नेपालको बैंकिङ क्षेत्रले पछिल्लो डेढ वर्षमा ब्याजदरमा ठूलो गिरावट अनुभव गरेको छ। तलबेच ब्याजदर, ऋण दिने ब्याजदर र आधार दर सबैमा निरन्तर कमी आएको छ, जसले ऋणीलाई अवसर प्रदान गरेको छ भने बचतकर्तालाई आफ्नो बचत रणनीति पुनर्विचार गर्न बाध्य पारेको छ। यी परिवर्तनहरूले घरपरिवार, व्यवसाय, र लगानीकर्तालाई फरक ढंगले असर पारेको छ।

ब्याजदरको प्रवृत्ति

बचत ब्याजदर:

तलबेच बचत ब्याजदर, जसले बचतमा प्रतिफललाई निर्धारण गर्छ, आर्थिक वर्ष २०८०/८१ को साउन महिनामा ८.००% बाट सुरु भएर असार महिनासम्म ५.७७% मा झर्यो। चालू आर्थिक वर्ष २०८१/८२ मा यो दर घट्दै गइरहेको छ, मंसिर महिनामा ४.७८% सम्म पुगेको छ। यो गिरावटले बैंकिङ क्षेत्रमा तरलताको अवस्थामा सुधार भएको संकेत गर्दछ। वित्तीय संस्थाहरूले उच्च ब्याजदरमा बचत आकर्षित गर्न आवश्यक देखेका छैनन्, जसले बचतकर्तालाई प्रत्यक्ष असर गरेको छ।

