कुमारी बैंक लिमिटेडले आर्थिक वर्ष २०८१/८२ को दोस्रो त्रैमाससम्मको अपरिष्कृत वित्तीय विवरण सार्वजनिक गरेको छ। यो विवरणले बैंकको नाफा, आम्दानी, कर्जा प्रवाह, र अन्य वित्तीय सूचकहरूको स्थिति उजागर गरेको छ। समीक्षाको आधारमा बैंकले चालु आर्थिक वर्षमा उल्लेखनीय चुनौतीहरूको सामना गरेको देखिन्छ।

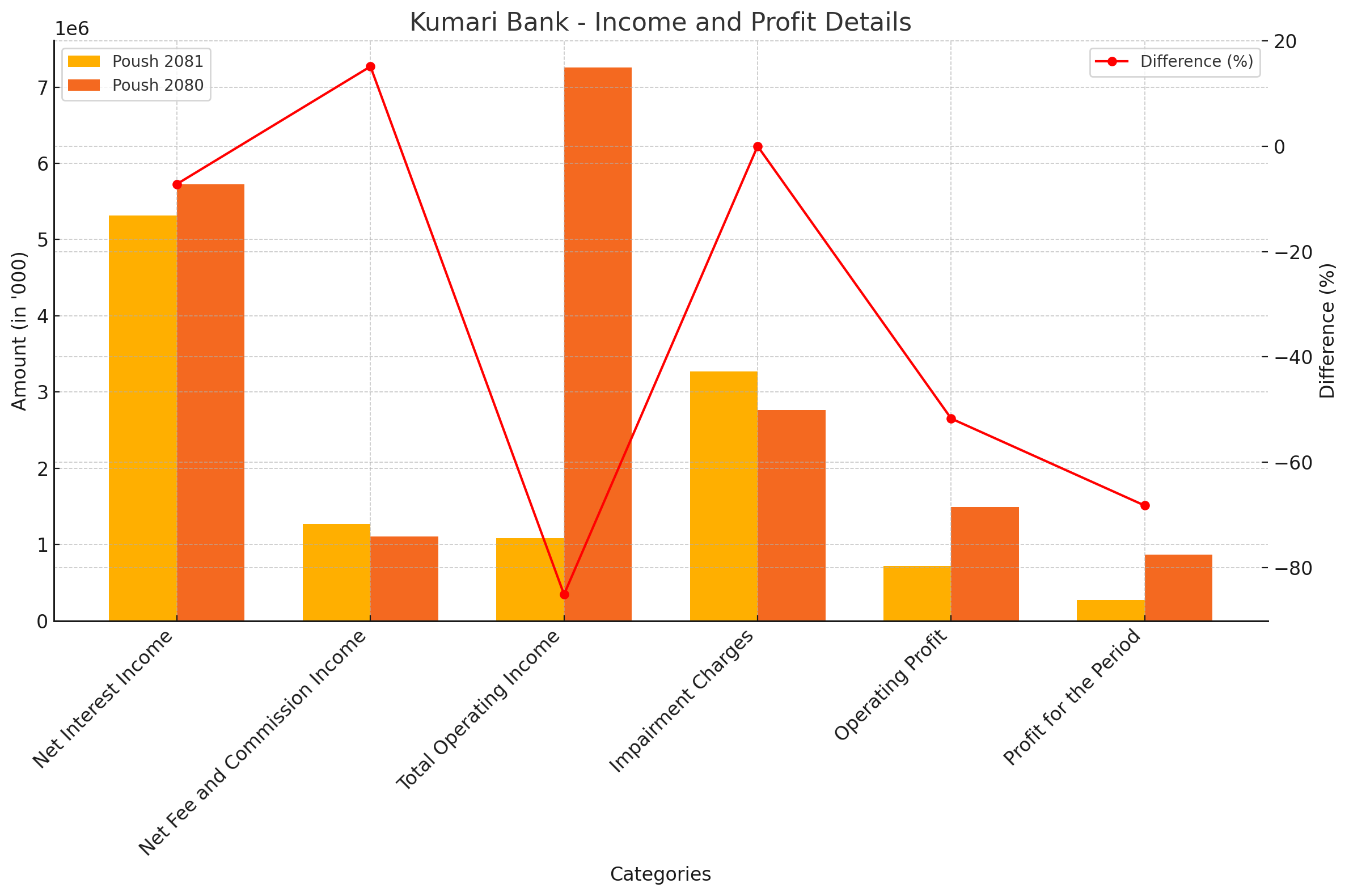

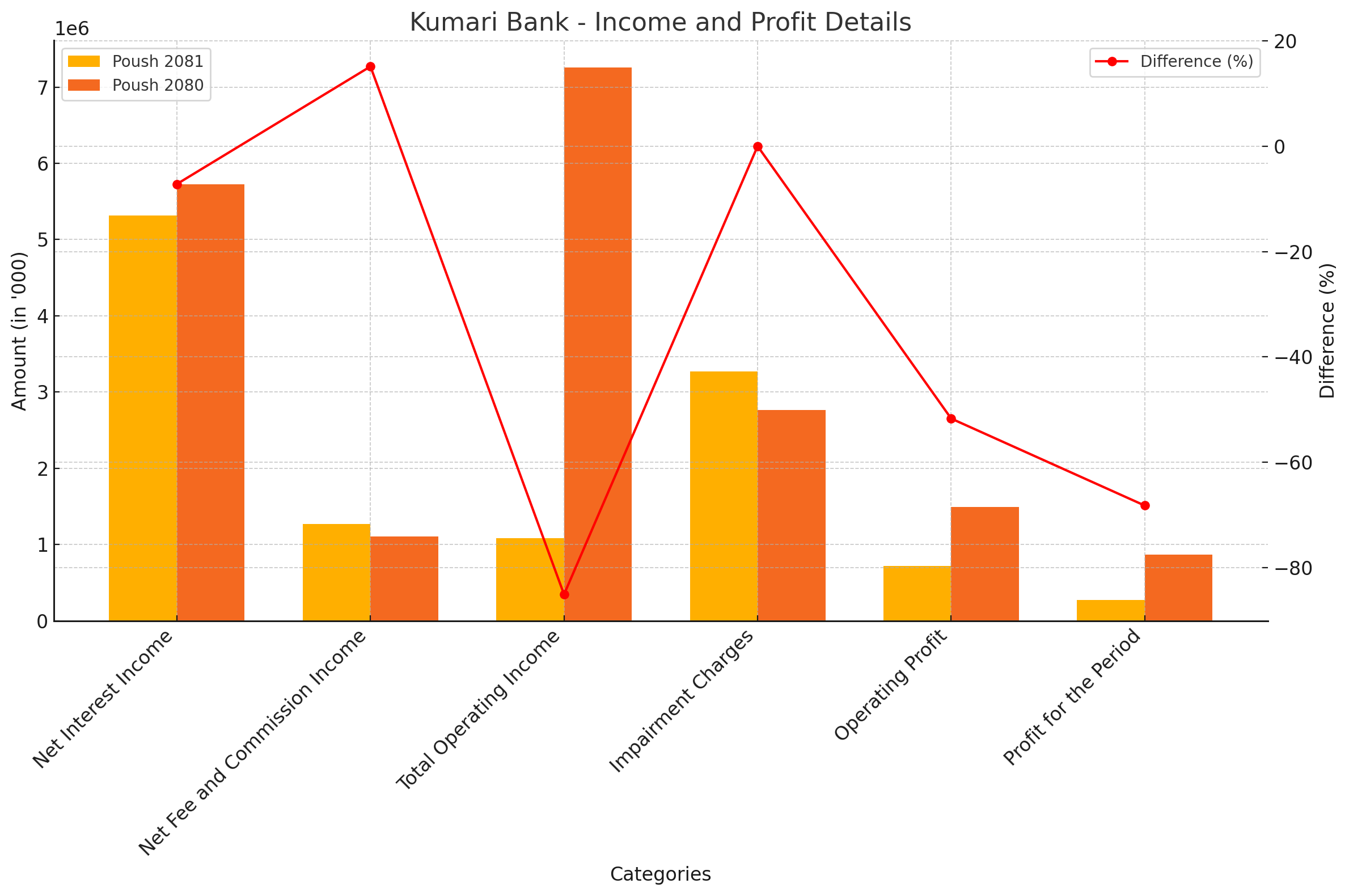

पुस मसान्तसम्ममा बैंकले २७ करोड ५७ लाख रुपैयाँ मात्र खुद नाफा कमाएको छ, जुन अघिल्लो वर्षको सोही अवधिको ८६ करोड ७२ लाख रुपैयाँभन्दा ६८.२० प्रतिशतले कम हो। यो गिरावट बैंकको वित्तीय प्रदर्शनमा गम्भीर असर परेको संकेत हो।

