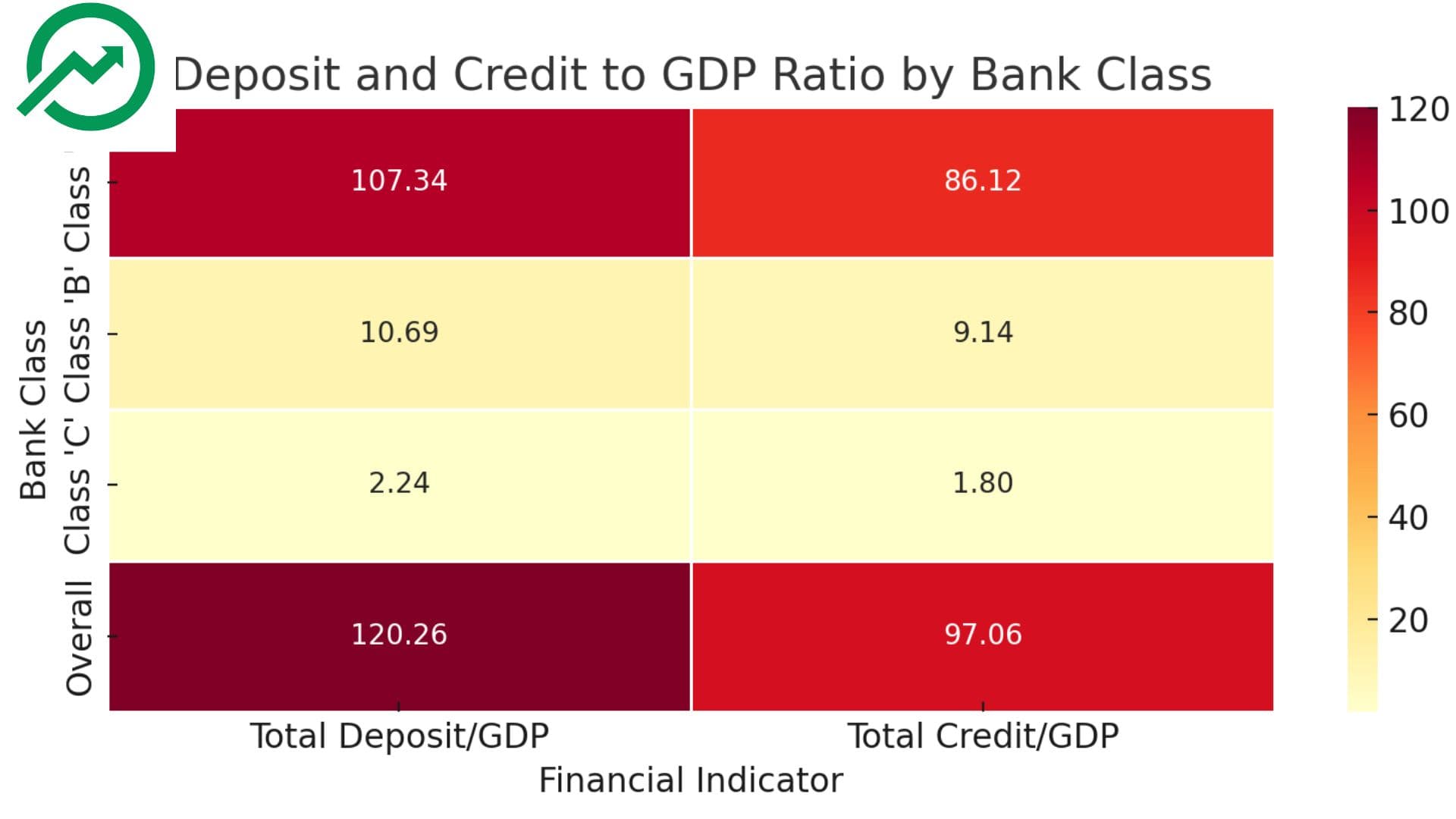

नेपालको बैंकिङ प्रणाली राष्ट्रको अर्थतन्त्रसँग कसरी जोडिएको छ भन्ने स्पष्ट देखिने तथ्यांक सार्वजनिक भएको छ। हालैको तथ्यांक अनुसार, कूल निक्षेप/जीडीपी अनुपात १२०.२६ प्रतिशत रहेको छ भने कूल कर्जा/जीडीपी अनुपात ९७.०६ प्रतिशत पुगेको छ। यसले वित्तीय प्रणालीमा आम नागरिकको पहुँच, विश्वास र बैंकिङ क्षेत्रमा पूँजी परिचालनको गहिराइ दर्शाउँछ।