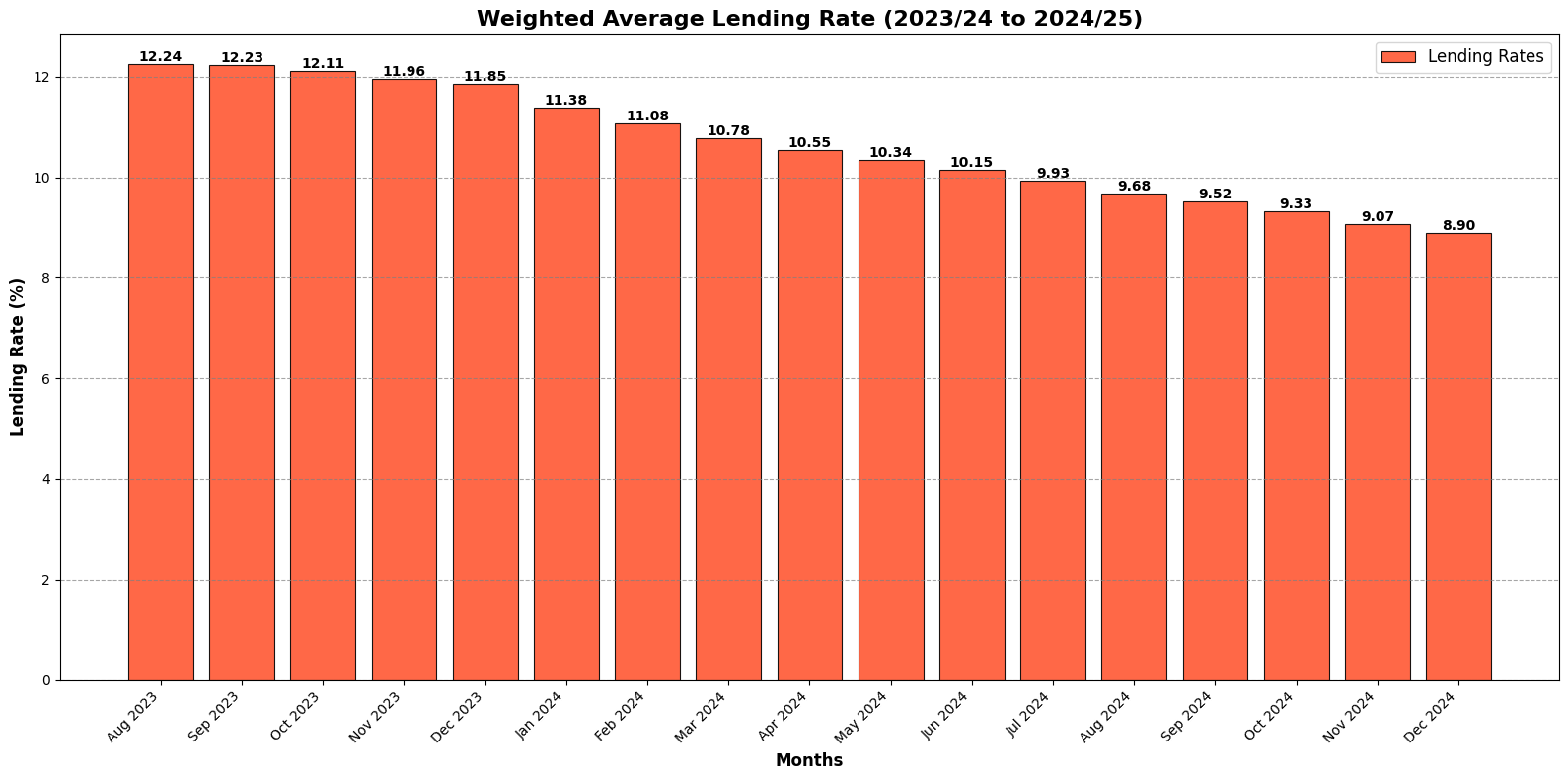

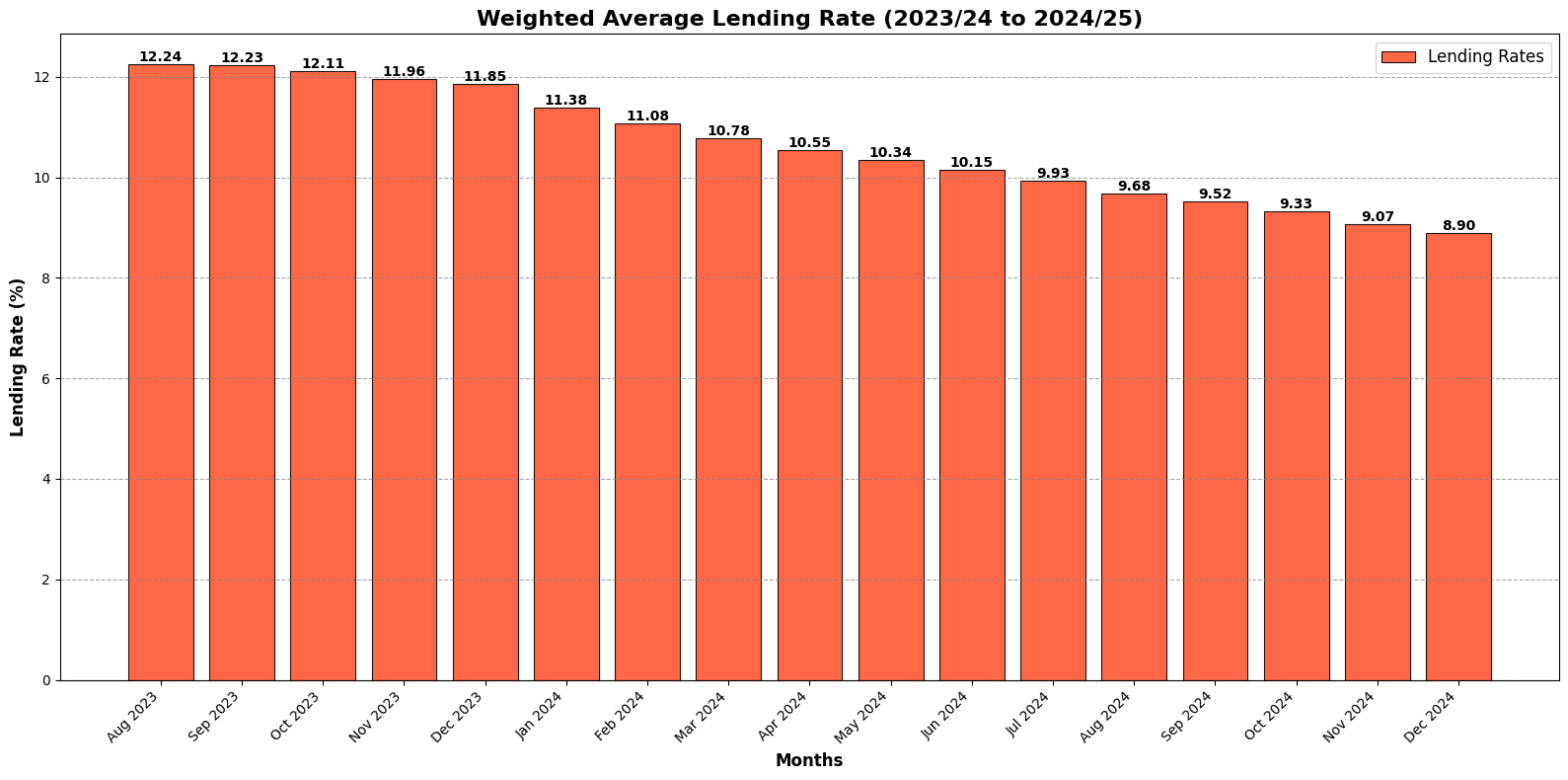

ऋण दिने ब्याजदर:

ऋणीहरूले ब्याजदरमा गिरावटको प्रत्यक्ष लाभ लिएका छन्। २०८० साउन महिनामा तलबेच ऋण दिने ब्याजदर १२.२४% थियो, जुन २०८१ असार महिनासम्म ९.९३% मा झर्यो। मंसिर महिनामा यो दर ८.९०% मा झरेको छ, जसले व्यवसाय र व्यक्तिगत ऋणलाई थप सुलभ बनाएको छ। यो कमीले व्यवसायीहरूलाई नयाँ परियोजना सुरु गर्न र विस्तार गर्न प्रोत्साहित गर्नेछ।

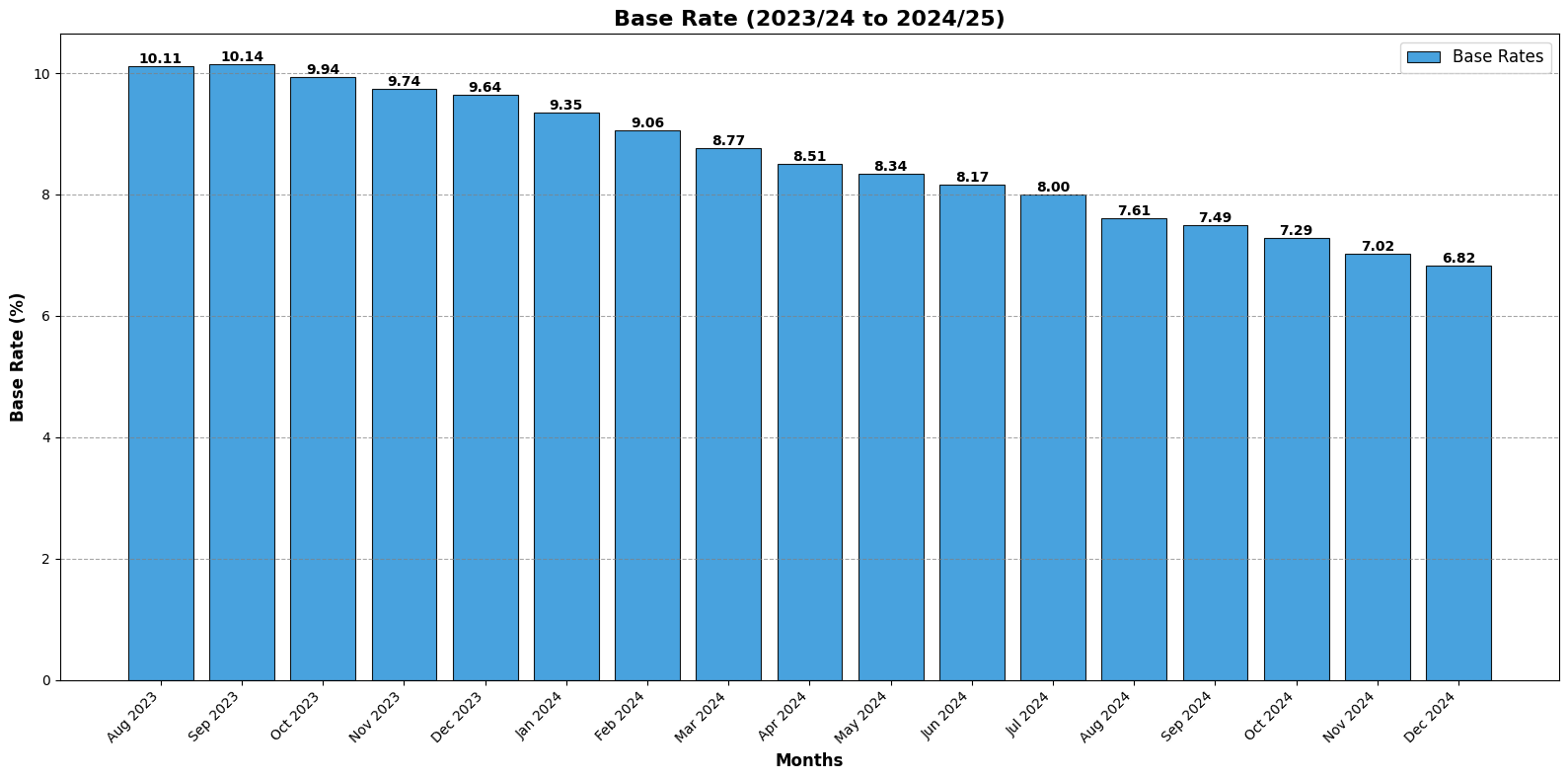

