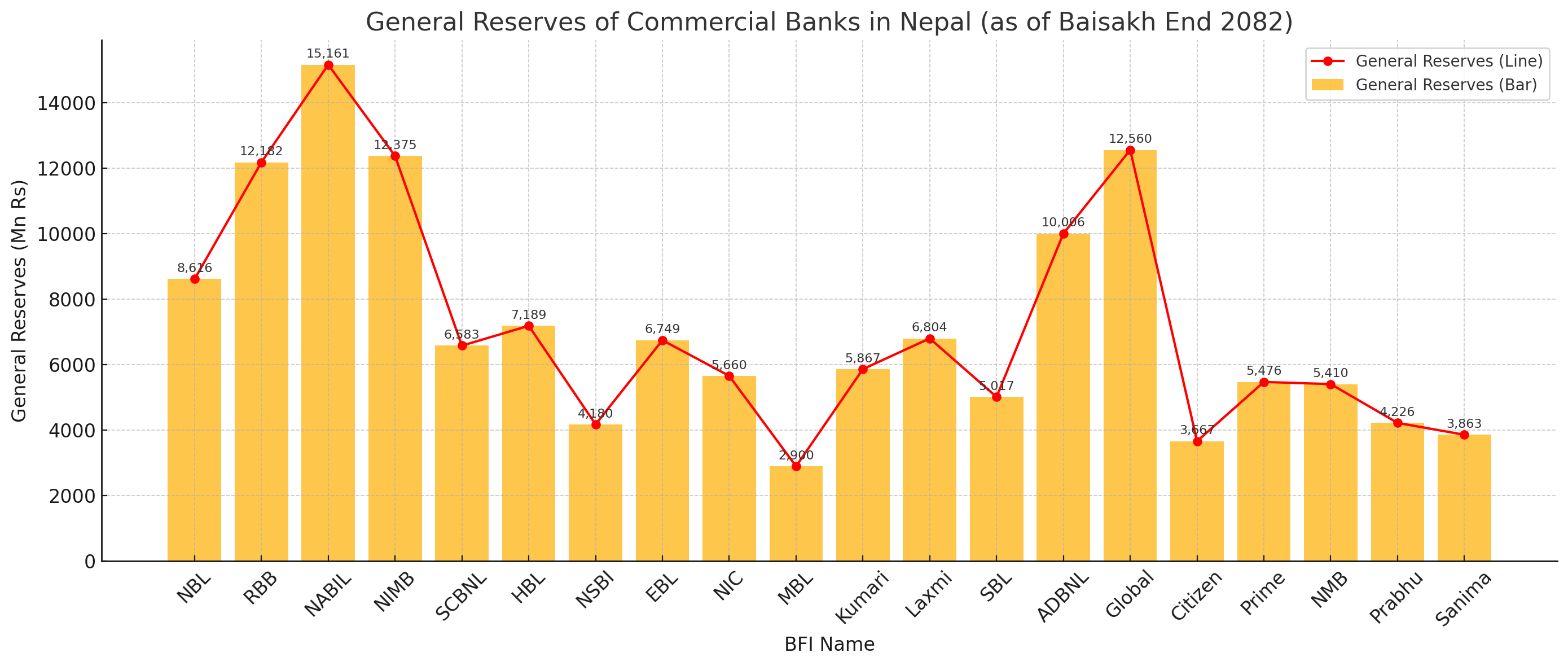

नेपाल राष्ट्र बैंकको नियामकीय निर्देशिकाअनुसार वाणिज्य बैंकहरूले आवधिक रूपमा आन्तरिक नाफाबाट सञ्चित कोष संकलन गर्दै आएका छन्। यसै अन्तर्गत, २०८२ सालको बैशाख मसान्तसम्मको सामान्य जगेडा (General Reserve) विवरण अनुसार नबिल बैंक सबैभन्दा अग्रस्थानमा देखिएको छ।

शीर्ष ५ बैंकहरू (सामान्य जगेडाको आधारमा):

स्थान | बैंकको नाम | सामान्य जगेडा (रु. करोड) |

|---|

१ | नबिल बैंक | १५,१६१.३१ |

२ | ग्लोबल आइएमई बैंक | १२,५५९.६५ |

३ | नेपाल इन्भेस्टमेन्ट मेगा बैंक (NIMB) | १२,३७५.१५ |

४ | राष्ट्र बैंक (RBB) | १२,१८२.१० |

५ | कृषि विकास बैंक (ADBNL) | १०,००५.७५ |

यी बैंकहरूले विगत वर्षहरूमा उच्च नाफा संकलन, नियमन अनुरूपको जगेडा राख्ने नीतिको पालना, र गाभ्ने प्रक्रियाबाट सुदृढ आन्तरिक पूँजी बनाएका छन्।

अन्य उल्लेखनीय बैंकहरूको अवस्था:

स्ट्यान्डर्ड चार्टर्ड बैंक – रु. ६५८३.३१ करोड

हिमालयन बैंक (HBL) – रु. ७१८९.४५ करोड

लक्ष्मी बैंक – रु. ६८०४.२२ करोड

ईभेरेष्ट बैंक – रु. ६७४८.९९ करोड

कुमारी बैंक – रु. ५८६७.०४ करोड

कम जगेडा भएका बैंकहरू:

बैंक | सामान्य जगेडा (रु. करोड) |

|---|

MBL (माछापुच्छ्रे) | २८९९.५४ |

Citizen Bank | ३६६६.८३ |

Sanima Bank | ३८६३.०० |

Prabhu Bank | ४२२५.५४ |

NSBI Bank | ४१८०.५० |

यी बैंकहरूले तुलनात्मक रूपमा कम जगेडा राखेका छन्, जुन नाफाको स्तर, जगेडा छुट्याउने नीति, र ब्याज तथा खर्च संरचनामा निर्भर रहेको देखिन्छ।

सामान्य जगेडा कुनै पनि बैंकको आन्तरिक वित्तीय सुरक्षा कवच हो, जसले असामान्य घाटा वा जोखिम आइपर्दा तत्कालीन समाधान प्रदान गर्छ। नेपाल राष्ट्र बैंकले यसलाई न्यूनतम प्रतिशतमा छुट्याउन निर्देशन दिने गर्दछ।

उच्च सामान्य जगेडा भएका बैंकहरू बजारमा स्थायित्व र विश्वसनीयता कायम गर्न सक्षम देखिन्छन्। यस्ता बैंकहरूले विस्तारित ऋण कारोबार, अन्तर्राष्ट्रिय साझेदारी, र विपद् व्यवस्थापनमा अग्रसरता लिन सक्छन्।

कम जगेडा भएका बैंकहरू भविष्यमा जोखिम व्यवस्थापन चुनौती, नियम उल्लंघनको सम्भावना, र ब्याज दरमा अस्थिरता जस्ता समस्यामा पर्ने सम्भावना रहन्छ।

२०८२ बैशाख मसान्तसम्मको तथ्यांकले देखाउँछ कि वाणिज्य बैंकहरूको सामान्य जगेडा स्तर स्पष्ट रूपमा अलग–अलग छ। जसले बैंकहरूको जोखिम वहन क्षमता, नाफा सञ्चालन नीति, र नियामकीय अनुरूपता प्रस्ट पार्छ। नीति निर्माताका लागि यो तथ्यांक आगामी वर्षको बैंक मूल्यांकन र वर्गीकरण गर्न उपयोगी हुनेछ।

According to data published for the period ending Baisakh 2082, Nabil Bank leads Nepal's commercial banking sector in terms of general reserves, with a total of Rs. 15.16 billion. General reserves reflect a bank’s internal financial buffer, accumulated primarily from retained earnings to safeguard against future risks.

Top 5 Banks by General Reserves:

Rank | Bank Name | General Reserves (Million Rs.) |

|---|

1 | Nabil Bank | 15,161.31 |

2 | Global IME Bank | 12,559.65 |

3 | Nepal Investment Mega Bank | 12,375.15 |

4 | Rastriya Banijya Bank (RBB) | 12,182.10 |

5 | Agricultural Development Bank | 10,005.75 |

These banks have benefited from strong profit retention, robust earnings, and favorable cost control policies. Mergers and efficient capital management have also contributed to their strengthened reserve base.

Notable Mid-tier Banks:

Standard Chartered Bank Nepal – Rs. 6,583.31 million

Himalayan Bank – Rs. 7,189.45 million

Laxmi Bank – Rs. 6,804.22 million

Everest Bank – Rs. 6,748.99 million

Kumari Bank – Rs. 5,867.04 million

These banks maintain reasonably healthy reserves, indicating prudent management of retained earnings.

Banks with Lower General Reserves:

Bank | General Reserves (Million Rs.) |

|---|

Machhapuchchhre Bank (MBL) | 2,899.54 |

Citizen Bank | 3,666.83 |

Sanima Bank | 3,863.00 |

Prabhu Bank | 4,225.54 |

NSBI Bank | 4,180.50 |

These banks reflect comparatively limited reserve accumulation, possibly due to lower profitability, higher operating expenses, or conservative reserve allocation policies.

General reserves act as a financial shield, enabling banks to absorb losses during economic stress or market downturns. The Nepal Rastra Bank (NRB) mandates commercial banks to allocate a portion of profits to these reserves annually.

Higher reserves signal greater risk-bearing capacity, improved creditworthiness, and better compliance with regulatory requirements. Banks like Nabil and Global IME are in a stronger position to finance large projects and handle shocks.

Banks with smaller reserves may face higher vulnerability during liquidity crunches or unexpected losses. It also reflects limited reinvestment of profits, which can hinder long-term capital expansion.

As of Baisakh end 2082, the disparity in general reserves across Nepal’s commercial banks illustrates a clear distinction in profitability, capital discipline, and financial resilience. Regulatory bodies and investors will likely monitor these metrics closely in evaluating bank health and risk exposure going forward.