Inflation

Consumer Price Inflation Trends: Nepal-India Gap Narrows in FY 2024/25

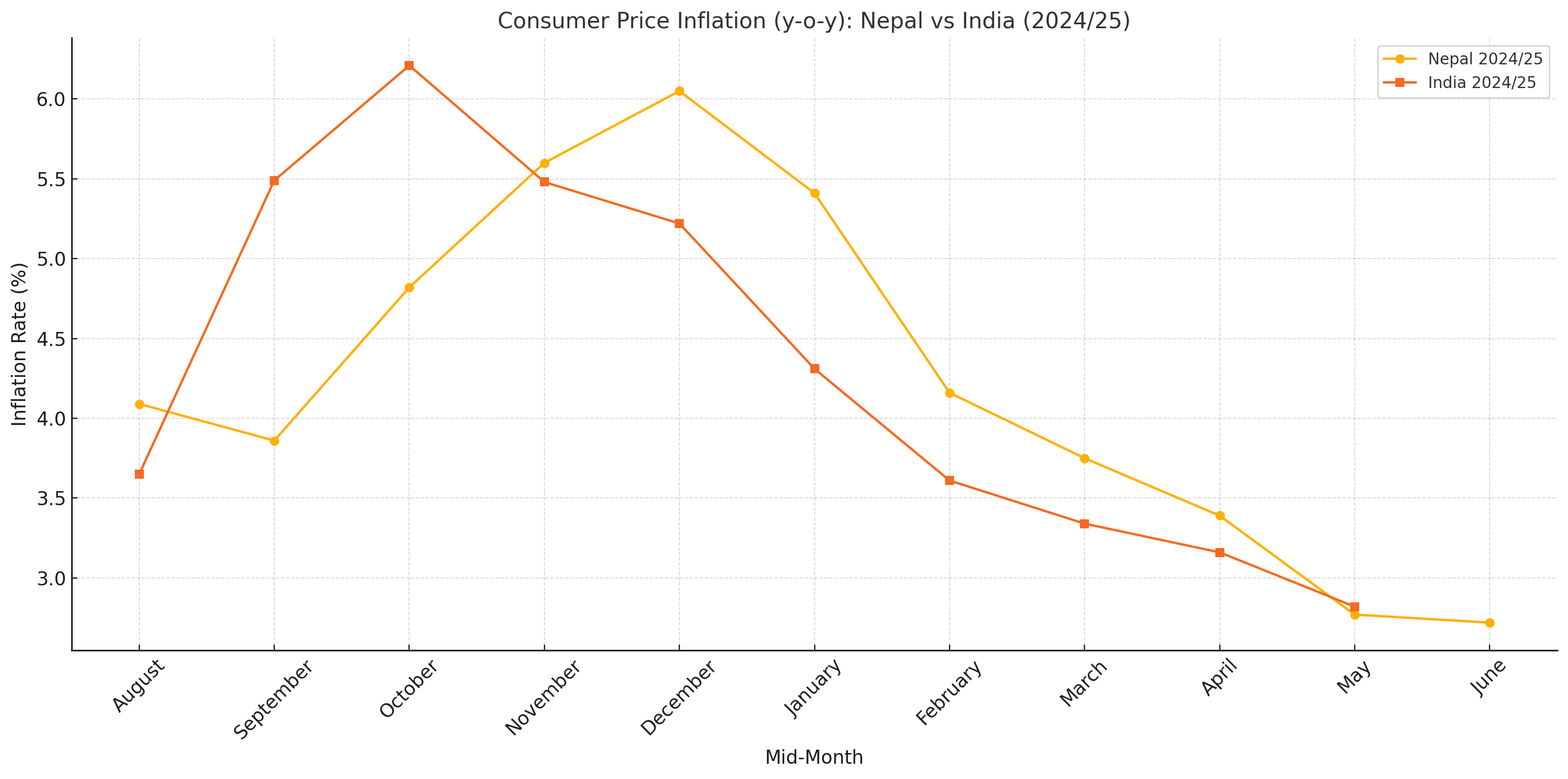

In fiscal year 2024/25, consumer price inflation in Nepal has shown a declining trend, averaging 4.24% up to mid-June, compared to India’s 4.33%. The gap between the two countries has significantly narrowed, with Nepal even recording lower inflation than India in months like September and October. The chart highlights that while India's inflation exhibited moderate volatility across months, Nepal maintained a more consistent downward trajectory. This convergence in inflation rates reflects a relative stabilization in Nepal’s price environment and indicates improved control over domestic inflationary pressures amid global economic fluctuations.

Sandeep Chaudhary

1 min read

The latest comparative data on consumer price inflation between Nepal and India reveals a shifting pattern of inflationary pressure across both economies over the past four fiscal years. The year-on-year inflation data up to mid-July 2025 highlights notable fluctuations, particularly in the inflation gap between the two neighboring countries.

In fiscal year 2021/22, Nepal's average inflation rate stood at 6.32%, slightly higher than India's 6.02%, with a modest positive deviation of 0.31 percentage points in Nepal's favor. However, by 2022/23, Nepal experienced a significant inflation surge, averaging 7.74% compared to India’s 6.06%, widening the gap to 1.68 percentage points. This period coincided with rising global commodity prices and domestic supply chain challenges.

The inflation gap began to tighten in 2023/24, with Nepal’s average inflation falling to 5.44%, and India’s at 5.11%, resulting in a reduced deviation of just 0.34 percentage points. Notably, Nepal's inflation was higher than India's in the early months, but gradually reversed in the latter half, where India’s rates often outpaced Nepal’s.

In the current fiscal year 2024/25 (till mid-June), the average inflation in Nepal has further declined to 4.24%, while India recorded a slightly higher average at 4.33%. This marks the first time in four years where India has registered a higher inflation rate than Nepal, albeit by a minimal deviation of -0.06 percentage points. The sharpest monthly negative deviation was observed in September 2024, when Nepal’s inflation (3.86%) was 1.63 points lower than India’s (5.49%).

This recent convergence indicates an easing of inflationary pressures in Nepal, supported by tight monetary policy and a stable external sector. On the other hand, India appears to be witnessing relatively persistent inflation in certain months, likely driven by food price shocks and demand recovery.

Overall, the narrowing gap reflects regional inflation synchronization, but also underscores the need for both economies to remain vigilant in managing price stability amidst global uncertainties.

Advertisement

Written by

Sandeep Chaudhary