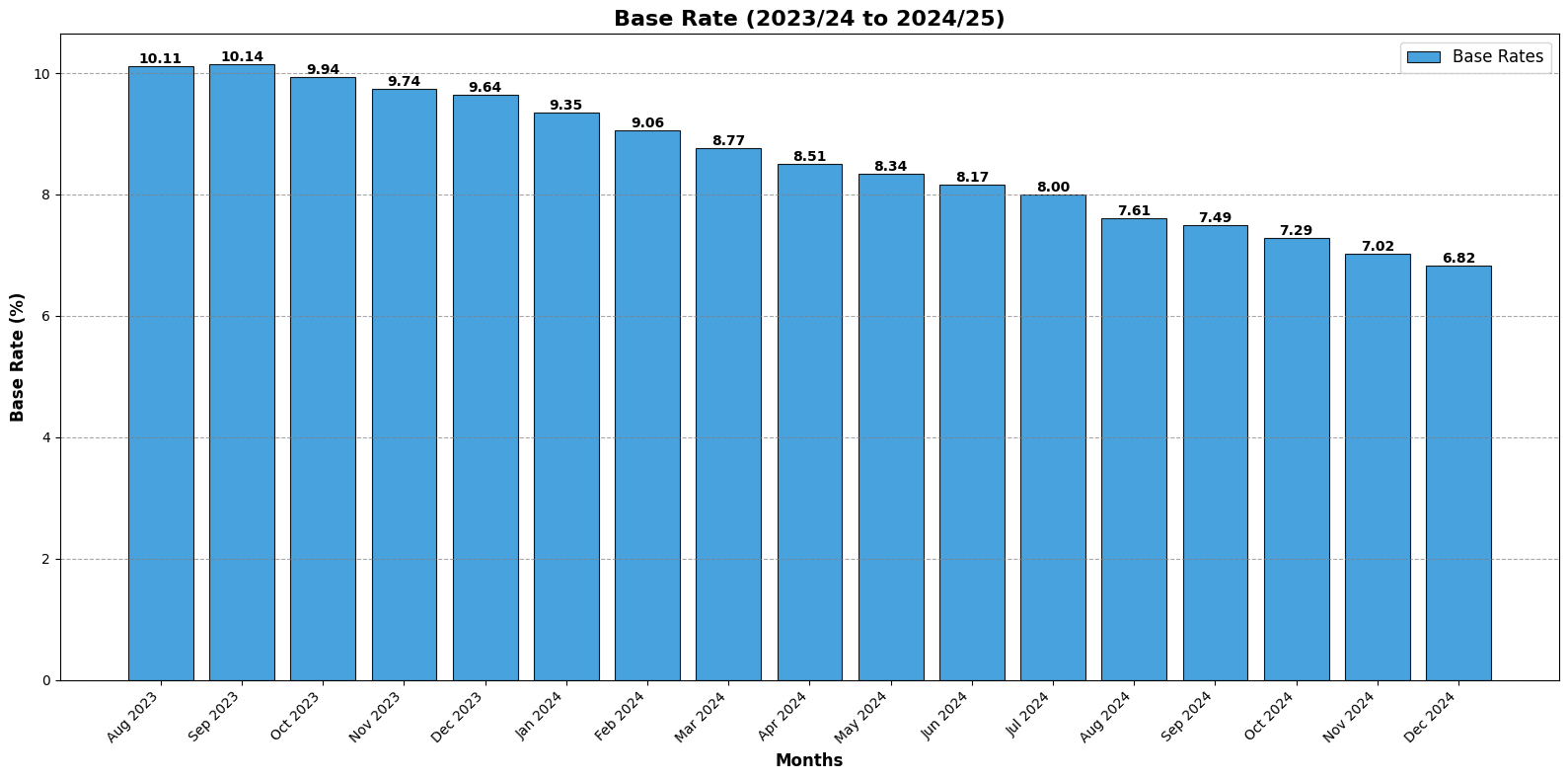

आधार दर:

आधार दर, जुन ऋण दिने ब्याजदर निर्धारण गर्न प्रयोग गरिन्छ, १०.११% बाट सुरु भएर २०८१ असार महिनासम्म ८.००% मा झर्यो। मंसिर महिनामा यो दर ६.८२% मा झरेको छ। आधार दरको गिरावटले बैंकहरूले कम मार्जिनमा ऋण दिन इच्छुक रहेको संकेत गर्दछ, जसले आर्थिक गतिविधि बढाउन भूमिका खेल्न सक्छ।