बैंक वर्गीकरणअनुसार विश्लेषण गर्दा, क्लास “ए” का व्यावसायिक बैंकहरू अत्यन्तै प्रभावशाली देखिएका छन्। यी बैंकहरूले जीडीपीको १०७.३४ प्रतिशत बराबरको निक्षेप संकलन गरेका छन् भने ८६.१२ प्रतिशत बराबरको कर्जा प्रवाह गरेका छन्। यो तथ्यले देखाउँछ कि मुलुकको आर्थिक गतिविधिमा प्रमुख योगदान यिनै बैंकहरूबाट भइरहेको छ। देशभर शाखा विस्तार, ठुलो पुँजी संरचना र प्रविधिमा लगानीले गर्दा क्लास “ए” बैंकहरू नेपालको वित्तीय प्रणालीको मेरुदण्ड बनेका छन्।

क्लास “बी” विकास बैंकहरूले १०.६९ प्रतिशत निक्षेप र ९.१४ प्रतिशत कर्जा मात्र व्यवस्थापन गरेका छन्। ती बैंकहरू प्रायः अर्धशहरी क्षेत्रमा सिमित रहेर सेवा प्रदान गरिरहेका छन्। त्यस्तै, क्लास “सी” वित्त कम्पनीहरूको योगदान झनै सानो छ—२.२४ प्रतिशत निक्षेप र १.८ प्रतिशत कर्जा मात्र। यी संस्थाहरू सामान्यतः साना व्यवसाय र व्यक्तिगत ऋणमा केन्द्रित छन्।

यी तथ्यांकले देखाउँछ कि नेपालको बैंकिङ प्रणाली अझै पनि केन्द्रीकृत रहेको छ। कुल वित्तीय कारोबारको ठूलो हिस्सा केही ठूला व्यावसायिक बैंकहरूको हातमा केन्द्रित छ। यस्तो संरचनाले यद्यपि स्थायित्व दिन्छ, तर यसले साना तथा क्षेत्रीय वित्तीय संस्थाको भूमिकालाई न्यून बनाउँछ। सरकारले यदि वित्तीय पहुँचलाई समावेशी बनाउने हो भने, क्लास “बी” र “सी” संस्थाहरूलाई प्रवर्द्धन गर्ने नीति आवश्यक हुनेछ।

अन्त्यमा, हालको जीडीपीमा आधारित निक्षेप र कर्जा अनुपात सकारात्मक देखिए तापनि, समावेशी वित्तीय प्रणाली विकास गर्नको लागि साना वित्तीय संस्थाहरूको सहभागिता बढाउनुपर्ने खाँचो देखिन्छ। यसले देशको आर्थिक सन्तुलन र वित्तीय स्थायित्वमा दीर्घकालीन योगदान पुर्याउन सक्छ।

Nepal’s banking sector continues to show a strong linkage with the national economy, as indicated by the latest financial indicators of deposit and credit in relation to Gross Domestic Product (GDP). The combined ratio of total deposits to GDP stands at a significant 120.26%, while the total credit to GDP ratio is 97.06%. These ratios reflect the depth of financial intermediation in the country and the level of trust the public places in financial institutions.

Breaking it down by institutional class, Class "A" commercial banks remain the dominant players, accounting for 107.34% of GDP in total deposits and 86.12% in total credit. This clearly illustrates their commanding presence in mobilizing public funds and extending loans within the economy. The robust financial infrastructure, large branch network, and higher capital base have helped Class "A" banks to maintain this lead, ensuring they serve as the backbone of Nepal’s banking system.

In contrast, Class "B" development banks, while playing a supportive role, contribute 10.69% of GDP in deposits and 9.14% in credit. Their impact is regionally important, particularly in semi-urban areas, but they are far from rivaling the dominance of commercial banks. Class "C" finance companies contribute even less, with only 2.24% in deposits and 1.8% in credit relative to GDP. These figures indicate that while they still cater to niche markets, especially in micro and small enterprise financing, their role in the overall financial ecosystem is minimal in terms of volume.

The disparity in these figures underscores the consolidated nature of Nepal’s banking sector, where a few large institutions handle the bulk of the country’s financial transactions. It also raises questions about the inclusiveness and accessibility of financial services offered by lower-tier institutions. While Class "A" banks have made progress in expanding their reach, the relatively low contribution of Class "B" and "C" institutions highlights potential areas for policy intervention, especially to enhance financial access in underserved communities.

In conclusion, while the overall deposit and credit ratios to GDP are high—signaling a healthy level of monetization and financial sector involvement in the economy—the concentration of financial activity in commercial banks points to both their strength and the need for deeper diversification in Nepal’s financial architecture. Encouraging broader participation of development and finance companies could lead to a more resilient and inclusive financial system in the long term.