सिद्धार्थ बैंकको नाफामा भारी गिरावट, इम्पेरमेन्ट चार्ज मुख्य कारणSignificant Decline in Siddhartha Bank's Profit: Impairment Charge as the Key Reason

सिद्धार्थ बैंक लिमिटेडले आर्थिक वर्ष २०८१ को दोस्रो त्रैमाससम्मको वित्तीय विवरण सार्वजनिक गरेको छ। विवरणअनुसार बैंकको नाफा, सञ्चालन मुनाफा, र प्रतिशेयर आम्दानी (EPS) जस्ता मुख्य वित्तीय सूचकहरूमा उल्लेखनीय गिरावट आएको छ। बैंकले इम्पेरमेन्ट चार्जको उच्च वृद्धिलाई नाफा घट्नुको मुख्य कारण ठहराएको छ।

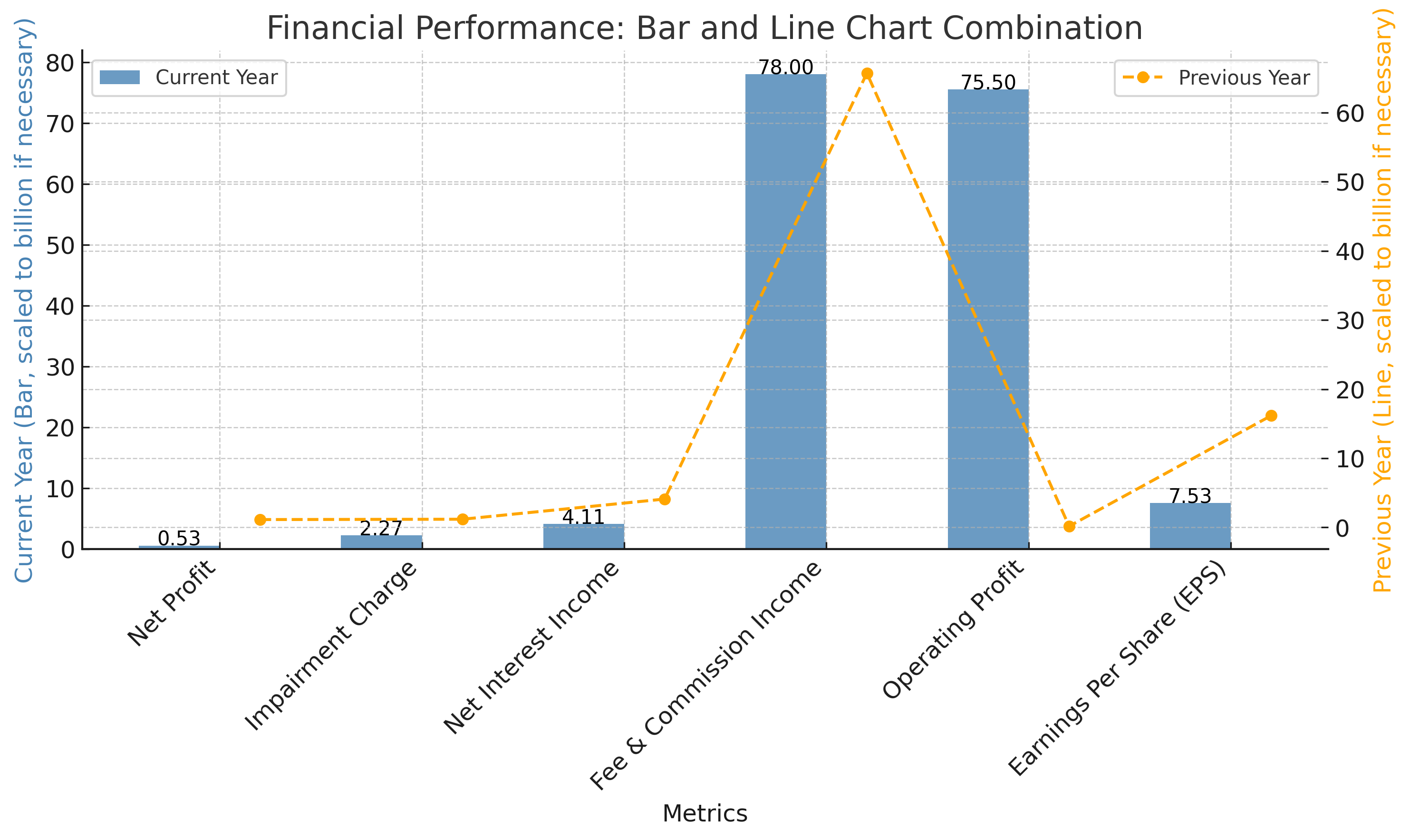

