सिटिजन्स बैंक इन्टरनेसनल लिमिटेडको दोस्रो त्रैमास २०८१/८२ को वित्तीय विश्लेषणDetailed Financial Analysis of Citizen Bank International Limited for the Second Quarter of FY 2081/82

सिटिजन्स बैंक इन्टरनेसनल लिमिटेडले चालु आर्थिक वर्ष २०८१/८२ को दोस्रो त्रैमासमा ६६ करोड १८ लाख रुपैयाँ खुद नाफा आर्जन गरेको छ। यो नाफा गत वर्षको यसै अवधिमा आर्जित ७८ करोड २७ लाख रुपैयाँभन्दा १५.४५% ले कम हो। नाफा घट्नुको प्रमुख कारण इम्पेयरमेन्ट चार्जमा भएको उल्लेखनीय वृद्धि हो।

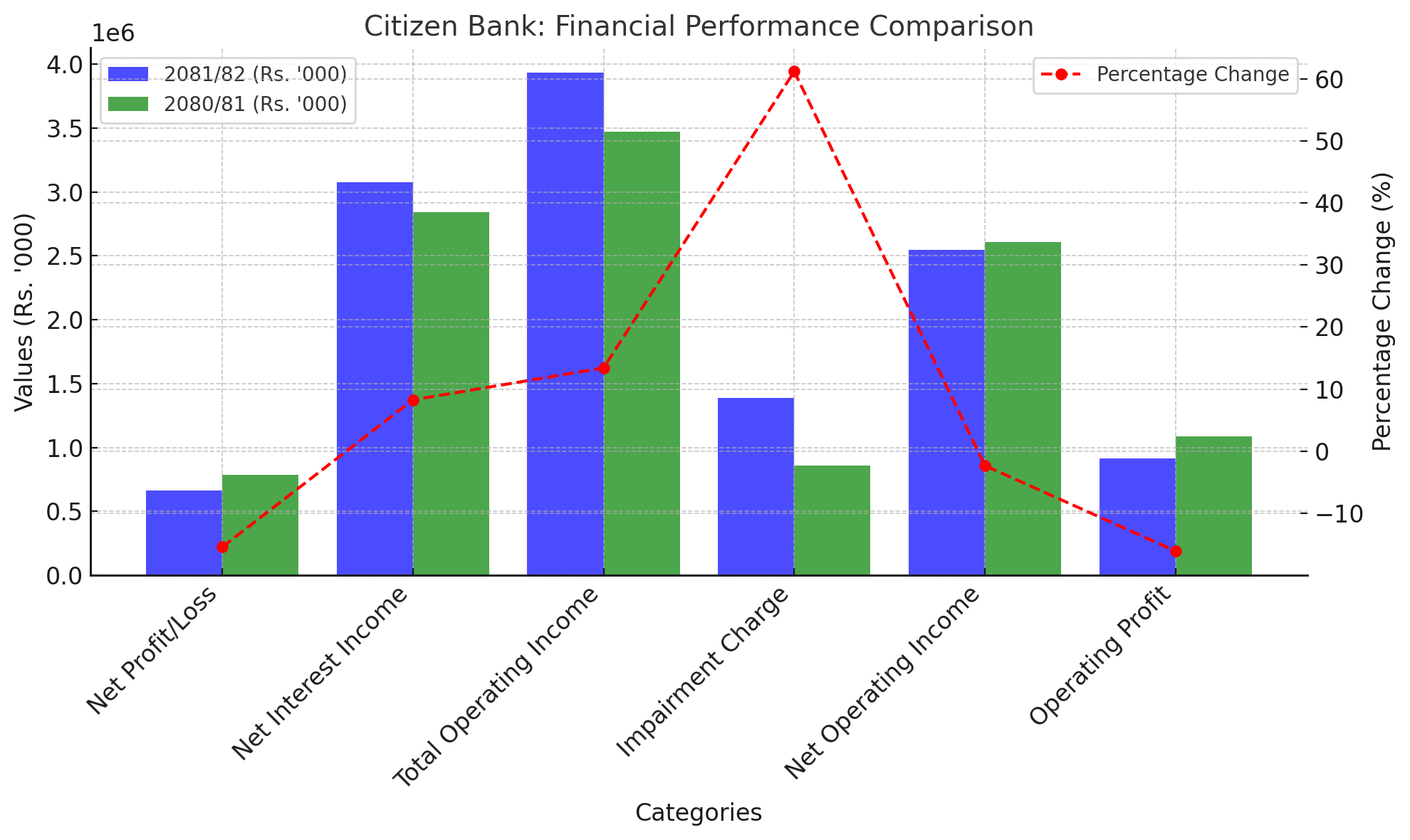

विवरण | २ त्रैमास, २०८१/८२ (रु. '000) | २ त्रैमास, २०८०/८१ (रु. '000) | अन्तर (%) |

