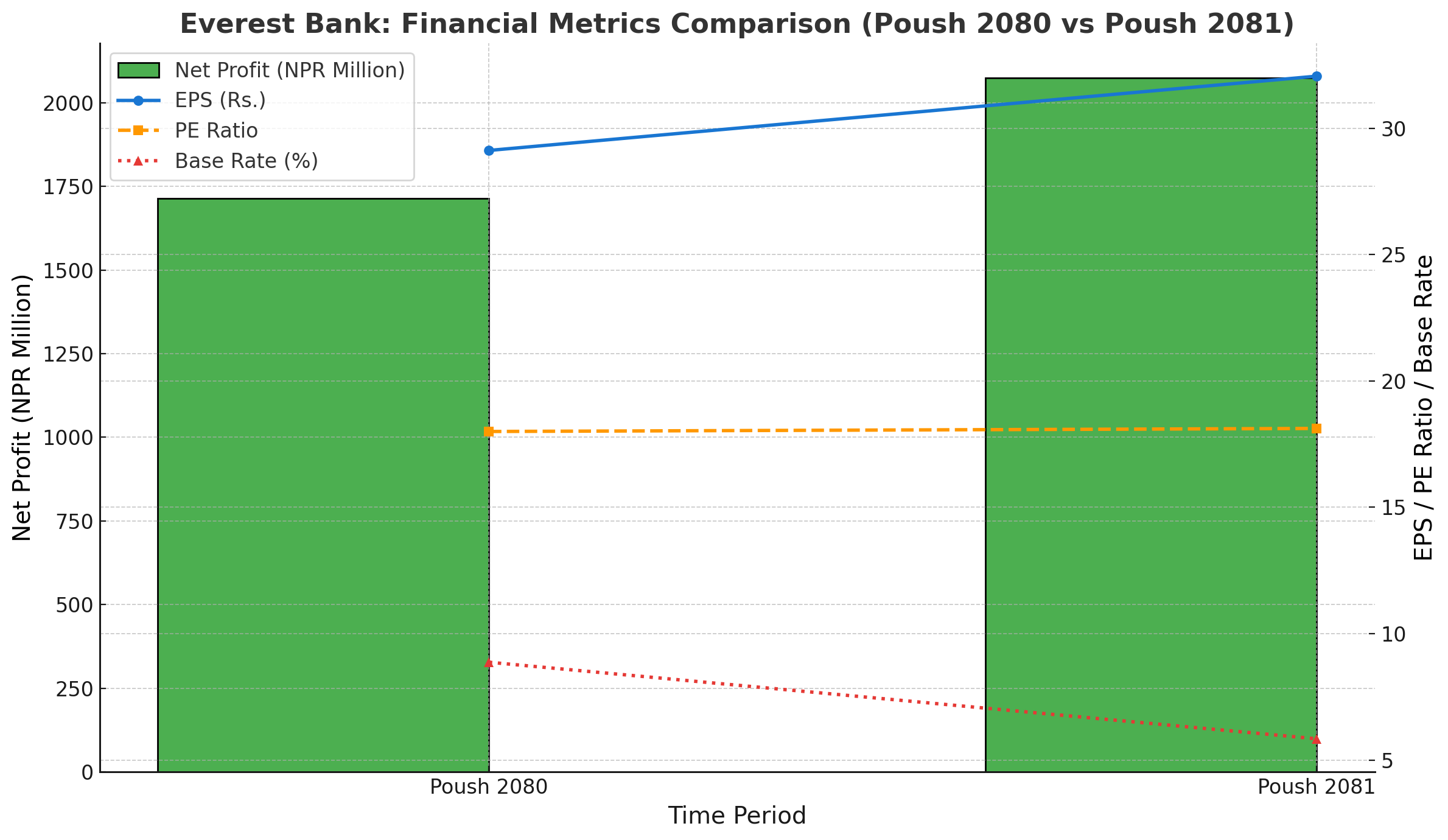

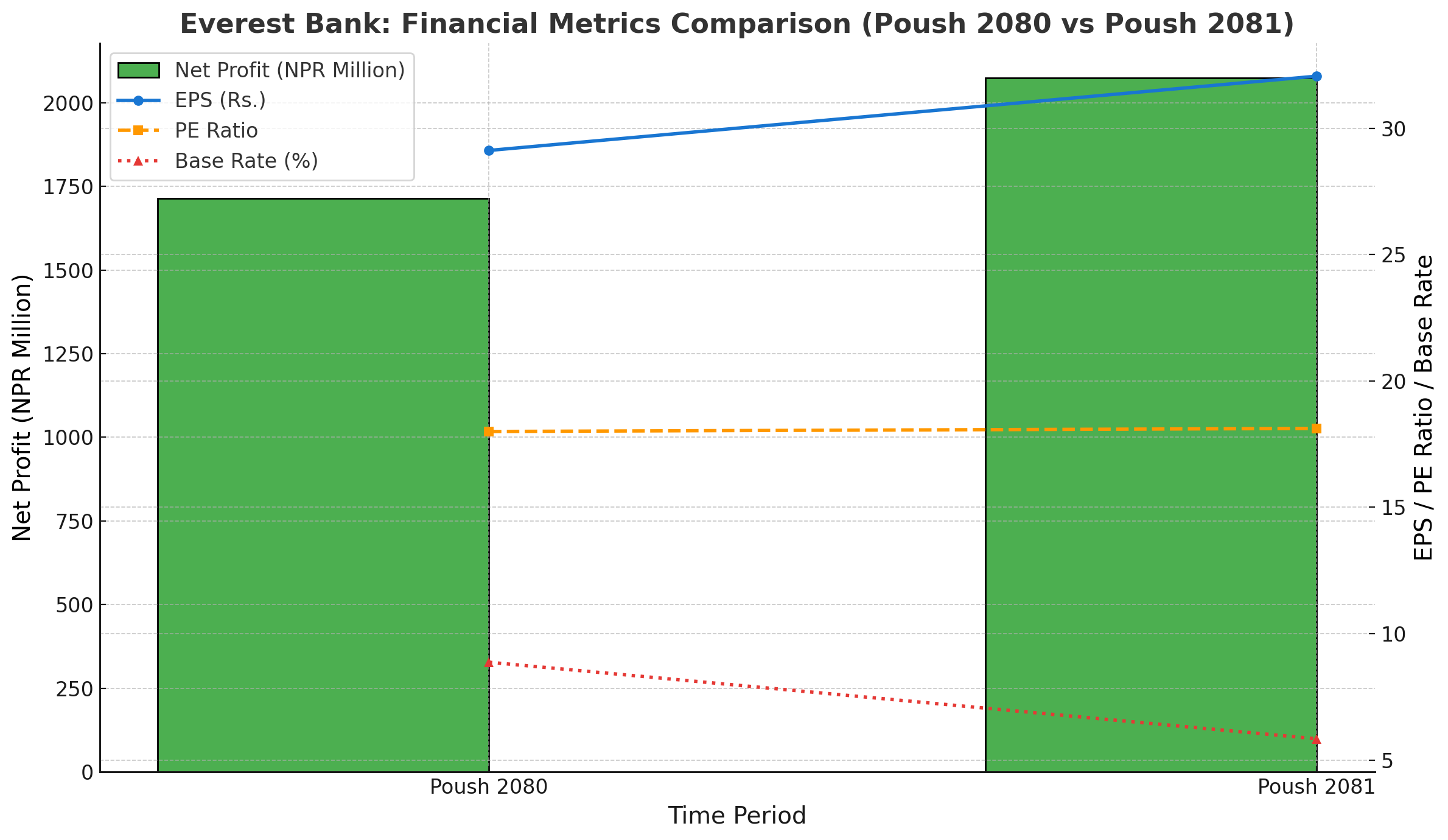

एभरेष्ट बैंक लिमिटेड (EBL) ले आर्थिक वर्ष २०८१ को दोस्रो त्रैमाससम्मको अपरिष्कृत वित्तीय विवरण सार्वजनिक गरेको छ। विवरण अनुसार, बैंकले २ अर्ब ७ करोड ४७ लाख रुपैयाँ खुद नाफा आर्जन गरेको छ, जुन अघिल्लो वर्षको सोही अवधिको तुलनामा २१.११% ले वृद्धि हो। गत वर्षको सोही अवधिमा बैंकको खुद नाफा १ अर्ब ७१ करोड ३१ लाख रुपैयाँ थियो। यो वृद्धि बैंकले ब्याज आम्दानी बढाउनु र खर्च व्यवस्थापन सुधार्नुका साथै इम्पेरमेन्ट चार्ज घटाउन सफल भएकाले सम्भव भएको हो।

खुद नाफामा उल्लेख्य वृद्धि

बैंकले चालु त्रैमासमा ३६ करोड १६ लाख रुपैयाँले खुद नाफा बढाएको छ। यो वृद्धि बैंकको सञ्चालन कुशलता र ग्राहकहरूको बढ्दो विश्वासलाई पुष्टि गर्छ।

खुद ब्याज आम्दानी (Net Interest Income)