खुद ब्याज आम्दानीमा कमी: बैंकको खुद ब्याज आम्दानी गत वर्षको तुलनामा ७.१९ प्रतिशतले घटेर ५ अर्ब ३१ करोड रुपैयाँमा सीमित भएको छ। यो कमी ब्याजदरमा आएको प्रतिस्पर्धात्मक दबाब र लगानीको घट्दो प्रभावकारिताका कारण भएको हुनसक्छ।

इम्पेरमेन्ट चार्जमा वृद्धि: समीक्षाको अवधिमा इम्पेरमेन्ट चार्ज २ अर्ब ७६ करोड रुपैयाँबाट बढेर ३ अर्ब २७ करोड रुपैयाँ पुगेको छ। यो वृद्धि ऋण पुनरावलोकन तथा खराब कर्जाको व्यवस्थापनमा भएको कठिनाइका कारण भएको हुनसक्छ।

कुल सञ्चालन आम्दानीमा ठूलो गिरावट: बैंकको कुल सञ्चालन आम्दानी ८५.०६ प्रतिशतले घटेर १ अर्ब ८३ लाख रुपैयाँमा सीमित भएको छ। यो गिरावट बैंकको सञ्चालन खर्च र ब्याज आम्दानीबीचको असन्तुलनको कारण भएको देखिन्छ।

खुद फि तथा कमिशन आम्दानीमा वृद्धि: यो आम्दानी १५.१२ प्रतिशतले वृद्धि भई १ अर्ब २७ करोड रुपैयाँ पुगेको छ। बैंकको डिजिटल सेवा तथा ग्राहक सेवाको विस्तारले यो वृद्धि ल्याएको अनुमान गर्न सकिन्छ।

निक्षेप संकलनमा सुधार: बैंकले पुस मसान्तसम्ममा ३ खर्ब ४८ अर्ब रुपैयाँ निक्षेप संकलन गरेको छ, जुन गत वर्षको तुलनामा ४.६९ प्रतिशतले वृद्धि हो।

चुक्ता पूँजी: बैंकको चुक्ता पूँजी २६ अर्ब २२ करोड रुपैयाँ रहेको छ।

जगेडा कोष: पुस मसान्तसम्ममा ८ अर्ब ७८ करोड रुपैयाँ जगेडा कोषमा सञ्चित छ।

कर्जा प्रवाह: बैंकले २ खर्ब ७५ अर्ब रुपैयाँ कर्जा प्रवाह गरेको छ, जुन गत वर्षको तुलनामा २.४८ प्रतिशतले वृद्धि हो।

प्रति शेयर आम्दानी (EPS): यो आम्दानी ६ रुपैयाँ ६१ पैसाबाट घटेर २ रुपैयाँ १० पैसामा सीमित भएको छ।

प्रति शेयर नेटवर्थ: बैंकको प्रति शेयर नेटवर्थ १३३ रुपैयाँ ५१ पैसा छ।

बैंकको आधार दर (Base Rate) १०.२८ प्रतिशतबाट घटेर ७.१४ प्रतिशतमा आएको छ। यसले बैंकको कर्जा लगानीमा न्यूनतम ब्याजदर घटाएको देखाउँछ। त्यस्तै, ब्याजदरको अन्तर (Interest Rate Spread) ३.९८ प्रतिशतबाट घटेर ३.५१ प्रतिशतमा सीमित भएको छ।

कुमारी बैंकले हाल देखिएको चुनौतीपूर्ण अवस्थालाई सुधार गर्न निम्न रणनीतिहरू अपनाउन सक्छ:

डिजिटल बैंकिङको प्रवर्द्धन: डिजिटल बैंकिङ सेवामा लगानी गर्दै ग्राहकको पहुँच र सन्तुष्टिलाई बढावा दिनु आवश्यक छ।

खर्च व्यवस्थापन: सञ्चालन खर्चलाई थप प्रभावकारी बनाउँदै न्यूनतम इम्पेरमेन्ट चार्जको रणनीति बनाउनुपर्छ।

नयाँ लगानी अवसरहरू पहिचान: उदीयमान क्षेत्रहरूमा कर्जा प्रवाह बढाउँदै ब्याज आम्दानी सुधार गर्न सकिन्छ।

जोखिम व्यवस्थापनमा सुधार: खराब कर्जाको व्यवस्थापनलाई प्राथमिकतामा राख्दै जोखिम न्यूनीकरणका उपायहरू अपनाउनुपर्छ।

कुमारी बैंकको पछिल्लो वित्तीय विवरणले बैंकिङ क्षेत्रका लागि चुनौतीका साथै अवसरहरूको मिश्रण प्रस्तुत गर्दछ। बैंकले आफ्ना सकारात्मक पक्षलाई सुदृढ गर्दै वित्तीय स्थिरताका लागि दीर्घकालीन रणनीति अपनाउनुपर्छ।

Kumari Bank Limited has published its unaudited financial report for the second quarter of the fiscal year 2081/82. The report reveals a significant decline in the bank's net profit, along with other key financial indicators, highlighting the challenges faced during the review period.

As of Poush 2081, the bank has reported a net profit of NPR 275.7 million, a massive 68.20% drop compared to NPR 867.2 million in the corresponding period of the previous fiscal year. This steep decline is attributed to a combination of reduced interest income and increased impairment charges.

Drop in Net Interest Income: The bank’s net interest income decreased by 7.19%, falling to NPR 5.31 billion from NPR 5.73 billion. This can be attributed to competitive pressure on interest rates and reduced profitability on loans and advances.

Increase in Impairment Charges: Impairment charges surged from NPR 2.77 billion to NPR 3.27 billion, indicating challenges in managing bad loans and credit risks.

Significant Decline in Operating Income: The total operating income fell by a staggering 85.06%, settling at NPR 1.08 billion. This decline underscores inefficiencies in operational management and the widening gap between expenses and income.

Despite the challenges, the bank has achieved some positive outcomes:

Growth in Fee and Commission Income: Fee and commission income increased by 15.12%, reaching NPR 1.27 billion. This indicates growth in customer engagement and the expansion of non-interest revenue streams.

Improvement in Deposits: The bank’s total customer deposits grew by 4.69%, reaching NPR 348.7 billion by the end of Poush 2081.

Paid-Up Capital: The bank’s paid-up capital stands at NPR 26.22 billion.

Reserves and Surplus: The reserve fund has increased to NPR 8.78 billion.

Loans and Advances: Total loans and advances reached NPR 275.09 billion, up by 2.48% from the previous year.

Earnings Per Share (EPS): EPS dropped from NPR 6.61 to NPR 2.10, reflecting reduced profitability.

Net Worth Per Share: The bank’s net worth per share stands at NPR 133.51.

Decline in Financial Ratios

The bank’s base rate decreased from 10.28% to 7.14%, which indicates a reduction in the minimum lending rate. Similarly, the interest rate spread narrowed from 3.98% to 3.51%, impacting the bank’s margin on loans and deposits.

Future Strategies and Areas for Improvement

To address these challenges and improve its financial performance, Kumari Bank can adopt the following strategies:

Focus on Digital Banking: Investing in digital banking infrastructure to enhance customer accessibility and satisfaction.

Cost Management: Streamlining operational costs and focusing on reducing impairment charges to improve profitability.

Explore New Investment Opportunities: Increasing lending in emerging sectors to diversify income sources and improve interest income.

Strengthen Risk Management: Prioritizing the management of non-performing loans and implementing measures to mitigate credit risks.

Kumari Bank’s latest financial report highlights both challenges and opportunities in the banking sector. The bank needs to leverage its strengths, such as improved fee and commission income, while addressing areas of concern like impairment charges and declining profitability. A robust long-term strategy will be crucial for ensuring financial stability and sustainable growth.