|---|---|---|---|

खुद नाफा | ६६१,८२८ | ७८२,७८४ | -१५.४५ |

खुद ब्याज आम्दानी | ३०७४,५७१ | २८३९,८३१ | ८.२७ |

कुल सञ्चालन आम्दानी | ३९३४,५५८ | ३४६९,३५१ | १३.४१ |

इम्पेयरमेन्ट चार्ज | १३८५,३५४ | ८५९,५०१ | ६१.१८ |

सञ्चालन आम्दानी | २५४९,२०४ | २६०९,८५० | -२.३२ |

सञ्चालन मुनाफा | ९११,३९१ | १०८६,४५४ | -१६.११ |

१. खुद नाफामा गिरावट

बैंकको खुद नाफा १५.४५% ले घटेर गत वर्षको ७८ करोड २७ लाख रुपैयाँबाट ६६ करोड १८ लाख रुपैयाँ पुगेको छ। यो गिरावटको मुख्य कारण इम्पेयरमेन्ट चार्जमा ६१.१८% वृद्धि हुनु हो, जुन ८५ करोड ९५ लाख रुपैयाँबाट १ अर्ब ३८ करोड ५३ लाख रुपैयाँ पुगेको छ।

२. मुख्य व्यवसायमा सुधार

बैंकको खुद ब्याज आम्दानी गत वर्षको २ अर्ब ८३ करोड रुपैयाँबाट बढेर ३ अर्ब ७ करोड रुपैयाँ पुगेको छ, जसले ८.२७% को वृद्धि देखाएको छ।

त्यस्तै, कुल सञ्चालन आम्दानी पनि १३.४१% ले वृद्धि भएर ३ अर्ब ९३ करोड रुपैयाँ पुगेको छ।

३. सञ्चालन मुनाफामा गिरावट

सञ्चालन आम्दानीमा सुधार भए पनि, सञ्चालन मुनाफा १६.११% ले घटेर ९१ करोड १३ लाख रुपैयाँमा झरेको छ। यसले उच्च इम्पेयरमेन्ट चार्ज र सञ्चालन खर्चको प्रभाव देखाउँछ।

४. चुक्ता पुँजी र जगेडा कोष

बैंकको चुक्ता पुँजी १४ अर्ब ७६ करोड रुपैयाँ छ, जुन गत वर्षको तुलनामा ४.००% ले वृद्धि भएको हो।

जगेडा कोष ६ अर्ब ७६ करोड रुपैयाँबाट ७ अर्ब २८ करोड रुपैयाँ पुगेको छ, जसले ७.७६% को वृद्धि देखाएको छ।

५. ऋण र निक्षेपमा वृद्धि

ग्राहक निक्षेप २.४२% ले वृद्धि भएर १ खर्ब ९३ अर्ब ८१ करोड रुपैयाँ पुगेको छ।

ऋण तथा लगानी ५.२२% ले वृद्धि भएर १ खर्ब ६१ अर्ब ३५ करोड रुपैयाँ पुगेको छ।

६. एनपीएल (Non-Performing Loan) मा वृद्धि

बैंकको नेट एनपीएल अनुपात गत वर्षको ४.०७% बाट ४.८५% मा पुगेको छ। यो वृद्धि बैंकको ऋणको गुणस्तरमा सुधारको आवश्यकता देखाउँछ।

७. खर्च व्यवस्थापनमा सुधार

बैंकको कोषको खर्च (Cost of Funds) ७.७७% बाट घटेर ५.२७% मा झरेको छ, जसले खर्च व्यवस्थापन सुधार देखाउँछ।

आधार दर (Base Rate) ९.८१% बाट घटेर ७.३०% मा पुगेको छ, जसले बैंकलाई प्रतिस्पर्धात्मक बनाएको छ।

