borrowers have faced difficulties in repaying loans due to economic uncertainties and business disruptions.

Economic Slowdown

The overall economic slowdown has led to reduced revenues for businesses, making it harder for them to meet repayment obligations.

High-Interest Rates

Rising interest rates have increased the financial burden on borrowers, especially small and medium enterprises (SMEs).

Inadequate Credit Monitoring

Some banks failed to implement rigorous monitoring of loan portfolios, resulting in delayed identification of repayment risks.

Implications of High NPL Ratios

Impact on Financial Health

High NPLs weaken a bank's financial stability, as provisions for bad loans reduce profitability.

Regulatory Restrictions

As per NRB regulations, banks with NPLs exceeding 5% cannot:

Distribute dividends to shareholders.

Expand their loan portfolios or undertake new business ventures.

These restrictions aim to push banks toward improving loan recovery efforts.

Future Risks

Persistent increases in NPL ratios could lead to reduced investor confidence and a tightening of credit availability in the market.

Recommendations for Banks

Strengthen Loan Recovery Processes

Banks must focus on recovering bad loans by allocating resources to debt collection and negotiating with defaulters.

Improve Risk Management Practices

Implement robust credit evaluation systems to identify high-risk borrowers before loan approval.

Monitor Loan Portfolios Regularly

Conduct frequent reviews of loan portfolios to detect early signs of repayment challenges and take corrective actions.

Diversify Loan Portfolios

Reduce dependency on a few high-risk sectors by diversifying loans across different industries.

The rising NPL ratios highlight the critical need for banks to enhance their credit risk management and focus on loan recovery. The challenges faced by the banking sector are an opportunity to implement stronger internal controls and adopt more effective lending practices.

Banks that can successfully address their NPL issues will not only stabilize their financial performance but also contribute to the long-term resilience of Nepal's banking system.