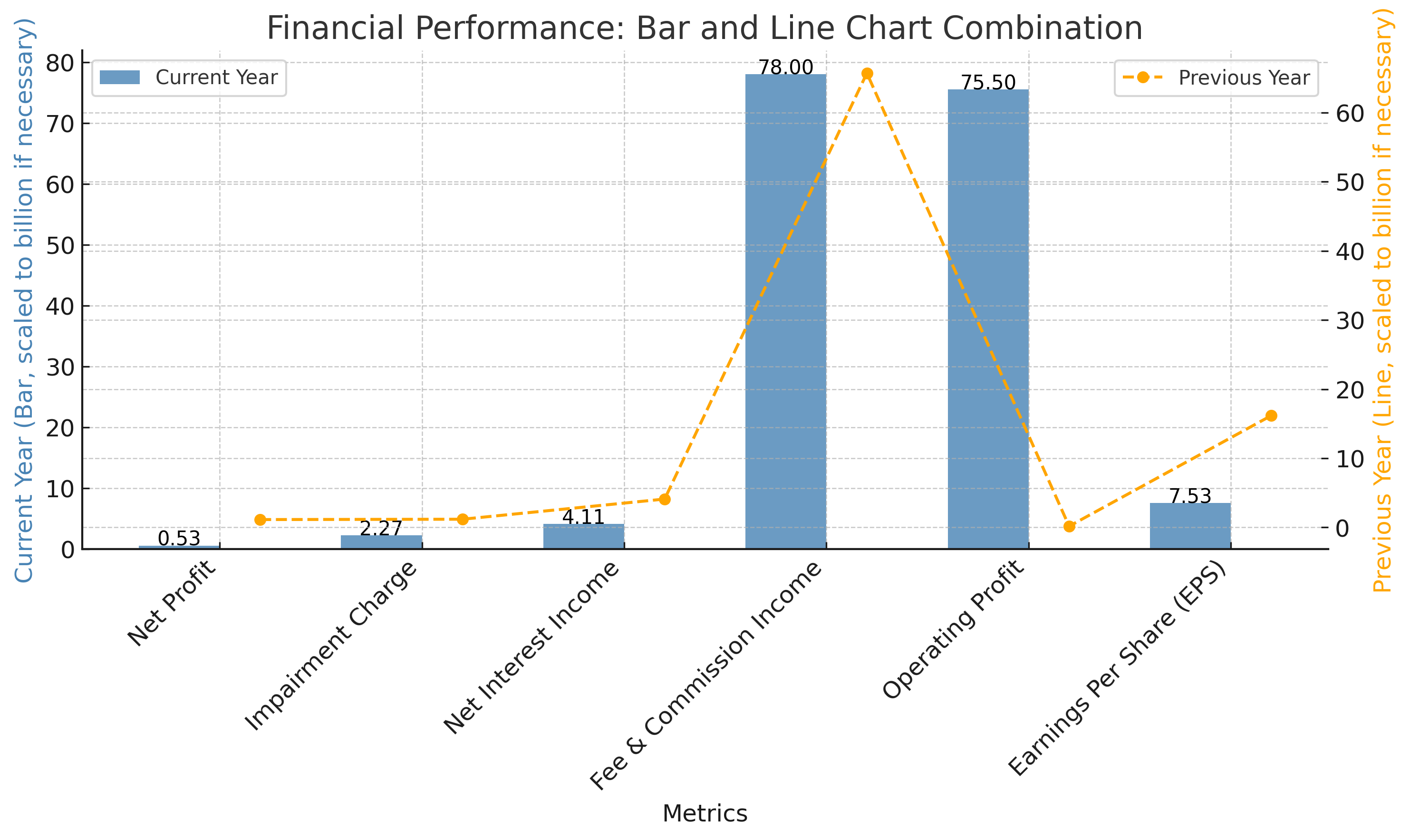

खुद नाफा ५३.३६ प्रतिशतले घट्यो

गत वर्षको पुस मसान्तसम्म १ अर्ब १३ करोड ६८ लाख रुपैयाँ खुद नाफा कमाएको बैंकले चालु आर्थिक वर्षमा ५३ करोड २ लाख रुपैयाँ मात्र नाफा आर्जन गर्न सकेको छ। यो ५३.३६ प्रतिशतको गिरावट हो।

बैंकको इम्पेरमेन्ट चार्ज गत वर्षको १ अर्ब १८ करोड रुपैयाँबाट २ अर्ब २६ करोड ५१ लाख रुपैयाँ पुगेको छ, जसले नाफामा ठूलो असर पुर्याएको छ।

ब्याज र कमिशन आम्दानीमा सुधार

सकारात्मक पक्षका रूपमा, बैंकले:

खुद ब्याज आम्दानी ०.३० प्रतिशतले वृद्धि गरी ४ अर्ब ११ करोड ६ लाख रुपैयाँ पुर्याएको छ।

फि तथा कमिशन आम्दानी १८.६८ प्रतिशतले बढेर ७ करोड ८० लाख रुपैयाँ पुर्याएको छ।

यद्यपि, यी सुधारहरूले कुल नाफामा पर्याप्त प्रभाव पार्न सकेनन्।

सञ्चालन मुनाफामा भारी गिरावट

बैंकको कुल सञ्चालन आम्दानी ५.२७ अर्ब रुपैयाँ रहेको छ, जुन गत वर्षको तुलनामा ४.४० प्रतिशतको वृद्धि हो। तर, इम्पेरमेन्ट चार्ज बढेकाले बैंकको सञ्चालन मुनाफा ५४.३७ प्रतिशतले घटेर ७ करोड ५५ लाख रुपैयाँमा सीमित भएको छ।

EPS मा गिरावट

प्रतिशेयर आम्दानी (EPS) गत वर्षको १६.१८ बाट घटेर ७.५३ मा झरेको छ, जसले लगानीकर्तालाई चिन्तित बनाएको छ।

पूँजी संरचना र वित्तीय स्थिति

चुक्ता पूँजी: १४ अर्ब ८ करोड रुपैयाँ।

जगेडा कोष: १३ अर्ब ८९ करोड रुपैयाँ।

वितरणयोग्य मुनाफा: ३६ करोड १९ लाख रुपैयाँ ऋणात्मक।

क्रेडिट टू डिपोजिट अनुपात (CD Ratio): ८३.७८ प्रतिशत।

अन्य प्रमुख सूचकहरू

PE अनुपात: ३९.२१।

बेस रेट: ६.९३।

पूँजी कोष–जोखिम भारित सम्पत्ति अनुपात: ११.१९।

नन परफर्मिंग लोन (NPL): ४.५० प्रतिशत।

सिद्धार्थ बैंकको वित्तीय सूचकहरूले उच्च इम्पेरमेन्ट चार्ज, सञ्चालन खर्चको वृद्धि, र ऋणात्मक वितरणयोग्य मुनाफाका कारण आर्थिक दबाबको संकेत गरेका छन्। यद्यपि, खुद ब्याज आम्दानी र सञ्चालन आम्दानीको सुधार सकारात्मक पक्ष हुन्, बैंकले निकट भविष्यमा इम्पेरमेन्ट चार्ज व्यवस्थापन गर्दै नाफा सुधारमा ध्यान दिनुपर्ने देखिन्छ।

Siddhartha Bank Limited has published its financial report for the second quarter of FY 2081. According to the report, the bank has experienced a significant decline in key financial indicators such as net profit, operating profit, and earnings per share (EPS). The primary reason cited for this decline is the substantial increase in impairment charges.

Net Profit Drops by 53.36%

As of the second quarter of the previous fiscal year, the bank had earned a net profit of NPR 1.13 billion. However, by the same period this fiscal year, the net profit has dropped to NPR 530.2 million, marking a 53.36% decline.

The bank’s impairment charge has surged from NPR 1.18 billion last year to NPR 2.27 billion, significantly impacting its profitability.

Improvement in Interest and Commission Income

On the positive side, the bank has reported:

Net interest income increased by 0.30%, reaching NPR 4.11 billion.

Fee and commission income grew by 18.68%, reaching NPR 78 million.

Despite these improvements, they were not sufficient to offset the impact of rising impairment charges.

Sharp Decline in Operating Profit

The bank’s total operating income rose by 4.40%, reaching NPR 5.27 billion. However, due to higher impairment charges, the operating profit plunged by 54.37%, limiting it to NPR 75.5 million.

EPS Declines

The bank’s Earnings Per Share (EPS) dropped from 16.18 last year to 7.53, a decline of NPR 8.65, reflecting a notable reduction in returns for shareholders.

Capital Structure and Financial Position

Paid-up capital: NPR 14.08 billion.

Reserve fund: NPR 13.89 billion.

Distributable profit: Negative NPR 361.9 million.

Credit-to-Deposit Ratio (CD Ratio): 83.78%.

Other Key Indicators

Price-to-Earnings (PE) Ratio: 39.21.

Base rate: 6.93%.

Capital Adequacy Ratio: 11.19%.

Non-Performing Loan (NPL) Ratio: 4.50%.

Siddhartha Bank's financial indicators reveal the impact of higher impairment charges, increased operating expenses, and negative distributable profit. However, the improvement in net interest income and operating income serves as a positive sign, The bank must focus on managing its impairment charges and improving profitability in the near future to stabilize its financial performance.