८. प्रतिसेयर सूचकांकहरू

बैंकको प्रतिसेयर आम्दानी (EPS) ११.०२ रुपैयाँबाट घटेर ८.९६ रुपैयाँ मा झरेको छ।

प्रतिसेयर नेटवर्थ १५०.३९ रुपैयाँ छ, जसले बैंकको दीर्घकालीन स्थायित्व झल्काउँछ।

सकारात्मक पक्षहरू

ब्याज आम्दानी र सञ्चालन आम्दानीमा सुधार।

जगेडा कोष र चुक्ता पुँजीमा स्थिरता।

खर्च व्यवस्थापन सुधार, जसले कोषको खर्च र आधार दर घटाएको छ।

चुनौतीहरू

इम्पेयरमेन्ट चार्जमा तीव्र वृद्धि।

एनपीएल अनुपातमा वृद्धि, जसले ऋणको गुणस्तर सुधार गर्न चुनौती थपेको छ।

खुद नाफा र EPS मा कमी।

सिटिजन्स बैंकले खर्च व्यवस्थापन र सञ्चालन आम्दानीमा सुधार देखाए पनि, इम्पेयरमेन्ट चार्ज र एनपीएल वृद्धि जस्ता मुद्दाले बैंकको नाफामा गिरावट ल्याएको छ।

आगामी त्रैमासमा ऋण गुणस्तर सुधार र इम्पेयरमेन्ट चार्ज घटाउने रणनीति अनिवार्य देखिन्छ। लगानीकर्ताका लागि बैंकको दीर्घकालीन स्थायित्व सकारात्मक भए पनि, छोटो अवधिमा थप सुधारका लागि चुनौतीहरू बाँकी छन्।

Citizen Bank International Limited has posted a net profit of Rs. 66.18 crores for the second quarter of FY 2081/82. This represents a 15.45% decline compared to the same period last year, where the bank had achieved a net profit of Rs. 78.27 crores. The decline in profit can be primarily attributed to a significant increase in impairment charges during the period.