ब्याजदर घट्ने कारणहरू

१. मौद्रिक नीति परिवर्तन: नेपाल राष्ट्र बैंकले मौद्रिक नीति सहज बनाउँदै तरलताको अभाव हटाउन र आर्थिक वृद्धि प्रोत्साहित गर्न काम गरिरहेको छ। नीतिगत ब्याजदर घटाएर र तरलता प्रवाह कायम राखेर बैंकहरूलाई ब्याजदर घटाउने ठाउँ दिएको छ।

२. तरलताको सुधार: विगत वर्षमा बैंकिङ क्षेत्रमा तरलताको स्तरमा सुधार आएको छ, जसले बैंकहरूलाई उच्च ब्याजदरमा बचत आकर्षित गर्न आवश्यक छैन।

३. आर्थिक सुधार: विश्वव्यापी र स्थानीय चुनौतीबाट अर्थतन्त्र उकास्दै जाँदा बैंकिङ क्षेत्रमा क्रेडिट विस्तार र दर घटाउने प्रयास जारी छ।

सरोकारवालाहरूमा प्रभाव

ऋणीहरू:

ब्याजदरमा गिरावटले व्यवसाय र व्यक्तिगत ऋण सुलभ बनाएको छ। कम आधार दरले पारदर्शी ऋण मूल्य निर्धारणलाई प्रोत्साहन गरेको छ, जसले ऋणीलाई थप फाइदा पुर्याउँछ।

बचतकर्ता:

बचत ब्याजदरमा आएको कमीले बचतमा निर्भर घरपरिवार र सेवानिवृत्त व्यक्तिलाई चुनौती दिएको छ। यसले उनीहरूलाई शेयर बजार, रियल स्टेट, वा अन्य वैकल्पिक लगानीतर्फ आकर्षित गर्न सक्छ।

व्यवसाय:

कम ब्याजदरले व्यवसायलाई पुँजी लागत कम गर्न र नयाँ परियोजना तथा विस्तारमा लगानी गर्न मद्दत पुर्याउनेछ। जलविद्युत्, निर्माण, र कृषि क्षेत्रले यसबाट ठूलो फाइदा लिन सक्ने सम्भावना छ।

आर्थिक प्रभाव

१. लगानी प्रोत्साहन: कम ब्याजदरले लगानीलाई तीव्र बनाउन मद्दत गर्नेछ। व्यवसायहरूले क्षमता विस्तार र नयाँ परियोजना सुरु गर्न सक्छन्, जसले GDP वृद्धि बढाउन सहयोग गर्नेछ।

२. उपभोक्ता खर्चमा वृद्धि: सस्तो ऋणले घरपरिवारलाई ठूलो खर्च गर्ने बस्तुहरू, जस्तै घर-जग्गा र गाडी खरिद गर्न प्रोत्साहित गर्नेछ।

३. मूल्यवृद्धिको सम्भावना: ब्याजदरमा गिरावटले ऋण विस्तारलाई तीव्र बनाउँदा मूल्यवृद्धिको दबाब सिर्जना हुन सक्छ। यसलाई नियन्त्रण गर्न राष्ट्र बैंकले सतर्कता अपनाउनु पर्नेछ।

४. लगानी प्राथमिकतामा परिवर्तन: बचतकर्ताहरू परम्परागत बैंक बचतबाट बाहिरिएर उच्च प्रतिफल दिने लगानीतर्फ मोडिन सक्छन्, जसले पूँजी बजारलाई गहिरो बनाउनेछ।

२०८१/८२ का लागि दृष्टिकोण

ब्याजदरमा गिरावटले आर्थिक वृद्धिका लागि नयाँ सम्भावना प्रदान गरेको छ। तर, यो प्रवृत्तिले स्थायित्व कायम गर्नका लागि राष्ट्र बैंक र बैंकिङ क्षेत्रले मिलेर काम गर्नु आवश्यक छ। कम ब्याजदरले आर्थिक गतिविधिलाई प्रोत्साहित गर्ने भए पनि मूल्यवृद्धि र तरलता व्यवस्थापनमा ध्यान दिनुपर्नेछ।

आगामी महिनाहरूमा ब्याजदरको गिरावटले नेपालका वित्तीय र आर्थिक परिदृश्यलाई कसरी परिवर्तन गर्छ भन्ने हेर्न बाँकी छ। ऋण सुलभता र लगानी प्रवर्द्धनले दीर्घकालीन आर्थिक स्थिरता कायम गर्न सहयोग गर्नेछ।