बैंकको खुद ब्याज आम्दानी १९.११% ले वृद्धि भई ३ अर्ब ६२ करोड रुपैयाँबाट ४ अर्ब ३१ करोड रुपैयाँ पुगेको छ। यो बैंकको प्रभावकारी ऋण व्यवस्थापन र व्याज दर फैलावटको कुशल उपयोगको संकेत हो।

शुल्क र कमिशन आम्दानी (Fee and Commission Income)

खुद शुल्क र कमिशन आम्दानी १४.४६% ले वृद्धि भई ६६ करोड ८४ लाख रुपैयाँबाट ७६ करोड ५० लाख रुपैयाँ पुगेको छ। यसले सेवा शुल्क, कार्ड जारी गर्ने शुल्क र अन्य बैंकिङ सेवा मार्फत आम्दानी बढेको देखाउँछ।

सञ्चालन आम्दानी (Operating Income)

कुल सञ्चालन आम्दानी १७.६९% ले वृद्धि भई ४ अर्ब ५० करोड रुपैयाँबाट ५ अर्ब २९ करोड रुपैयाँ पुगेको छ, जसले बैंकको आर्थिक बलियो आधारलाई पुष्टि गर्छ।

इम्पेरमेन्ट चार्जमा कमी

इम्पेरमेन्ट चार्ज ४३ करोड २३ लाख रुपैयाँबाट घटेर ३४ करोड ९५ लाख रुपैयाँमा झरेको छ। यसले बैंकको सम्पत्ति गुणस्तरमा सुधार र जोखिम व्यवस्थापन प्रभावकारी भएको संकेत गर्दछ।

सञ्चालन मुनाफा (Operating Profit)

बैंकको सञ्चालन मुनाफा २६.९७% ले वृद्धि भई ३ अर्ब १० करोड रुपैयाँ पुगेको छ, जुन अघिल्लो वर्षको २ अर्ब ४४ करोड रुपैयाँ थियो।

प्रति शेयर आम्दानी (EPS)

बैंकको EPS २.९४ रुपैयाँले बढेर ३२.०६ रुपैयाँ पुगेको छ, जसले लगानीकर्ताहरूका लागि राम्रो प्रतिफलको संकेत गर्दछ।

प्रति शेयर नेटवर्थ (Net Worth Per Share)

२२५.७९ रुपैयाँ पुगेको छ, जसले बैंकको सुदृढ वित्तीय अवस्थालाई झल्काउँछ।

PE अनुपात (PE Ratio)

१८.१२ गुणा रहेको छ, जुन स्थिर छ।

आधार दर (Base Rate)

आधार दर ८.८७% बाट घटेर ५.८४% मा झरेको छ। यो घटावटले बैंकको ऋण प्रतिस्पर्धा बढाउनेछ।

निक्षेप र कर्जा (Deposits and Loans)

निक्षेप

ग्राहक निक्षेप ७.८०% ले वृद्धि भई २ खर्ब ५० अर्ब रुपैयाँ पुगेको छ।

कर्जा लगानी

कर्जा लगानी १६.९६% ले वृद्धि भई २ खर्ब ८ अर्ब रुपैयाँ पुगेको छ।

कर्जा-निक्षेप अनुपात (LDR)

८५.३९% पुगेको छ, जसले बैंकले निक्षेपलाई प्रभावकारी रूपमा लगानी गर्न सफल भएको देखाउँछ।

आधार दरमा गिरावट

आधार दर घट्नुले ऋणग्राहीहरूका लागि आकर्षक भए पनि बैंकको व्याज आम्दानीमा असर पर्न सक्ने जोखिम छ।

सम्पत्ति गुणस्तरको व्यवस्थापन

सम्पत्ति गुणस्तर कायम राख्न बैंकलाई जोखिम व्यवस्थापनमा सतर्क रहन आवश्यक छ।

एभरेष्ट बैंकले चालु आर्थिक वर्षको दोस्रो त्रैमासमा वित्तीय सूचकहरूमा उल्लेखनीय वृद्धि हासिल गरेको छ। शुल्क र व्याज आम्दानीको वृद्धि, इम्पेरमेन्ट चार्जको कमी, र निक्षेप तथा कर्जाको राम्रो व्यवस्थापनले बैंकलाई प्रतिस्पर्धात्मक बनाएको छ।

लगानीकर्ताहरूका लागि उच्च प्रतिफल, ग्राहकहरूका लागि आकर्षक दर, र समग्र रूपमा बलियो वित्तीय स्थिति बैंकको आगामी सफलताका लागि सकारात्मक संकेत हुन्। बैंकले चालु रणनीतिलाई निरन्तरता दिएमा आगामी त्रैमासहरूमा पनि थप उत्कृष्टता हासिल गर्न सक्छ।