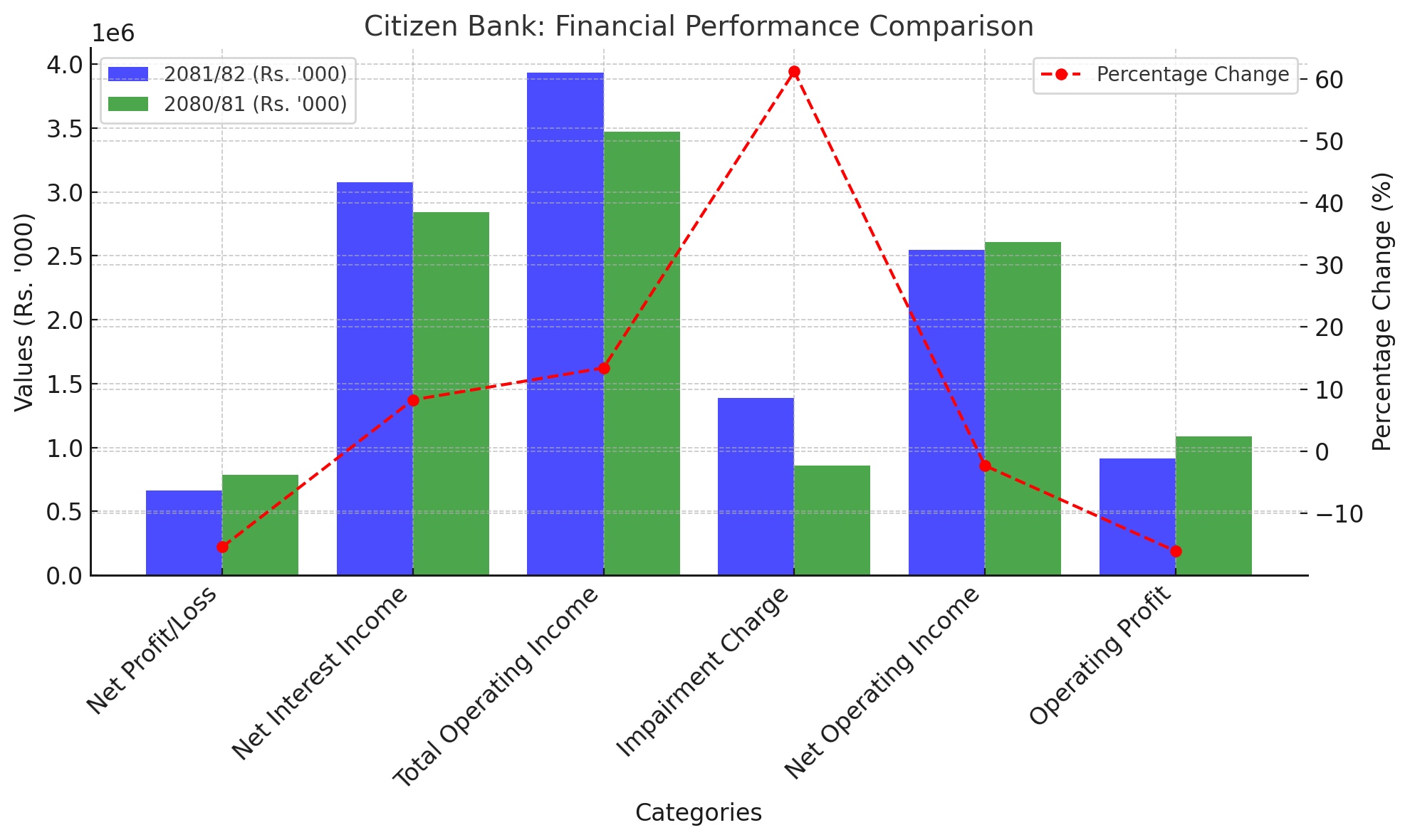

Particulars | 2nd Qtr, 2081/82 (Rs. '000) | 2nd Qtr, 2080/81 (Rs. '000) | Change (%) |

|---|---|---|---|

Net Profit/Loss | 661,828 | 782,784 | -15.45 |

Net Interest Income | 3,074,571 | 2,839,831 | 8.27 |

Total Operating Income | 3,934,558 | 3,469,351 | 13.41 |

Impairment Charge/ (Reversal) | 1,385,354 | 859,501 | 61.18 |

Net Operating Income | 2,549,204 | 2,609,850 | -2.32 |

Operating Profit | 911,391 | 1,086,454 | -16.11 |

1. Decline in Net Profit

The bank’s net profit fell by 15.45% to Rs. 66.18 crores from Rs. 78.27 crores last year. This decline is primarily due to a 61.18% increase in impairment charges, which rose from Rs. 85.95 crores to Rs. 138.53 crores. This sharp rise in provisions for bad loans indicates a challenge in the bank's asset quality.

2. Improvement in Core Operations

Despite the decline in profit, the bank's core operations showed growth:

Net Interest Income grew by 8.27%, reaching Rs. 307.45 crores from Rs. 283.98 crores. This demonstrates an improvement in the bank's ability to earn from its lending and borrowing activities.

Total Operating Income rose by 13.41%, reaching Rs. 393.45 crores from Rs. 346.93 crores, indicating better efficiency in overall operations.

3. Decline in Operating Profit

Although the operating income increased, the operating profit dropped by 16.11% to Rs. 91.13 crores from Rs. 108.64 crores. This reflects the adverse impact of higher impairment charges and other operating expenses.

4. Capital and Reserves

The bank's paid-up capital increased by 4.00%, reaching Rs. 1,476.90 crores.

The reserve fund grew by 7.76%, totaling Rs. 728.45 crores, reflecting financial stability and retained earnings capacity.

5. Loans and Deposits Growth

Deposits from Customers rose by 2.42%, reaching Rs. 1,938.15 crores.

Loans and Advances increased by 5.22%, reaching Rs. 1,613.50 crores. This growth indicates the bank’s expanded lending activities, though it must address asset quality issues.

6. Challenges in Asset Quality

The Non-Performing Loan (NPL) ratio increased from 4.07% to 4.85%, signaling a deterioration in the quality of the bank’s loan portfolio. This rise underscores the need for enhanced credit risk management.

7. Cost Efficiency

The Cost of Funds decreased from 7.77% to 5.27%, reflecting better operational efficiency.

The Base Rate dropped from 9.81% to 7.30%, making the bank more competitive in the market.

8. Per-Share Metrics

The bank’s Earnings Per Share (EPS) declined from Rs. 11.02 to Rs. 8.96, reflecting reduced profitability.

The Net Worth Per Share was Rs. 150.39, indicating strong capital adequacy.

Positive Aspects

Growth in core income: Net interest income and total operating income showed healthy growth, reflecting strong operational performance.

Improved cost efficiency: The reduction in cost of funds and base rate highlights better resource management.

Capital strength: Paid-up capital and reserves have both increased, indicating financial stability.

Challenges

Higher impairment charges: The significant rise in provisions has negatively impacted profitability.

Deterioration in asset quality: The increase in NPL ratio points to potential risks in the loan portfolio.

Decline in profitability: Both net profit and earnings per share have dropped significantly, affecting shareholder returns.

Citizen Bank International Limited has showcased growth in operational efficiency and core income. However, the sharp increase in impairment charges and the rise in the NPL ratio have overshadowed its achievements, leading to a decline in net profit. Moving forward, the bank must focus on improving asset quality and managing provisions to ensure sustainable growth and profitability.

For investors, the bank remains stable in terms of capital and reserves, but it faces challenges that need addressing to maintain long-term performance.